Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 23rd June 2017

Investment markets and key developments over the past week

- Global shares mostly rose over the last week, despite falls in energy shares, as economic data was mostly good and there was good news for Trump’s pro-growth agenda in the US. US shares rose 0.2%, Japanese shares rose 1%, Chinese shares rose 3% but eurozone shares lost 0.3%. Australian shares fell 1% thanks to a combination of falling oil prices hitting resource stocks, “fear of Amazon” weighing again on retailers and worries that China’s inclusion in MSCI share benchmarks will see funds flow out of Australian shares. Bond yields were flat to down, the plunge in the oil price continued and this along with a slightly stronger US$ weighed on the A$.

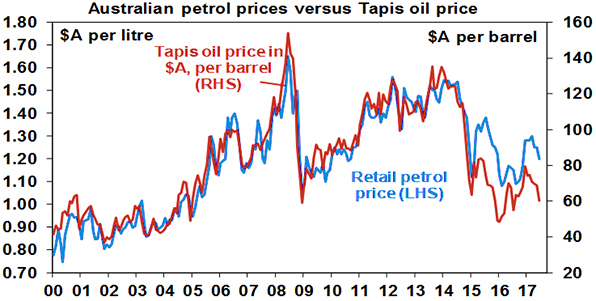

- Oil price plunges, inflation still MIA, interest rates to remain low, good news for Australian consumers. The oil price has been trending down since February amid concerns that rising non-OPEC production will offset OPEC production cuts. This hit the headlines over the last week as the decline pushed beyond 20%. While oil is oversold and sentiment towards oil is so negative it’s hard to get too excited. Particularly with steadily rising shale production in the US putting a cap on price upside. More broadly, the weak oil price highlights the broader lack of inflationary pressure globally which will keep interest rates low. Low oil prices, however, mean low petrol prices and this is positive for consumers. In Australia, if current oil prices are sustained the retail price of petrol could fall towards $1.10 a litre. This implies a saving for the average family’s weekly petrol bill of around $6 compared to January.

Source: Bloomberg, AMP Capital

Which is good news given the self-inflicted wound flowing from higher electricity prices in Australia. And if oil prices stay low or fall further it will mean lower gas export prices which could take pressure off the domestic gas market.

- The inclusion of Chinese mainland (or A) shares in MSCI’s share benchmarks is another sign of the opening up of the Chinese share market and its integration globally, but it has a long way to go. The inclusion only relates to large cap shares accessible by foreigners via the Hong Kong share connection. Initially the weight of Chinese shares in the MSCI emerging market index will be just 0.7% whereas right now the Chinese share market is 9% of total global share market capitalisation and it won’t start phasing in until May next year. Full inclusion may take 5-10 years. And the initial index related flows into the Chinese share market from the move are likely to be less than half the typical daily turnover in the Chinese share market. So don’t expect a huge short term impact. However, the impact on Chinese shares will grow over time as the exposure in the MSCI indexes is likely to rise. It’s also another sign that China is now becoming an integral part of the global financial system. Over time the increasing participation of foreign institutional investors will help enhance the rights of Chinese shareholders, add to the liquidity and reduce the speculative tendencies in the Chinese share market.

Major global economic events and implications

- While the noise around President Trump continues to swirl, the past week confirmed that his policy agenda remains on track, with the Senate having released its draft Obamacare reform bill, Treasury Secretary Mnuchin and House Speaker Ryan confirming tax reform remains a top priority, a draft executive order on the health industry focussing on easing in regulations and Republican election victories all providing impetus to Trump’s agenda. On the data front home sales, home prices and the leading index rose and jobless claims remain ultra weak but the Markit business conditions PMIs fell slightly in June despite strong new orders. Major US banks also passed the first stage of the Fed’s latest bank stress tests, as would be expected in this environment.

- Eurozone consumer confidence rose to its highest in 16 months and French business confidence rose to a 6 year high. Against this the composite business conditions PMI fell slightly in June, albeit it remains strong.

Australian economic events and implications

- ABS home price data confirmed continued strength in the March quarter but a lot has happened since then with bank rate hikes for investors and interest only borrowers, tighter lending standards and evidence the Sydney and Melbourne property markets have started to cool. Skilled vacancies remained strong in May pointing to continued solid jobs growth for now.

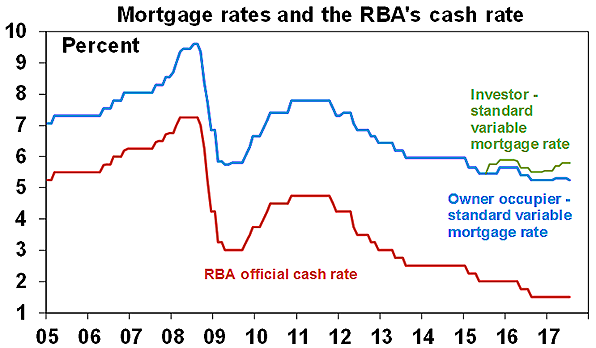

- More bank mortgage rate hikes, but cuts for owner occupiers paying principle and interest. The drip feed of bank rate hikes has continued but it’s worth putting this in perspective. Reflecting regulatory pressure and banks managing their risks the rate hikes have been for investors and more recently for interest only (IO) borrowers. See the chart below.In the last week banks have been cutting their variable rates for owner occupiers on principle and interest (P&I) loans. (Note that the chart below relates to standard variable rates, the discounted rates are around 0.75% lower). While the hike in investor and interest only rates (of around 0.3% for investor P&I loans, 0.75% for investor IO loans and 0.5% for owner occupier IO loans since November) are a dampener, they are modest compared to past rate hiking cycles, investors can get up to half of it back from the tax man and nearly 80% of owner occupiers are on principle and interest loans and many of them have seen a small rate cut over the last week.

- The main uncertainty relates to the impact on interest only owner occupiers and the threat in terms of repayments as they move across to P&I and its effect on overall economic growth. However, if this problem becomes a reality then the RBA can simply offset the increase in mortgage costs by cutting the cash rate again (and yes for owner occupiers it’s likely the banks would pass it on).

Source: RBA, AMP Capital

- News that South Australia will add to the Federal Government’s bank levy adds to concerns that a Pandora’s box has been opened. It’s understandable that businesses will fear that if they are in an industry that does well (and is unpopular) then they will be hit with a higher tax rate. Good tax policy seeks to minimise distortions with a single tax rate across all industries and we seem to be moving away from that.

What to watch over the next week?

- US data to be released in the week ahead will provide an update on business investment, consumer confidence and the US Federal Reserve’s (Fed) preferred measure of inflation. Expect underlying capital goods orders (Monday) to show a further improvement, consumer confidence to have slipped a bit but remain strong with home prices continuing to rise (both Tuesday), pending home sales (Wednesday) to rise, May consumer spending growth (Friday) to be a bit soft and inflation as measured by the core private consumption deflator (also Friday) to fall further to around 1.4%. The combination of which will probably keep the Fed on a tightening path but only gradually.

- Eurozone consumer and business confidence readings (Thursday) are likely to show continued strength consistent with stronger growth, but core inflation (Friday) is likely to remain weak and below target at around 1% year on year.

- Japanese data to be released Friday is expected to show continuing strength in labour market indicators (helped by a falling workforce), continued strong annual growth in industrial production and continuing weakness in inflation with core inflation remaining around zero.

- Chinese business conditions PMIs (Friday) will also provide a look at how growth is holding up in June. Expect the official manufacturing PMI to remain around 51.

- In Australia, expect job vacancies for May to have remained solid consistent with ANZ job ads, new home sales to show a continuing gradual downtrend (both Thursday) and credit growth (Friday) to have remained modest with most interest likely to be on whether the rate of growth in property investor credit is continuing to slow.

Outlook for markets

- Shares are still vulnerable to a short term setback as we go through a weaker seasonal period for shares, with risks around Trump, North Korea, Chinese growth, the Fed and the Australian economy all providing potential triggers. Valuations however remain okay particularly outside of the US, global monetary conditions remain easy and profits are improving on the back of stronger global growth, so it is likely to see the broad 6-12 month trend in shares remaining up.

- Low yields point to low returns from sovereign bonds.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the ongoing search for yield, but this will wane eventually as bond yields trend higher.

- National residential property price gains are expected to slow, as the heat comes out of Sydney and Melbourne.

- Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.5%.

- Our view remains that the downtrend in the A$ from 2011 will resume this year. The rebound in the A$ from the low early last year of near $0.68 has lacked upside momentum, the interest rate differential in favour of Australia is continuing to narrow and will likely reach zero early next year (as the Fed hikes rates and the RBA holds or cuts) and commodity prices will also act as a drag (particularly the plunge in the iron ore price). Expect a fall below $US0.70 by year end.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer