Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A FinSec View #17

Issue: Friday 18 September 2020

‘The Show Must Go On’ …

As residents of #10 Greenhill Road, the middle of September represents show week and our cue to escape as a team for our annual business planning. This year (the first time in 100 years of The Royal Adelaide) the Ferris wheel did not turn, the show bags were regulated to supermarket shelves, and the silence (as a business, it is a noise we often begrudge) was deafening in its absence. But.. the show must go on.

In FinSec terms this meant two constructive days away from the office as a team, workshopping our processes, client journeys and planning out the year ahead. The next 12 months promises to be an exciting one, and we look forward to sharing the outcomes with you, as we implement some new and exciting initiatives over the forward period.

The middle of September also signifies the last weeks of JobKeeper (1.0) bringing with it the much anticipated ‘September cliff’. From 28 September, JobKeeper falls from $1,500 to $1,200 a fortnight for those actively engaged in the business for 80 hours or more a month and to $750 for all others. Businesses will take on more administrative and compliance complexity.

The stimulus enjoyed by many companies from the initial government money dump (a part-timer on $100 a fortnight was suddenly eligible for $1,500) is about to hit a wall.

Stimulus was also front and centre, as the results of Australia’s main reporting season (August) came in. A sea of red ink in corporate profits and dividend announcements was offset by optimism that corporate profitability will be restored, propped up by innovative and expeditious government support.

Although the August reporting season for Australian listed companies was the worst since 1931, it provided very few negative surprises and a significant number of positive ones. Despite many companies reporting in the red, there were no major negative developments and no flood of corporate bankruptcies.

- Revenues were virtually flat (around the same as last year)

- Profits were down (in-line with forecasts from earlier this year)

- Dividends were down, mostly the big banks (account for 35-40% of dividends), also flagged earlier this year.

Several companies posted revenues, profits and shareholder dividends (all propped up by the next generations tax burden!).

The August reporting provided the first comprehensive opportunity we have had to properly understand the effect of the COVID related shutdowns. The data does support our previous assessment (as penned in many a view) that thus far, the combined impact of efforts to contain the virus, prop up income with deficit spending programs, plus support from central banks to keep interest rates low (keeping the bond markets liquid so governments can finance their debt) seems to have done the trick in preventing the flood of red ink from worsening. This, in turn, has supported share prices.

What lies ahead?

The medical crisis is far from over, with no vaccine in sight. The assumption that corporate profits have bottomed rests on the hypothesis that further lock-downs will either be short and/or targeted. If not, and we are forced back into a more restrictive, widespread lock-down, then it is probable that governments will continue their support packages which in turn will reap the same flow through to companies and shareholders. The other unknown is of course how many ‘zombie’ companies there will be once the ride (JobKeeper) is over.

A Note on Markets

The ASX has stumbled home to end the week 18.7 points (0.3%) down at the close, a contraction that is off the back of profit taking in US tech stocks. In doing so the market has narrowly avoided recording five consecutive weeks in the red – a stat that hasn’t happened in four years – as it edged 5.1 points higher over the course of the five sessions.

The Weak Link Between Profits and Shares

The past few months have exacerbated a trend we have been touting with concern for some time now.

The huge expansion of government balance sheets, triggered by COVID has enabled market ‘favourites’ to reach new dizzying valuation heights that are seemingly disconnected from the real economy. Government largesse means that despite the fact that the global economy is presenting few growth prospects, we are seeing profit forecasts that would be unconvincing even in a booming economy.

Playing the share market has become less about companies with great revenue and profit growth potential, and far more about forecasting, which stocks the market will fall in love with in the future.

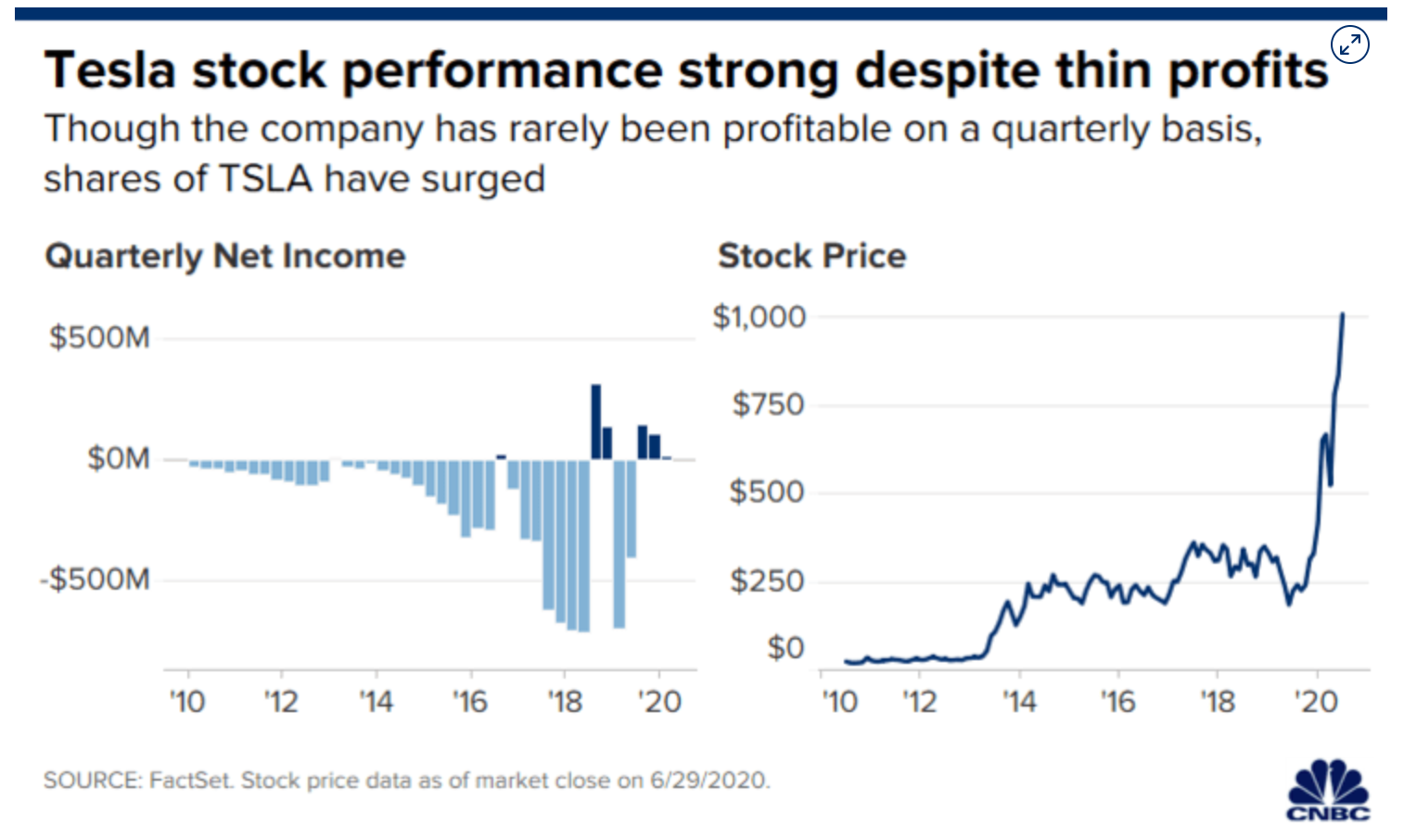

Take Tesla.

Tesla’s share price is up an electrifying 4000+% since its IPO ten years ago – this includes an increase of close to 200% this year alone.You might (logically) assume that its sales and profits have grown by a similar amount? You might assume that. But you would be very wrong. The truth is Tesla has never made a profit.

This is not suggesting that Tesla is a bad investment, but rather highlights the weak link between profit and shares that can occur. Leading to an environment in which the share price alone creates the appeal, not the underlying value creation.

It is worth acknowledging here that the share market is pricing in profits two years ahead. Even so, it is an audacious goal for Tesla to achieve…

At FinSec we continue to believe that fundamental value creation happens slowly (this will never result in 200% share price gains in a year). Our role is to protect our investors’ hard earned capital, and we do not achieve this by chasing growth with nothing to support it.

We remind investors that history has shown, time and again, that all bubbles burst and growth cannot continue into perpetuity.

The SG debate has it been good enough?

In the last month we have seen the Superannuation Guarantee (SG) rachet up in terms of toxicity. There have been personal attacks and heated arguments as both sides scramble for a populist high ground that everyday Australians can relate to.

With superannuation touted as the solution to every problem, it was refreshing to see an article in this week’s publication of Professional Planner providing a more measured perspective.

Publisher and author Colin Tate points out that the primary purpose of super is to provide retirees with the ability to fund some or all of their retirement (a fact that is embedded in the legislation itself, as the sole purpose test). All other items e.g. the support of projects which create jobs, while important, are secondary.

With this in mind, he challenges if the debate has been good enough?

“Have the arguments acknowledged the full household balance sheet including age pension entitlements? Have all policy levers beyond the level of the SG been considered? Has the research considered the effectiveness on different cohorts of the population and the value-for-money of government spend? Filter the various proposals through these lenses and ask yourself how many would make it through.”

Much has changed since the SG was introduced; age pension, life expectancy, aged care, housing affordability, interest rates and the tinkering of super rules themselves. Groups even argue that a higher SG is the solution to the labour/wages share of National income (currently at a 60 year low).

These are all important social issues, however super is but one tool in the box.

Fearing that we may have created a binary debate (9.5% or 12% SG), while the middle option rarely gets a mention, sensibly Tate suggests a pause “until we see the crisis settle and how Australia’s economy, fiscal situation, corporate sector and house-holds are all placed”. He encourages both sides of the debate to park their vested interests, respect the Review and allow due process to take its course.

Chart of the week

This week’s chart of the week looks at the impact liquidity has on share prices. ‘Liquidity’ is fuelled by zero interest rates and central bank bond buying (QE).

In one adviser note we read this week, liquidity was likened to morphine. ‘Great if used sparingly and only in case of emergency, but overuse desensitises the patient and can cause nasty side effects. Always read the label.’