Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 5th August 2022

Investment markets and key developments over the past week

- The rebound in share markets continued over the last week, helped by good earnings data and relief that increased China/US tensions resulting from US House Speaker Nancy Pelosi’s visit to Taiwan did not spill over into a more serious conflict (at least not yet). Despite a slight set back on Friday, as strong US payrolls data were seen as keeping the US Federal Reserve (Fed) hawkish for now, for the week US shares rose 0.4%, Eurozone shares rose 0.3% and Japanese shares gained 1.4%. Chinese shares were the exception and fell 0.3%. The positive global lead, along with signs of slightly diminished hawkishness from the Reserve Bank of Australia (RBA), pushed the Australian share market up 1% for the week. For the week, bond yields reversed some of their recent falls, mostly after the strong US jobs data. Oil and metal prices fell, but iron ore rose. The $A fell as the $US rose.

- We remain of the view that shares are vulnerable to a pull back over the next few months as central banks are a way off actually cutting rates, recession risk is still rising (and this runs the risk of significant earnings downgrades) and geopolitical risk is still on the rise, as highlighted by China/US tensions in the last week and the upcoming November US mid-terms. However, the continuing strength of the rebound (with the direction setting US share market up 13% from its low) raises the possibility that we may have seen the bear market low and any pull back may just be a partial retracement of the rally since mid-June. Time will tell. Either way, on a 12-month horizon remain optimistic on shares as inflation recedes, central banks become less hawkish and a deep recession is likely to be avoided.

- First the bad news – which drives the risk of another pull back:

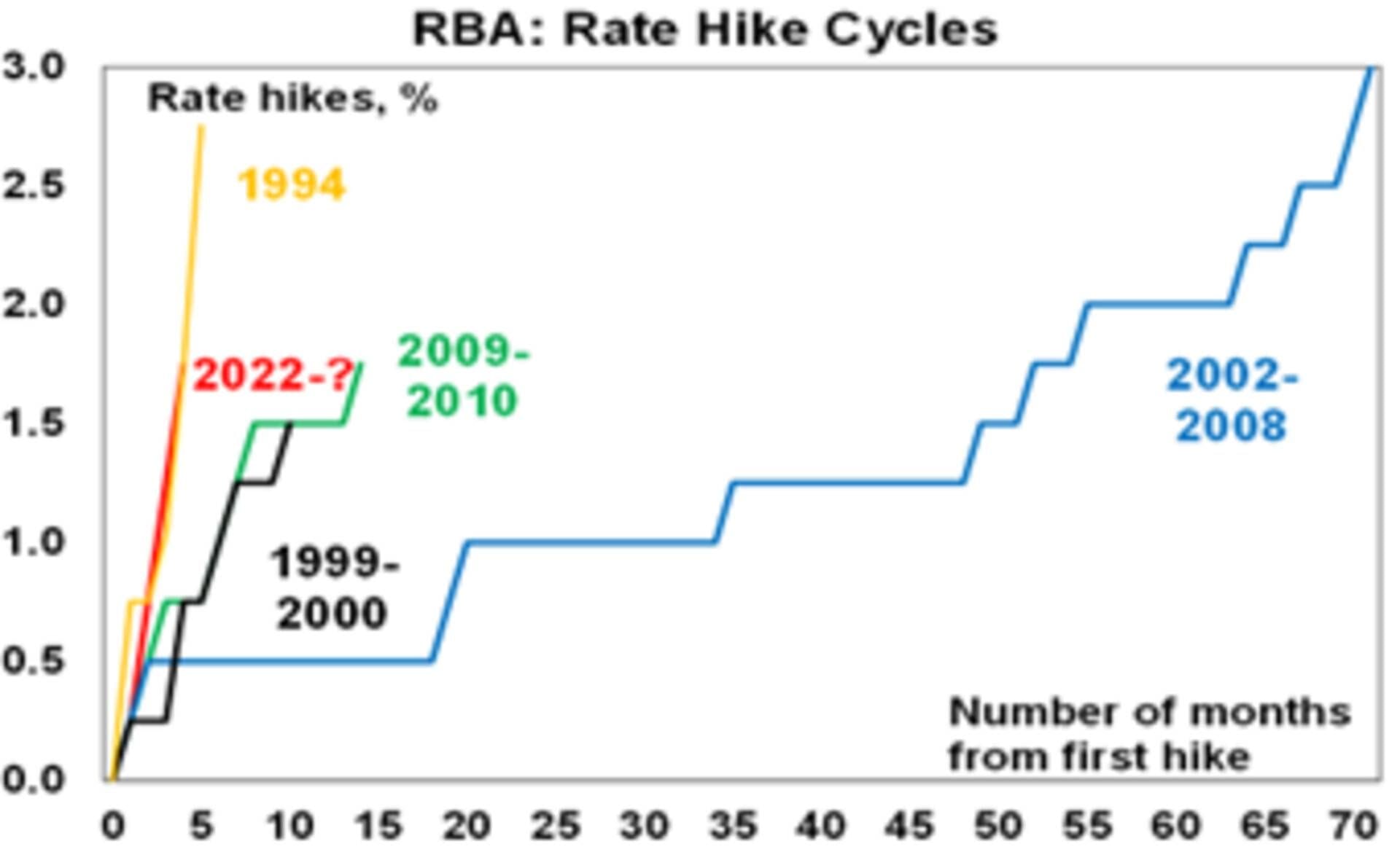

- Central banks are still hawkish. Various Fed officials indicated the Fed is still a long way from pivoting to an easier stance and stronger than expected US payroll growth in July, along with a new low in unemployment of 3.5%, will keep the Fed hawkish for now with the possibility of another 0.75% rate hike in September. The Bank of England (BoE) hiked rates by another 0.5% and started active bond selling, now expecting inflation to peak at 13%, and indicated a readiness to implement more “forceful” hikes despite expecting a severe recession to start this year. The RBA meanwhile hiked rates another 0.5% and indicated that more rate hikes are likely. Reflecting the low starting point and the severity of the inflation breakout, this is the most aggressive RBA rate hiking cycle seen in the last 30 years, except for the rate hikes that occurred in August to December 1994 with which this cycle is comparable. See the next chart.

Source: RBA, AMP

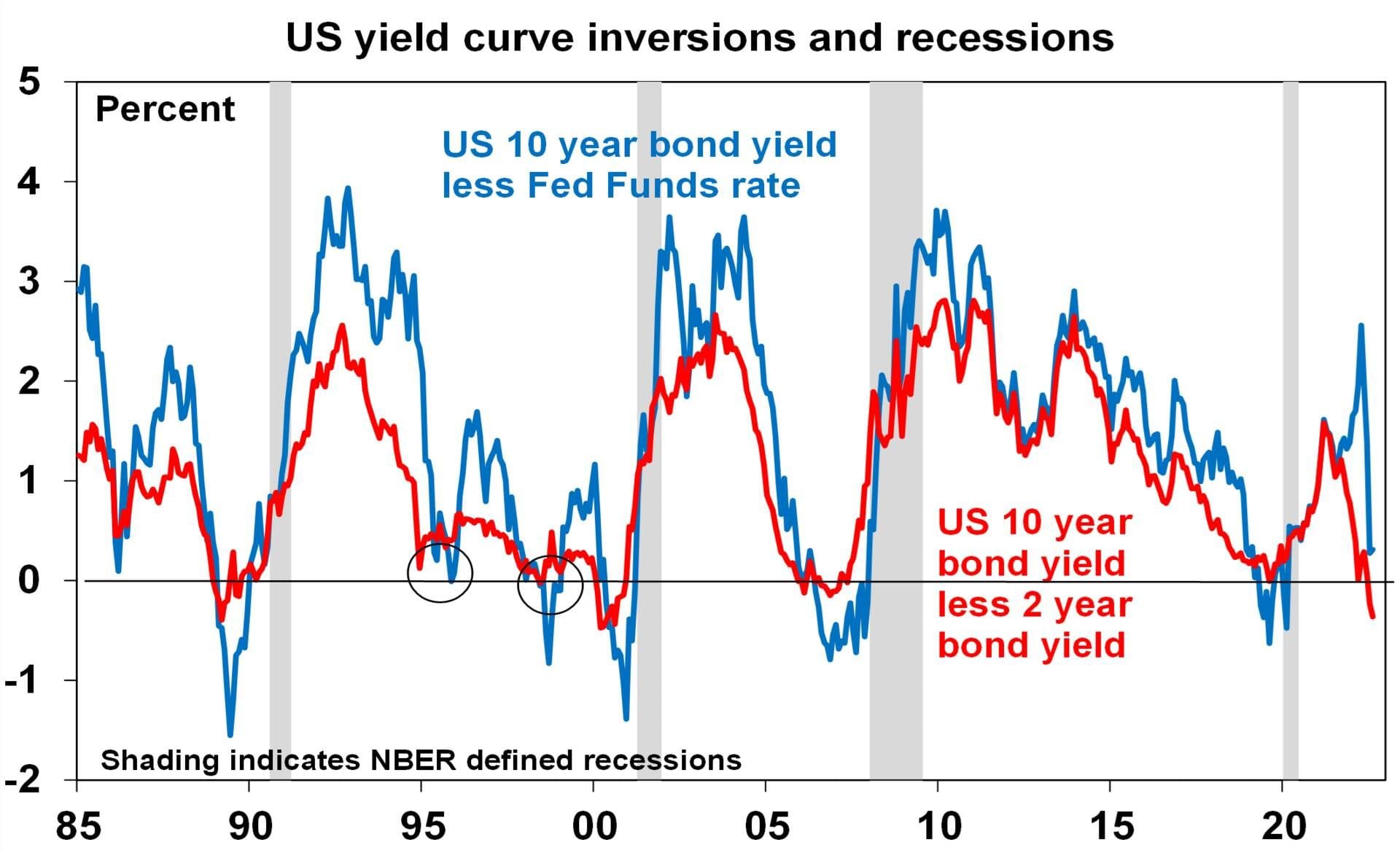

- The risk of a “real” recession in the US is continuing to build according to the US yield curve with the US 10 year less 2 year yield curve inverting further and the 10 year less Fed Funds rate gap getting very close to inverting too. A “real” recession, i.e., beyond the technical recession in the first half of this year, would mean a significant downgrade cycle for US, global and Australian share market earnings.

- Surging gas and electricity prices in Europe are still adding to the risk of recession there – particularly in Germany.

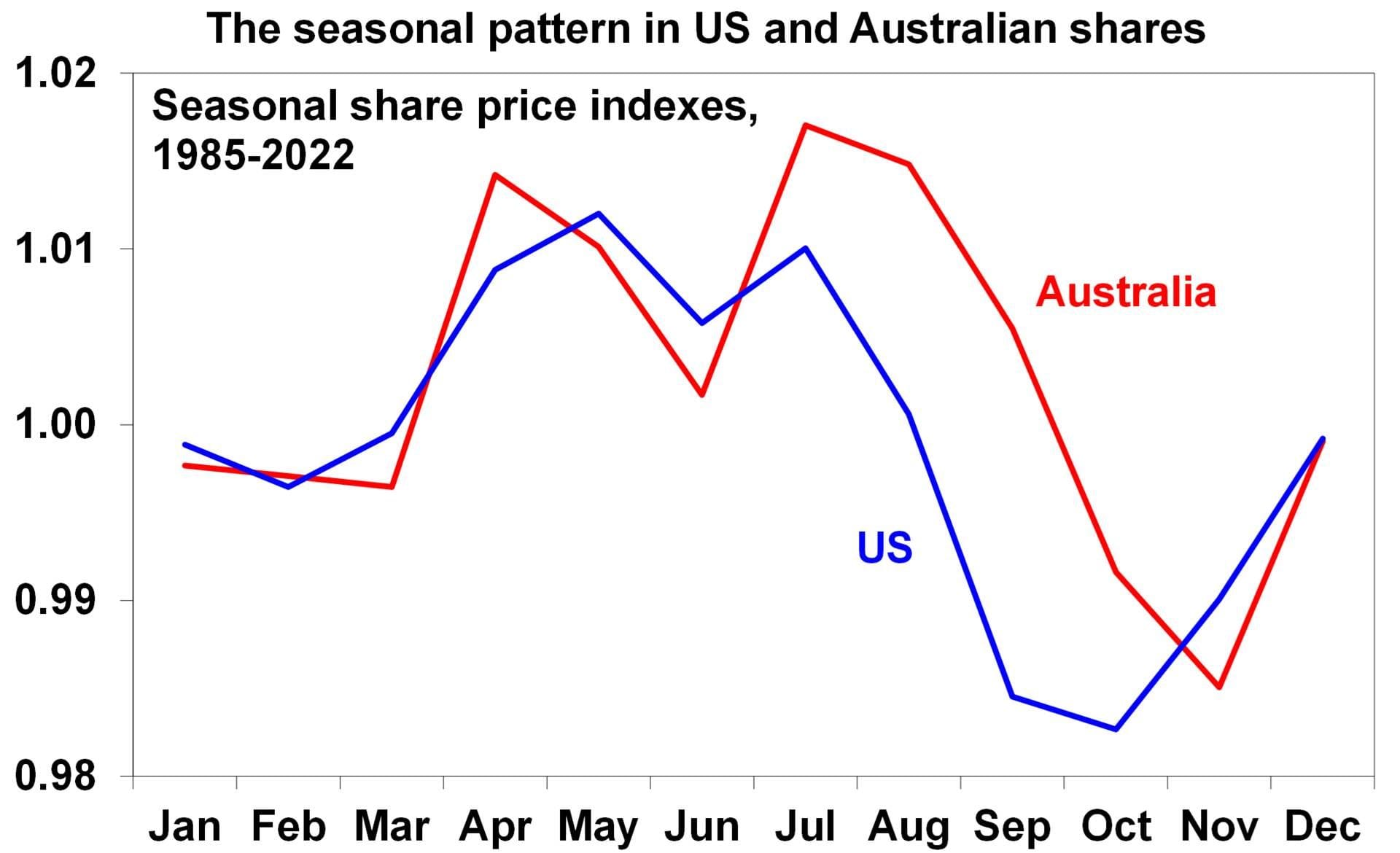

- After July’s strength the seasonal pattern for shares historically has turned down from August through to October.

Source: Bloomberg, AMP

- US shares usually have a rough year prior to the mid-term elections on the back of political uncertainty, but then rally once they are out of the way.

- China/US tensions flared up with House Speaker Pelosi’s visit to Taiwan. While nothing seriously bad has unfolded (yet), they highlight the ongoing tensions which still threaten to get worse before they get better.

- But there is also good news supporting the view we may have seen the low; or even if not, shares will be up on a 12-month view.

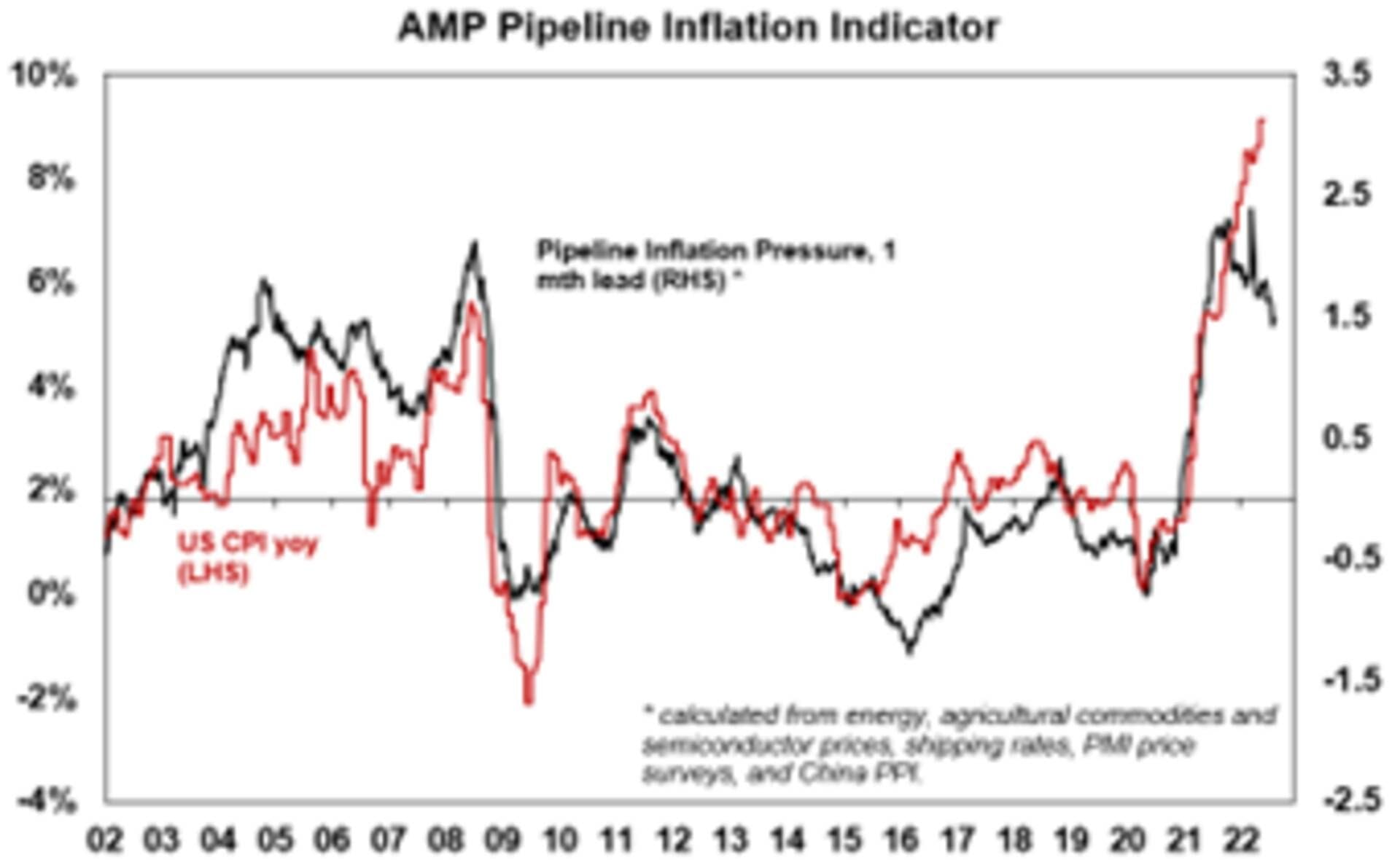

- Global inflation pressures may be at or close to a peak (excepting Europe, with its specific energy issues). The US Pipeline Inflation Indicator is continuing to trend down, reflecting a combination of a falling trend in work backlogs, freight rates, metal prices, grain prices and even oil prices. This was also evident in the ISM business survey showing falling delivery times, order backlogs and price pressures.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components. Source: Bloomberg, AMP

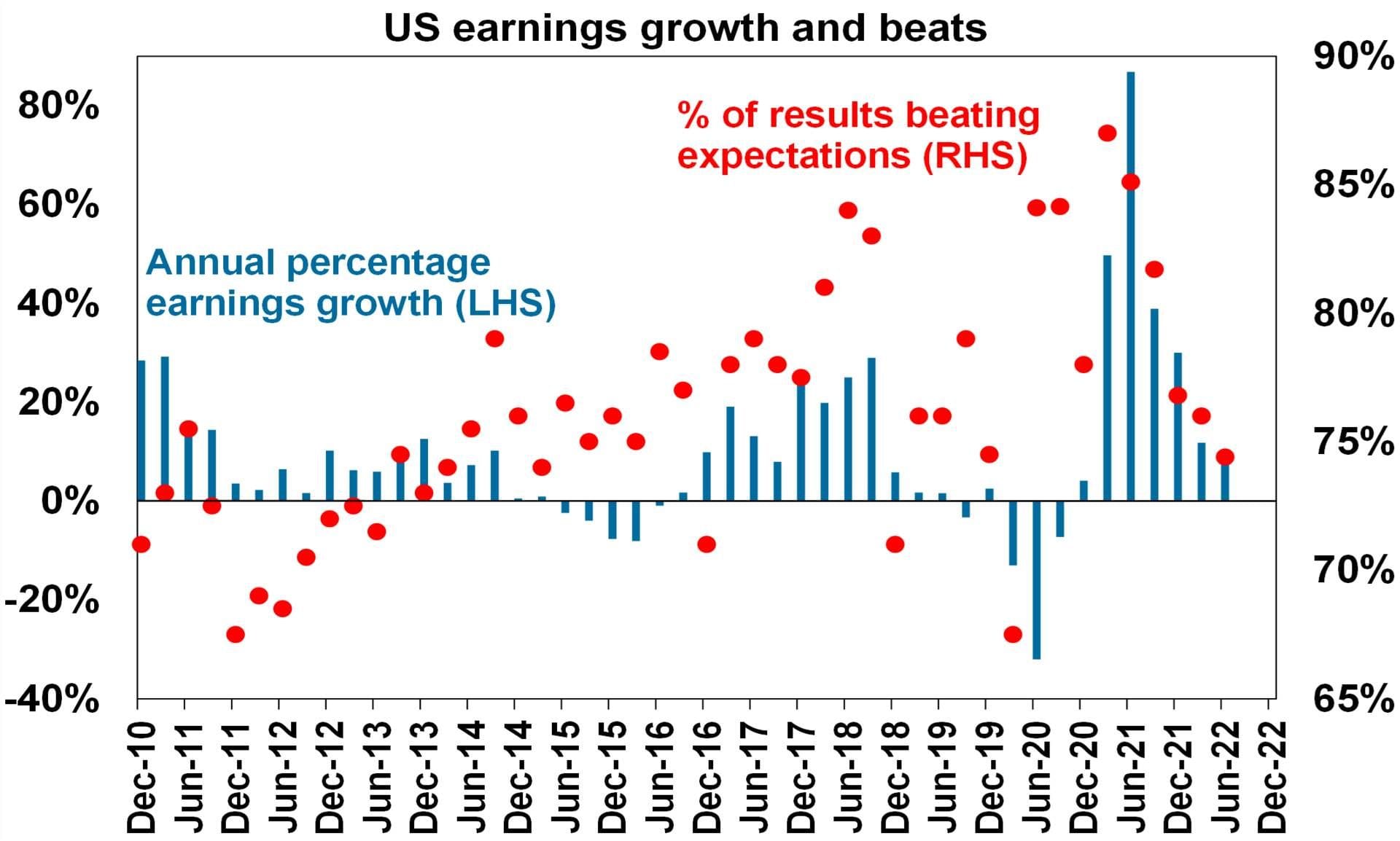

- US earnings reports have surprised on the upside again, with consensus earnings expectations for the year to the June quarter rising from 5%yoy three weeks ago to now 9.2% with outlook statements being mixed, as opposed to mostly negative as feared might have been the case. And earnings growth outside the US has been even stronger.

- Bond yields are well down from their June highs – with US 10-year yields down from 3.5% to 2.8% and Australian 10-year yields down from 4.2% to 3.1%. Falling bond yields reduce valuation pressure on shares and can help economic growth as they reduce longer term funding costs. Falling bond yields have already driven some Australian banks to lower their fixed mortgage rates (although this won’t be enough to avert the fixed rate cliff that fixed borrowers on roughly 2% rates will face when they roll over to fixed or variable rates two and a half times or more higher).

- Share markets anticipated the inversion of the US yield curve and its recession signal this time, whereas on previous occasions they only fell sharply well after the inversion. In other words, recession may have already been discounted.

- Central banks may still be hawkish, but they are softening a bit at the edges – suggesting they may be getting closer to the top and that they are also conscious of the worsening growth outlook. This was evident in Fed Chair Powel referring to eventually slowing the pace of rate hikes, the BoE noting that it’s not on a “pre-set” path and in the RBA’s commentary this week. Looks like the BoE got the “not on a pre-set path” reference from the RBA.

- Turning specifically to the RBA, which raised rates again by another 0.5%, the message from its post meeting statement and its quarterly Statement on Monetary Policy is that it remains hawkish, but it is starting to leave a bit of wiggle room. Given its upwards revision to its inflation forecast for this year to 7.75%yoy and the very tight labour market, it rightly remains focussed on slowing demand and keeping inflation expectations down and so is still flagging more rate hikes ahead. But its reference to wanting to keep the economy on an “even keel”, its downwards revisions to growth (to a very pedestrian 1.75% for the next of years), its forecast of a rise in unemployment from 2024, its acknowledgement of falling consumer confidence, its recognition of negative wealth effects from falling home prices, its stronger recognition that some households are not well placed to withstand rate hikes and its reiteration that its “not on a pre-set path” all suggest that its open to an easing in the pace of rate hikes in the months ahead as its tightening starts to get traction. This is broadly consistent with the assessment that cash rate hikes will slow in the months ahead, with some months seeing no moves ahead of a peak in the cash rate at 2.6% either later this year or early next, and that rates will start to fall in the second half of next year.

Coronavirus update

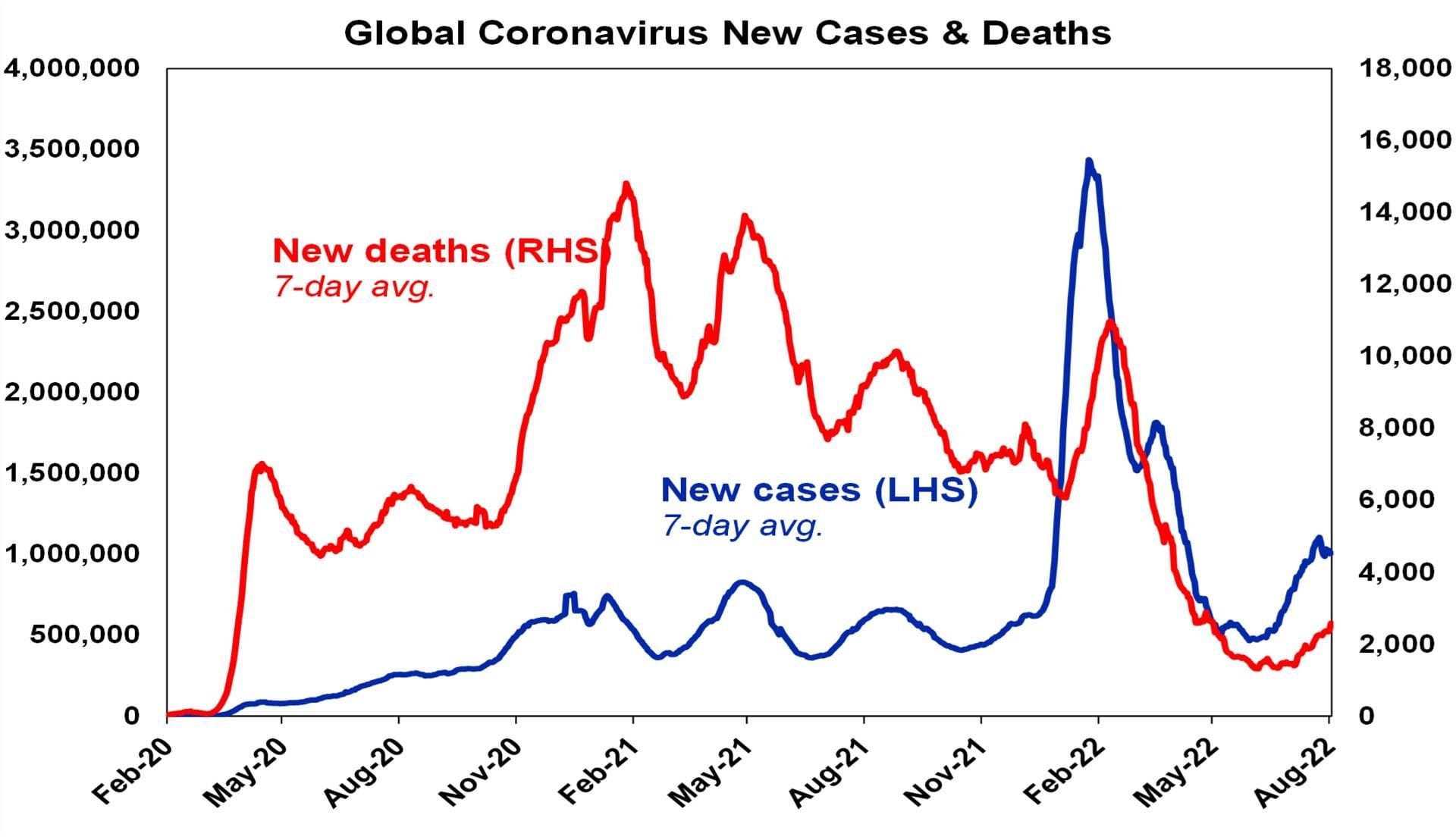

- New global COVID cases are down from their recent high – with Europe and South America down, the US stable but Asia (notably Japan, South Korea and Indonesia) up. New cases in China are remaining low.

Source: ourworldindata.org, AMP

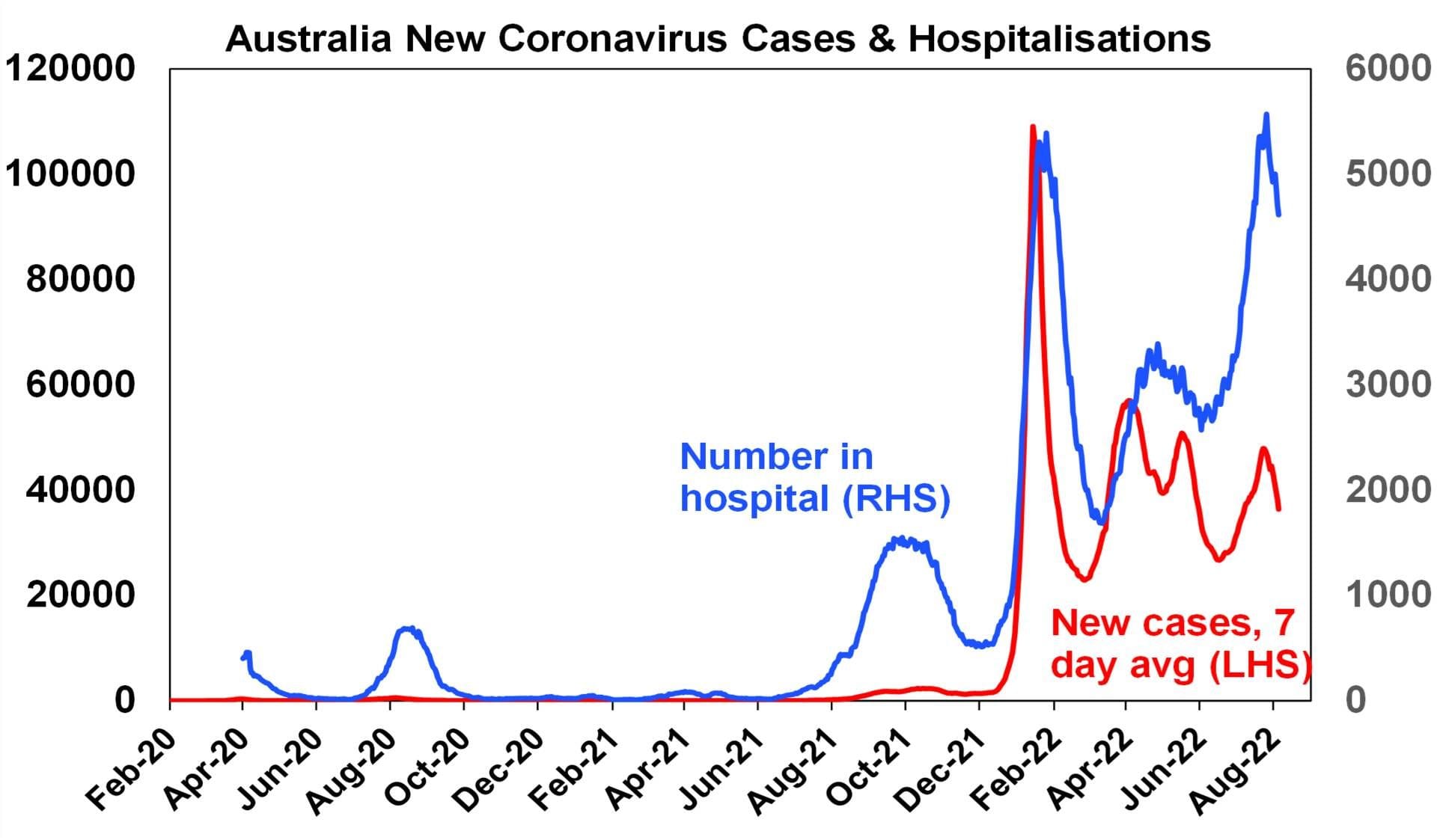

- Australia has seen new cases and hospitalisations roll over again. Although new daily deaths with COVID spiked above their high from earlier this year, this was partly due to the processing of a backlog of deaths in Victoria; and at least they remain about 90% lower than where they would have likely been based on the pre-Omicron and pre-vaccine period.

Source: ourworldindata.org, AMP

Economic activity trackers

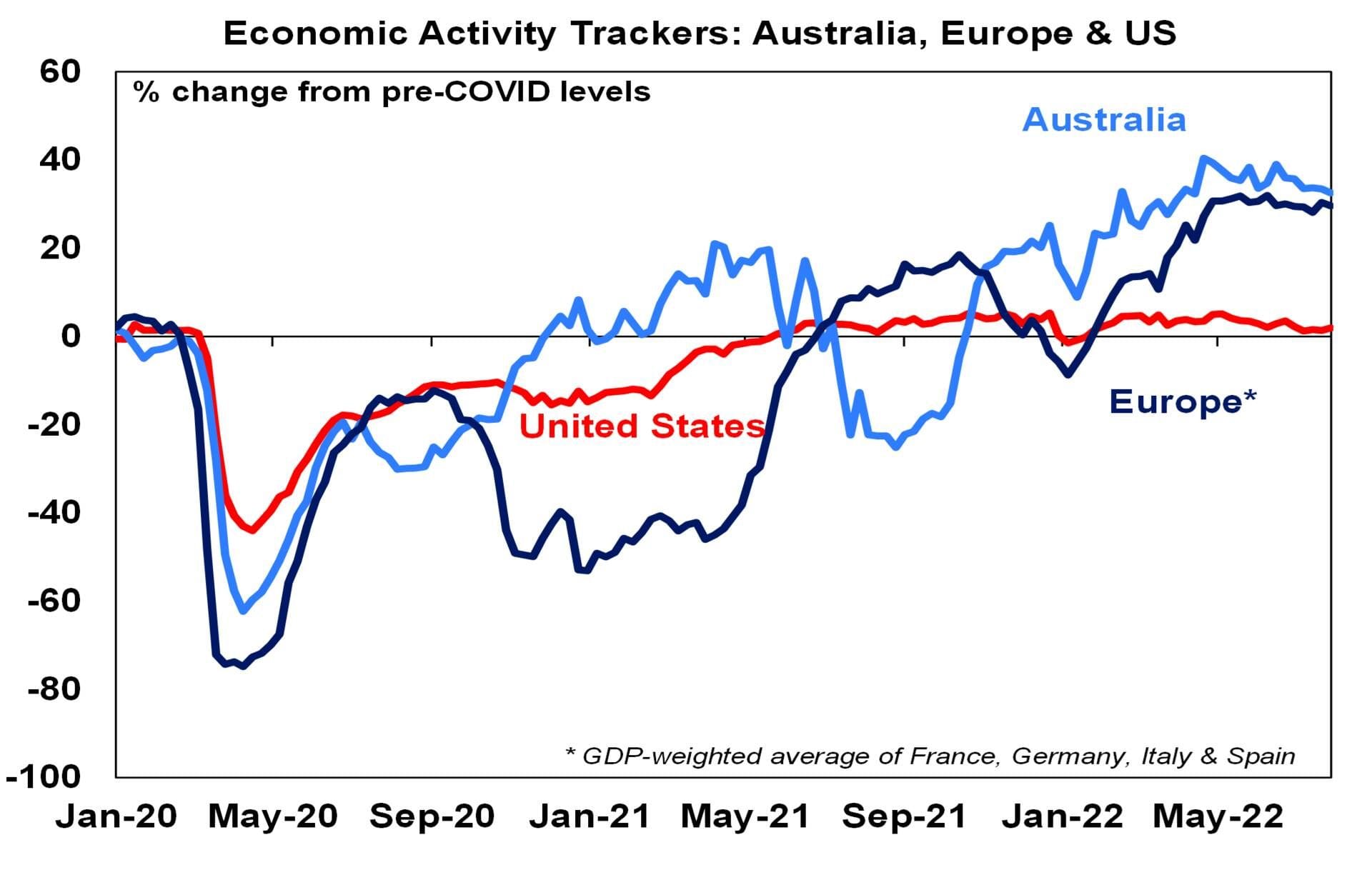

- The Australian Economic Activity Tracker fell slightly in the last week continuing the loss of momentum seen since April consistent with a slowdown in growth. The US Tracker rose slightly and the European Tracker fell slightly.

Based on weekly data for e.g. job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Major global economic events and implications

- US data was mixed. The July services conditions ISM surprisingly rose to a solid 56.7 and jobs data was strong, with payrolls up more than expected, unemployment down to a new low of 3.5% and wages growth accelerating. But against this the manufacturing ISM and construction spending fell. And forward-looking labour market indicators are continuing to soften, with job openings and quits falling (albeit from still high levels) and jobless claims continuing to trend up. The ISM survey showed a further fall in supplier deliveries, order backlogs and output prices, all pointing to easing inflation.

- 87% of US S&P 500 companies have now reported June quarter earnings, with 75% ahead of expectations and earnings growth expectations for the quarter, rising from 5%yoy at the start of the reporting season to now 9.2%, and on track for 10%. This is far stronger than expected. Outlook comments have been mixed, reflecting uncertainty regarding the growth outlook, but have not been overwhelmingly negative. Earnings growth outside the US has remained stronger, at around 16%yoy.

Source: Bloomberg, AMP

- The Democrats’ downsized build back better budget reconciliation legislation – called the Inflation Reduction Act – is close to passage through Congress. The main elements are a 15% minimum corporate tax rate, a 1% tax on share buybacks, lower drug prices and clean energy subsidies. It’s unlikely to have much macro impact though (as it’s a tiny fraction of the size of the original $3.5trn plan), it won’t really reduce inflation much (by no more than 0.1% pa) and will only start reducing the budget deficit from around 2027. Rough estimates are that it will amount to a 3% corporate tax rate increase.

- Eurozone producer prices were up a record 36%yoy in June, with energy prices up 93%yoy. German baseload electricity prices are now up 8-fold from where they were at the start of last year. All of which highlights the very high risk of recession in Europe and ongoing inflation pressures there.

- Japanese June household spending growth moved up and cash wages growth continues to trend up, but it’s only around 2%yoy.

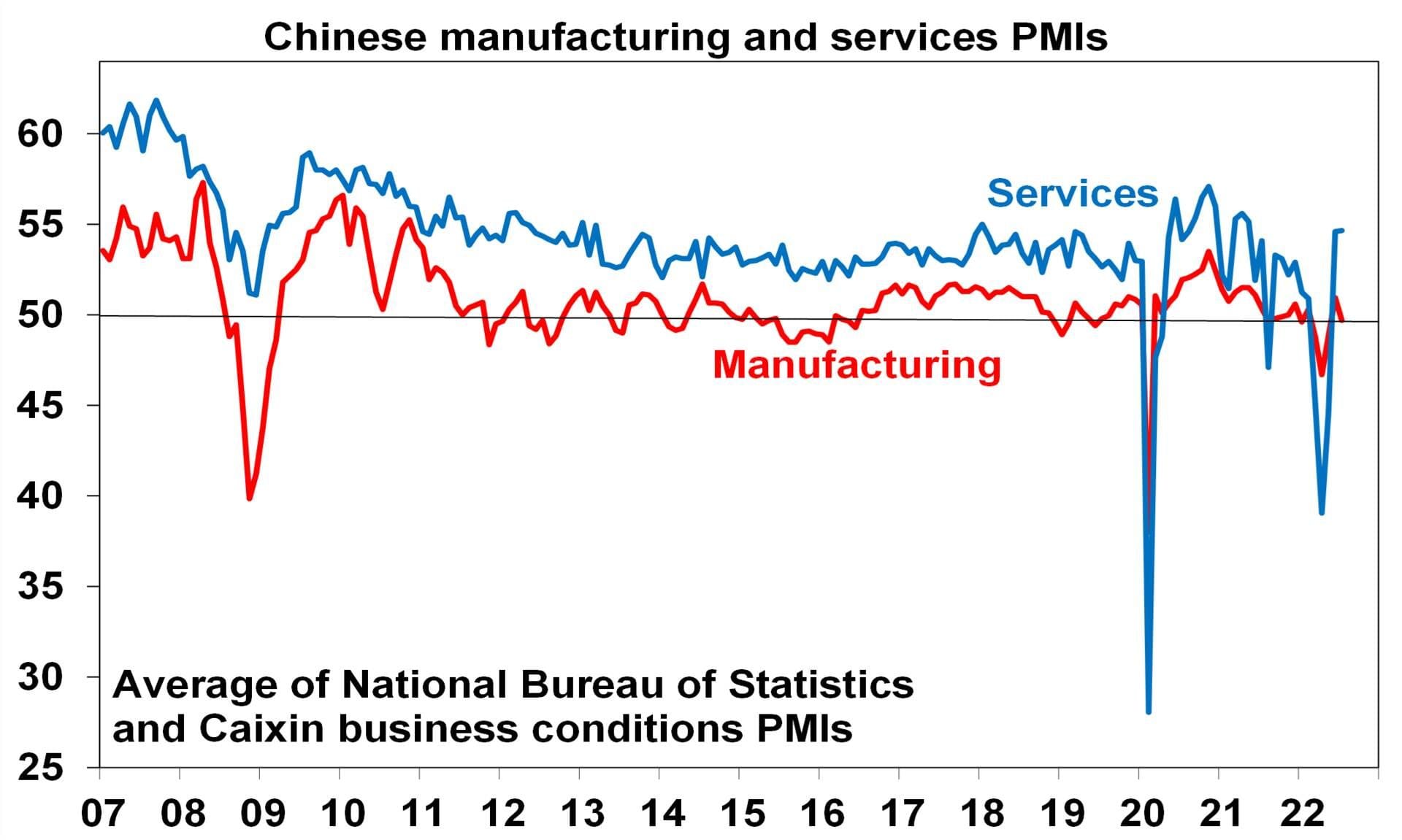

- Chinese manufacturing conditions PMIs slipped back in July, but services PMIs held on to their gains from reopening.

Source: Bloomberg, AMP

Australian economic events and implications

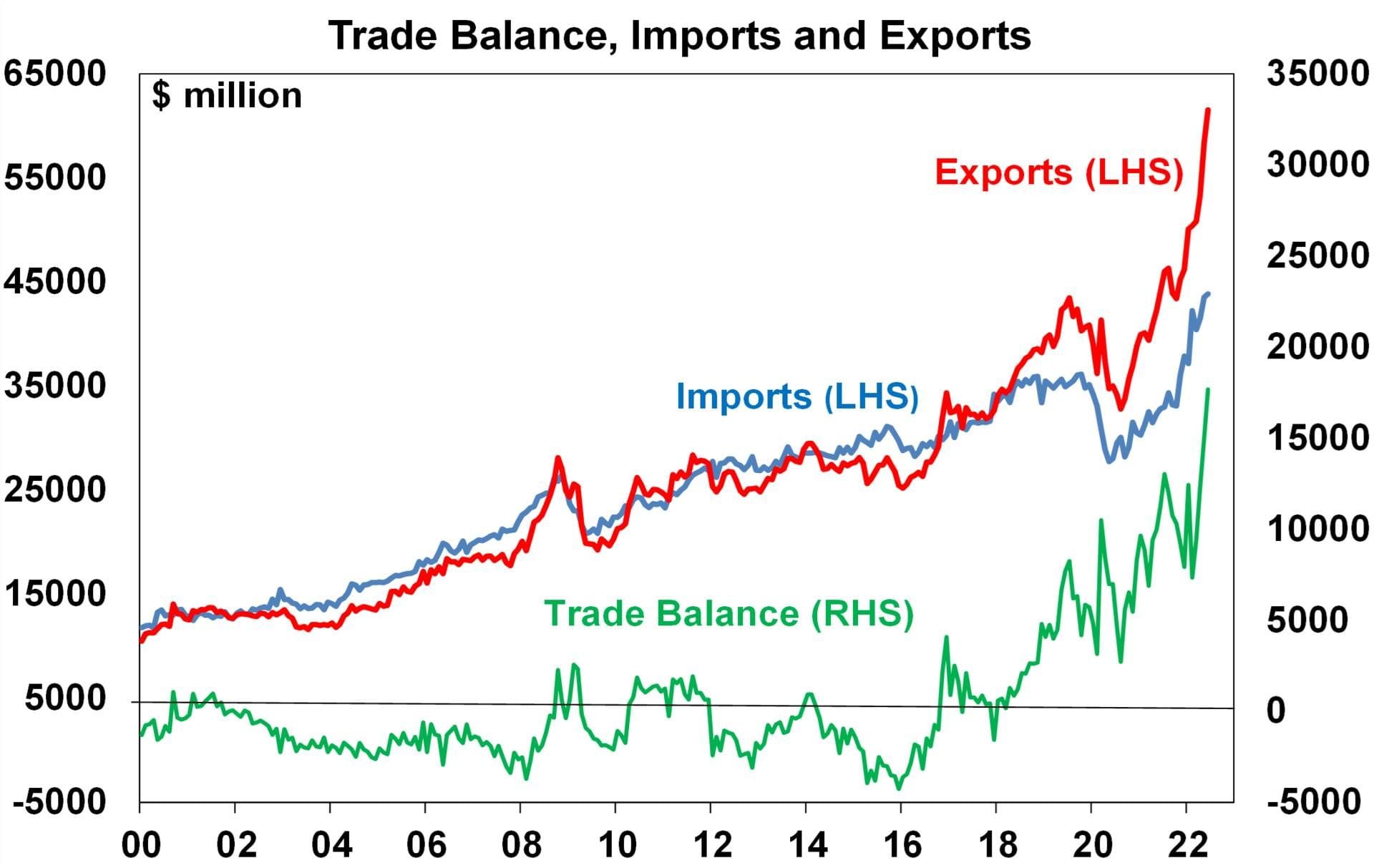

- Australian economic data was mixed. On the positive side real retail sales rose strongly in the June quarter, car sales bounced back strongly in July and the trade surplus rose to a new record high of $17.7bn. Net exports are expected to contribute around 1 percentage points to June quarter GDP growth and the strong rise in real retail sales augurs well for June quarter consumption growth. Of course, monthly retail sales data is now slowing and rising interest rates and poor consumer confidence points to a slowdown ahead.

