Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A FinSec View – GDP, Liquidity Risk, Retirees & More…

|

15th March 2024 |

Glass half-full approach as we see some silver linings

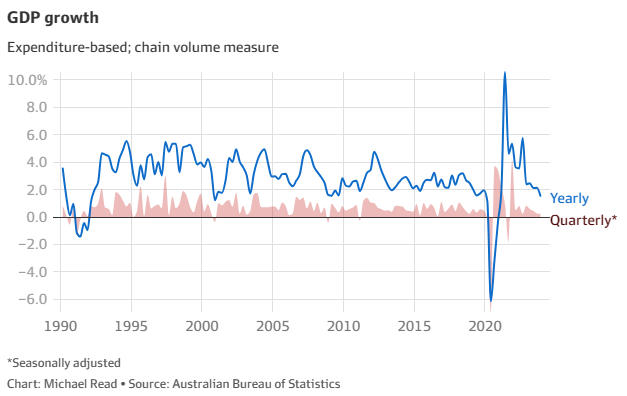

When Treasurer Jim Chalmers took to the media lectern to welcome December quarter GDP figures showing the very slimmest of growth (0.2 per cent), he embodied the true definition of a “glass half-full” kind of person. “Even weak growth is welcome growth in the circumstances,” Treasurer Chalmers said, as annual growth slumped to just 1.5 per cent, the lowest rate of growth since the dot com crash of 2000 (outside of the pandemic and the Global Financial Crisis). “Slow growth is still significant growth given the challenging global conditions combined with the impact of higher interest rates here in our own economy.” Though we are not in a technical recession, given the three quarters of consecutive per capita GDP contraction, Australia is in a “per capita recession”. Over the 12 months ending December, GDP per capita plunged 1.0%. That is, had it not been for our significant immigration inflow, we would indeed be in a technical recession.

However, the Treasurer’s unapologetic glass half-full approach seems to have rubbed off on us here at the View, because while we often talk about the things that are wrong, or concerning, in the economy, this month we thought it was worth looking at what might go right. To start with, we have a US economy that may be more resilient than first thought, so far avoiding a recession and growing at a stunning 3.3 per cent annualized rate in the fourth quarter. In January, the US economy added 353,000 jobs and wages increased 4.5 per cent year on year, though that pace is likely to slow. Meanwhile, the US housing market appears to be recovering as mortgage rates ease. Fed Reserve Chair Jerome Powell told the House Financial Services Committee last week that: “if the economy evolves broadly as expected, it will likely be appropriate to begin dialling back policy restraint at some point this year.” Further, we are witnessing what some have described as the dawn of an Artificial Intelligence-led productivity boom in the US (which we expect to be felt here, in due course), as companies use ChatGPT and other AI tools to reduce costs and create efficiencies for themselves and their customers. According to the Capital Group analysis, companies in the healthcare, financial services and retail sectors have already begun to harness AI’s potential to automate complex tasks, streamline workflow and accelerate technological advancements. Interestingly, Nvidia CEO Jensen Huang says AI smart enough to pass human tests (‘every single test that you can possibly imagine’) could become a reality as soon as five years! We talk more about the skyrocketing success of the tech giant later in this edition. Carl Kawaja, equity portfolio manager of The Growth Fund of America, also points to the significant advancements in pharmaceuticals, with new and improved treatments discovered for a range of conditions including cardiovascular disease, diabetes and obesity. These advances have the effect of not only reducing medical costs as a drag on the economy, but allowing people to be healthier, hence work longer and contribute to the economy. In a world where the media is saturated with bad news about tragic regional conflicts, climate catastrophes and cost-of-living crisis, it is important not to forget that there are also reasons to be positive. |

|

|

|

| We hope our optimism is rewarded, but it’s always important to be aware of risks.

And the latest in our investment risk series is Liquidity Risk. Liquidity risk, in the context of traded markets, the risk of being unable to buy or sell assets in a given size over a given period without adversely affecting the asset’s price. The risk will be significant if, for example, a large trade happens over a short period of time in an insufficiently liquid market. Some investors believe liquidity risk has become worse following the Global Financial Crisis, due to bank capital constraints, with dealers facing higher costs to hold inventories of securities and warehouse risk. An additional concern is that investors crowding into similar trades can lead to mismatches between willing buyers and sellers of certain assets in periods of stress, leading to diminished liquidity and putting further pressure on asset prices. In the context of funding, liquidity risk refers to the ability of institutions to fund liabilities as they fall due without incurring losses through being forced to sell less-liquid assets quickly. Following the GFC, regulation of banks has included focus on addressing mismatches between the liquidity of banks’ assets and liabilities, with banks required to hold enough highly liquid assets to cover liability requirements through periods of stress. This is also important for personal investors. Having cash set aside for regular income, or any unforeseen expenses, avoids the risk of having to sell a quality asset at a depressed price in a down market. |

|

|

The NVIDIA Corp share price has been on an incredible run, as this chart will attest. The surging success of the US tech giant – the world’s leading maker of Artificial Intelligence chips used to create systems like Open AI’s ChatGPT – has seen the stock skyrocket $502 (from $403 to $905) since October 2022! The $2.15 trillion American multi-national continues to be driven by the AI boom and, when you consider it’s just one of the Magnificent 7, you can see how dominant they are as a group. As the Wall Street Journal recently reported, ‘almost 28% of the S&P 500’s gains so far in 2024′ are a consequence of the Magnificent 7. In a recent article in the New York Times, The Economist opined that ‘it seems likely there is a connection between the concentration of value in the US stock market and its increasingly passive ownership’. “The five biggest companies in the S&P 500 now make up a quarter of the index. On this measure, markets have not been as concentrated since the ‘nifty fifty’ bubble of the early 1970s,” it reflected. “Last year the size of passive funds overtook active ones for the first time. The largest single ETF (exchange-traded funds) tracking the S&P index has amassed assets of over US$500b.” It also underscores our critique, made in last month’s View, that the Magnificent 7 are powerful in obscuring the narrowness of performance in the broader S&P 500 stock market. (And if the M7 pull back, they will take the whole index down with them). |

|

|

| That’s the staggering amount Australians are paying each year in surcharges when they pay with their cards instead of using cash, according to analysis of RBA data.

This is partly because the popular “tap-and-go” option at point-of-sale EFTPOS machines will be automatically routed to the more expensive Mastercard or Visa network, according to an ABC News. At a time when many Australians are feeling the cost-of-living squeeze, these ‘hidden’ transactional card costs can really add up. And, given we’re moving towards a cashless society, for many of us they can be difficult to avoid. (Ironic really, that the more we are being directed to electronic commerce – and away from cash – the more we are being charged for the privilege!) The RBA said it will mandate what it calls least-cost routing – a system where payment terminals automatically default to the lowest-cost card network (usually EFTPOS) when processing debit transactions which saves businesses and customers money – if the industry doesn’t meet the 80 per cent uptake target by mid-year. Least-cost routing means payment terminals automatically default to the lowest-cost card network when processing debit transactions, which saves businesses and customers money. In theory, it should put downward pressure on payment costs, and the flow-on effect should be smaller surcharges for consumers. By way of background, in 2003, the RBA began implementing reforms to Australia’s debit and credit card systems, which included the “no-surcharge rule” – which prevented merchants from surcharging for credit card transactions – being removed. The RBA’s website says these rules had masked price signals to cardholders about the relative costs of different payment methods, and they had also “contributed to the subsidisation of credit card users by all other customers, as merchants would build the costs of accepting card payments into the overall prices of their goods and services”.

|

|

|

In this column, we have often referred to Westpac’s (now former) veteran chief economist, Bill Evans, as the “RBA Whisperer”. Mr Evans – who has now moved to the new role of senior economic advisor at the Bank – steered Westpac’s forecasts through a recession, the GFC, a trade war and the COVID-19 pandemic and was the first economist to rightly predict the RBA’s easing cycle in 2011. Meet Dr Luci Ellis – the former Assistant Governor (Economic) at the Reserve Bank of Australia from December 2016 to October 2023 (and hence, a former colleague of the new RBA Governor Michele Bullock) who has now taken over the reigns at Westpac, becoming the first female chief economist at a big four bank. In a video and article “Luci’s Call” published to the Westpac website last month, Dr Ellis says that while the future is uncertain and the RBA is keeping all options open for now, she predicts interest rates will start easing towards the end of the year. “As inflation continues to fall, the labour market eases and consumer spending remains soft, we expect the RBA will gain confidence that inflation will return to the 2 to 3 per cent target band on the timetable they want to see,” she said. “If that happens, they’ll be confident enough to reduce interest rates a little and start softening their contradictory stance. “In our view, that level of comfort for the RBA will be reached around September giving them scope to cut rates a couple of times before the end of this year. “The future is uncertain, and the RBA is keeping all options open for now, but most likely the cash rate will be on hold for some months to come yet.” Westpac is even using the hashtag #luciscall – which it will, no doubt, be hoping will take off as a trending hashtag for all the right reasons in the months, and years, to come. |

|

|

The Albanese government, as you know, is consulting on a reform package to make super funds drastically improve the support they offer older members, in a bid to give retirees more confidence in retirement. Super fund bosses overseeing the $3.6 trillion industry have conceded they have fallen short on preparing their customers for retirement, despite 3.6 million Baby Boomers preparing to leave the workforce in the next decade. It comes as the Association of Superannuation Funds of Australia this week released new data showing surging electricity prices have helped push the annual cost of a comfortable retirement towards $72,000 for a couple and $51,000 for a single. And, contrary to what we’ve been led to believe, it seems retirees may not be underspending in retirement after all. At least that’s according to the newly-formed Super Members Council of Australia – a collective body created by profit-to-member super funds – in its retirement income submission to Treasury, which it says has combined consumer research, super fund data, and analysis of publicly available information. According to several news reports on the submission, the Council found that two in three people are drawing income from their super above the minimum required in retirement and 90 per cent of men and 80 per cent of women have no super left when they reach their life expectancy age. It said that while retirees’ stated ambition is to retire at 67, the data showed that about a third have accessed their super at 63 and about 25 per cent still work into their 70s. The SMC also found that the median balance at retirement was $200,000, while the median working 30-year-old is now expected to retire with $500,000. SMC chief executive Misha Schubert said Australians approaching retirement want more information and advice. “We are on the cusp of a seismic change to retirement… Our submission busts the longstanding myth that retirees are not spending their super.” The Government’s retirement agenda involves 3 pillars:

Good advice is crucial in optimising the right mix of these pillars based on each individual’s objectives. |

|

|

In recent weeks we have been given another fascinating insight into the wisdom, strategy and ethos of Warren Buffett – the so-called ‘Oracle of Omaha’ for his investing acumen – with the highly-anticipated release of his annual letter to Berkshire Hathaway shareholders. The 17-page letter was the first since the passing late last year of Buffett’s long-time business partner, company Vice-Chairman and, as Buffett put it, the “Architect of Berkshire Hathaway”, Charlie Munger. “In reality, Charlie was the ‘architect’ of the present Berkshire, and I acted as the ‘general contractor’ to carry out the day-by-day construction of his vision,” he wrote. “Charlie never sought to take credit for his role as creator but instead let me take the bows and receive the accolades. In a way his relationship with me was part older brother, part loving father.” Buffett wrote that together they followed an investing regime that sought to add ‘wonderful businesses purchased at fair prices’, rather than ‘fair businesses at wonderful prices’’. This approach has been a key factor in Berkshire’s success and has influenced many investors worldwide. He said ‘net earnings’ should be used as a ‘starting point’ only to measure the performance of a business, arguing it alone could be misleading due to its inclusion of unrealized capital gains and losses. Recounting the exact date of his first stock purchase (March 11, 1942), Buffett said America had been a ‘terrific country for investors’ – “All they have needed to do is sit quietly, listening to no one” – and reinforced the importance of patience when investing. AMEX and Coke, he said, had rewarded BH’s inaction last year, by increasing their earnings and dividends. ‘Indeed, our share of (American Express) AMEX earnings in 2023 considerably exceeded the $1.3 billion cost of our long-ago purchase,” he wrote. “The lesson from Coke and AMEX? When you find a truly wonderful business, stick with it. Patience pays, and one wonderful business can offset the many mediocre decisions that are inevitable.” |

|

|

We couldn’t help but laugh when we saw this modern interpretation of the Beatle’s legendary Abbey Road album cover. The Fab Four were photographed on that famous street in north-west London back on August 8, 1969 – almost four years before the first handheld mobile phone was produced by Motorola. Simpler times, pre-Siri. |

|

|