Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View #9

Issue: Friday 29 May 2020

This week the Prime Minister told Australia he wants to “fire the starters’ gun on the economy” in a speech outlining his vision for recovery. While boasting of the fact Australia is “weathering the storm better than many and better than most”, he lamented the fact “millions of Australians” are now relying on a recovery. A recovery that is for now, fuelled by government support.

The worst does seem to be over. Road traffic is returning, retail sales are rising and house auction clearance rates have improved. But what is the definition of a recovery? If recovery means a bounce from the bottom, then we are in a recovery.

But if the definition of recovery is a return to pre-crisis levels of demand, revenue and profits we are a long way off.

The fact of the matter is, stimulus cannot continue to prop up consumers for ever and it won’t be until later in the year that we will have a better idea of the extent to which the recovery is self-sustaining. For now, our view remains a cautionary one. The saying “the best prophet, is the best guesser” (Thomas Hobbes) sums up our capacity to predict the future: We can’t.

However, having no macro economic opinion is not useful either. While we reiterate there is a danger in placing too much weight on current circumstances when assessing the future, in this article Economist Shane Oliver shifts the focus from the short-term impacts of COVID-19 to examine 10 longer term implications. His list includes:

- Lower interest rates for longer

- A further blow to globalisation

- Another leg up in the US/China trade war

- Bigger Government and public debt

- Long-term risk of higher inflation

- Consumer and investor caution

- Faster embrace of technology

- Bad for airlines

- Another test for the Eurozone and

- Lower immigration.

Market Perspectives

Markets are booming even though the full economic toll of the coronavirus remains a mystery. But, this near euphoric rally on global equity markets is based on a fundamental fallacy – the premise that the rebound in Chinese economic growth will be replicated by the West. While the rhetoric test/track/isolate may be the same, with a few exceptions most OECD countries lack the surveillance and quarantine structures needed to carry out a clean exit.

Global virologists are worried. They fear that Europe and the US are dialling down containment measures before the tracking apparatus is fully in place and before the stock of infections has been cut to manageable levels. We are not close to herd immunity and therefore can only presume that leaders are looking to let the virus run its course and hope a vaccine will come along. Donald Trump is certainly angling to do exactly that and a great number of investors seem to be betting on it too.

The rush to reopen is understandable. But as a matter of economics, the notion that we must pick between fighting COVID-19 and reviving growth is misframed. The British authorities have shown that if you get it wrong, you get both the worst death toll in Europe and one of the worst economic hits as well.

There is a strong argument that the next few months will be a messy series of false dawns, carving out a protracted Nike swoosh rather than the Chinese “V” that is currently assumed by equity markets.

The most amazing investing lesson of all

The problem with investing is there are few absolutes. Outcomes depend on human behaviour, it’s not physics or chemistry. In this article first links Managing Editor Graham Hand goes back to basics with a mathematical certainty everyone can play with. There’s more investing learning in a simple formula than any other lesson.

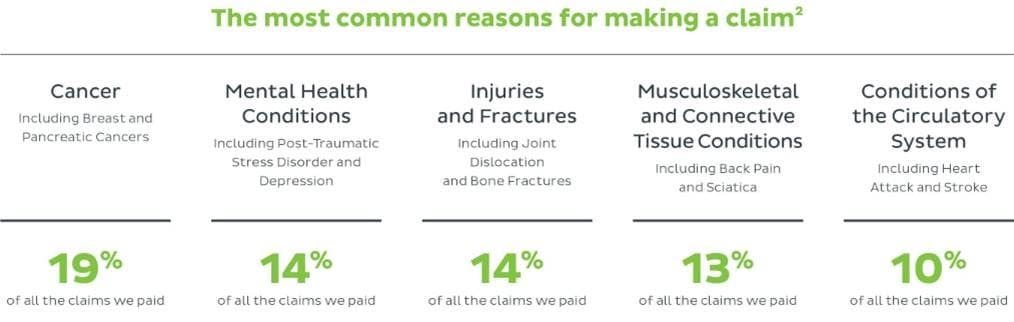

Australia’s broken personal insurance market

What are the most common health reasons for insurance claims? Cancer, heart and musculoskeletal conditions (back pain and sciatica) have dominated personal insurance claims for many years. However, in more recent times, mental health related conditions have spiked dramatically, so much so that they sit just behind cancer as the most common reason for making a claim.

A surge in mental health claims is one of the reasons as to why the insurance industry has collectively lost $4 billion on retail disability income products (also known as ‘Income Protection’ insurance) over the past five years, which is placing significant pressure on insurers to increase premium rates. This, coupled with a recent demand from regulator APRA to increase capital holdings, has seen insurers make significant changes to their products and pricing. One such insurer has just announced that they will be increasing their Income Protection premium rates by over 35%.

We strongly encourage you to reach out to your adviser to discuss your personal insurance options, whether you have policies with us or elsewhere. There are ways to limit these enormous premium increases.

2019 data from TAL

Things that make you go ‘mmm…’

When the market goes up or down it has an effect on pensioners with share-based investments, such as superannuation. It stands to reason therefore that Pension payments should be adjusted to account for a drop or increase in the value of assets. And, yes this is exactly what happens.

However, it has recently come to our attention that whilst Centrelink need to be notified when asset go down, they seem all to aware when they go back up again. It makes one wonder…

Tread Carefully Before Giving Adult Children Financial Help

A thought provoking article in the Fin Review from Louise Biti of Aged Care Steps on the perils of loaning or gifting money to your adult children who may have been financially impacted by the lockdown. The message is ‘tread with care’ as gifts and loans can impact your age pension entitlements, can affect their ability to access hardship payments and may cause future estate challenges (a topic close to our hearts that you can expect to hear more about very soon). Please speak to your adviser before gifting.

Read article here (requires a subscription)