Source: ABS, AMP

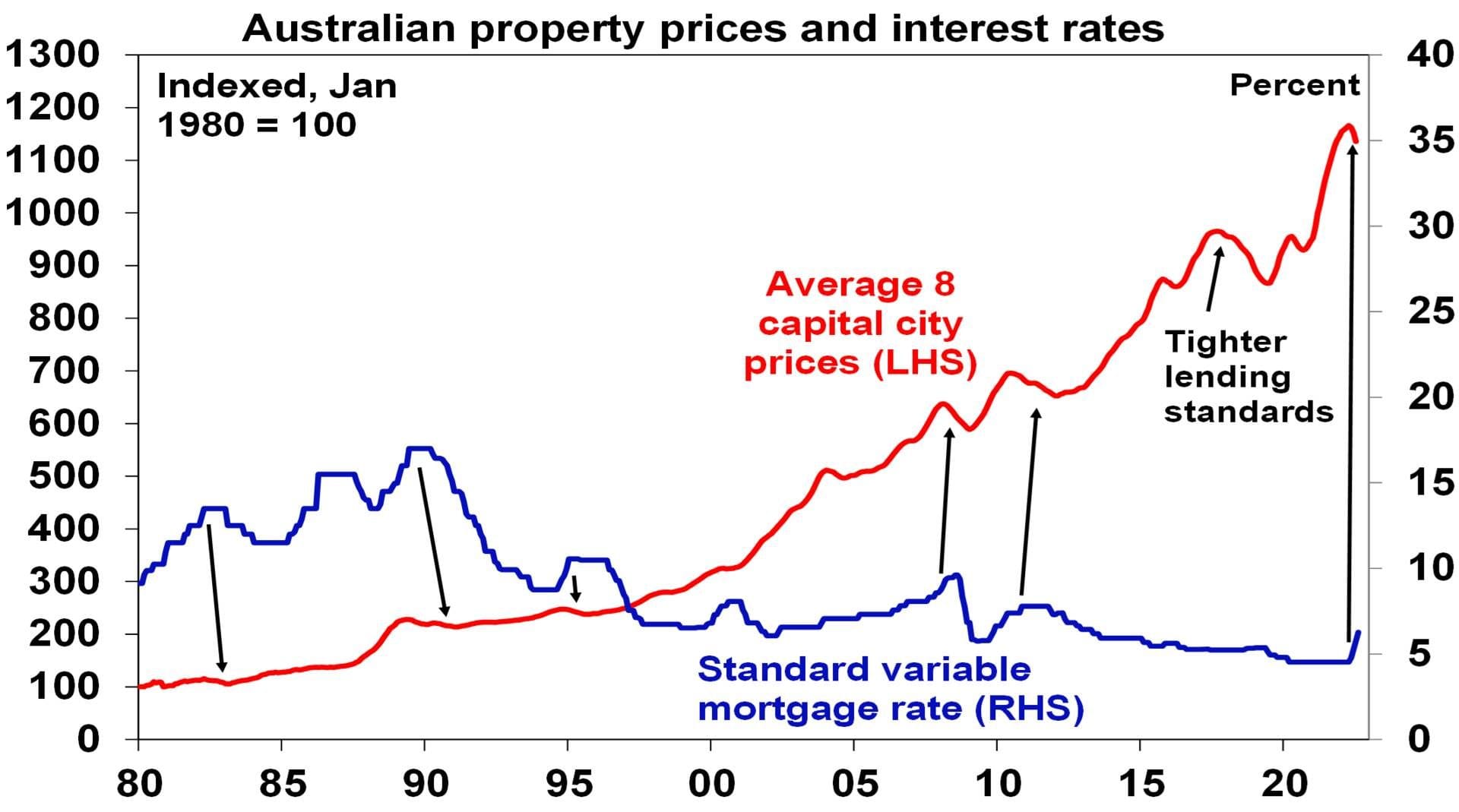

- Against this though, ANZ job ads remained high, but fell in July and may be starting to slow and housing related data was soft. Building approvals fell less than expected but the trend is clearly down, which, even allowing for a large pipeline of work yet to be done, points to slowing home building activity ahead. Housing finance fell by more than expected – and now looks to be clearly rolling over. More falls are likely ahead, as mortgage rate hikes and falling property prices impact. And CoreLogic data for July confirmed that the decline in home prices is accelerating, led by Sydney.

- So far, the decline in national average home prices is just 2%, which is just a flick off the top, but the pace of decline is comparable to what was seen going into the Global Financial Crisis (GFC), the run up to the early 1990s recession and in the early 1980s recession. But all of those slumps followed long periods or rate hikes with interest rates at their peaks and about to start falling, whereas this time around we are only four months into interest rate hikes, with more rate hikes still to come. The rapidity of the decline in home prices this time around so early in an RBA tightening cycle reflects the de facto tightening that started with rising fixed mortgage rates a year ago. but more importantly. the heightened sensitivity to rising interest rates flowing from much higher debt levels now and very poor consumer confidence.

Source: CoreLogic, AMP

- Meanwhile the Melbourne Institute’s Inflation Gauge rose 1.2% in July, or by 5.4%yoy. While it’s undershooting the upswing in the CPI, it’s consistent with more upside in CPI inflation.

What to watch over the next week?

- In the US, the focus will be on July CPI data (Wednesday) which is expected to show a fall in headline inflation to 8.8%yoy (from 9.1%) helped by lower gasoline prices, but a rise in core inflation to 6.1%yoy (from 5.9%). Small business optimism for July (Tuesday) is likely to show a further fall.

- Chinese inflation data (Wednesday) is expected to show a rise in CPI inflation to 2.8%yoy, but a fall in producer price inflation to 4.9%yoy. Credit data will also be released.

- In Australia, the NAB business survey and the Westpac/MI consumer survey (both Tuesday) are likely to show further falls in business and consumer confidence.

- The June half Australian earnings reporting season will ramp up, with around 17 major companies due to report covering 18% of market cap including Suncorp (Monday), Computershare and CBA (Wednesday), Mirvac, AMP, QBE and Telstra (Thursday) and Resmed & IAG (Friday). Consensus expectations are for around 20% earnings growth for the 2021-22 financial year, but with this boosted by energy earnings (+275%) and industrials averaging around 9.5% growth. The focus will likely be on outlooks given cost pressures, labour shortages and slowing consumer demand.

Outlook for investment markets

- Shares remain at high risk of a pull back in the months ahead as central banks continue to tighten to combat high inflation, the war in Ukraine continues and uncertainty about recession remains high. However, expect to see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary policy brakes.

- With bond yields looking like they have peaked for now, short-term bond returns should improve.

- Unlisted commercial property may see some weakness in retail and office returns (as online retail activity remains well above pre-COVID levels and office occupancy remains well below). Unlisted infrastructure is expected to see solid returns.

- Australian home prices are expected to fall 15 to 20% into the second half of next year, as poor affordability and rising mortgage rates impact.

- Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

- The $A is likely to remain volatile in the short-term as global uncertainties persist. However, a rising trend in the $A is likely over the medium-term as commodity prices ultimately remain in a super cycle bull market.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer