Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A better 2014 for the Australian economy and profits

Introduction

Ever since major mining investment projects, such as Olympic Dam, started to be cancelled over a year ago and it became clear the mining investment boom was coming to an end, much uncertainty has surrounded the outlook for the Australian economy. This was not helped by a mediocre initial response to interest rate cuts and sub-par growth of around 2.3% annualised since the June quarter last year.

Despite the economic uncertainty the Australian share market has lifted strongly – up 35% from 2011 lows – with many fretting the market has got ahead of itself given the weak economic backdrop and falling profits. Our view has been that the share market usually leads the economic cycle. So just as the 22% slump in Australian shares between April and September 2011 anticipated the slowdown in growth and profits seen recently, the rebound in the market over the last two years is in anticipation of stronger growth and profits ahead. This has been helped along by the fall in interest rates (which is positive for profits and helps drive investor flows back into shares), the decline in the $A and an improved global growth outlook. But with shares no longer cheap, we are now at the point where the economy and profits need to start confirming the share market’s optimism. Will the market be right?

Growth still well below trend…

September quarter GDP data didn’t provide much cause for optimism, but then again it wasn’t expected too either. GDP growth came in at 0.6% quarter on quarter or 2.3% year on year. This is poor for a country where potential growth is around 3 to 3.25%. The sub-par figures reflect modest growth in consumer spending, weak investment and falls in inventories but helped by a boost from net exports (or trade).

…but there are some grounds for hope

While there remains a bit of short term uncertainty, there are grounds for optimism that economic growth will improve through next year. Specifically:

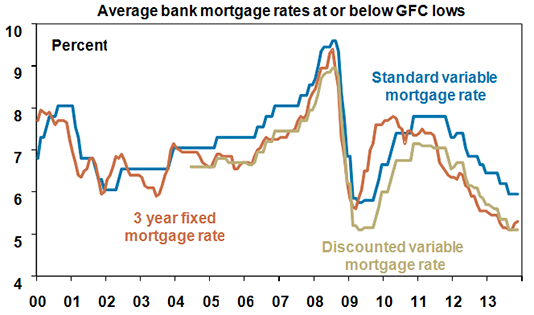

- Interest rates have fallen to past cycle lows. This means huge savings for the key demographic responsible for marginal consumer spending in the economy – those with a mortgage. For a family with a $250,000 mortgage the annual interest saving versus the rate peak two years ago is about $5000. Eventually some of this will be spent.

Source: RBA, AMP Capital

- The $A is down 15% or so from pre May average levels.

- Household wealth is up over the last year reflecting the rising share market and rising house prices.

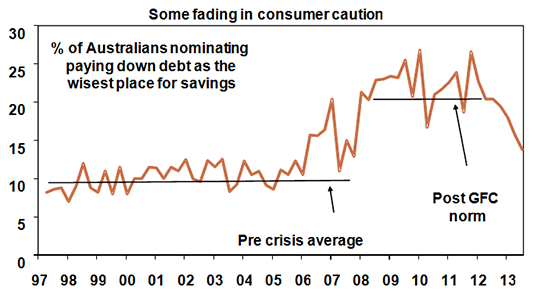

- Household caution seems to be fading. The proportion of Australian’s nominating paying down debt as the “wisest place for savings” has fallen to its lowest since 2007.

Source: Westpac/Melbourne Institute, AMP Capital

Reflecting this there are some good signs:

- A solid recovery in housing construction appears to be getting underway. Approvals to build new homes are pushing up towards past cyclical highs.

Source: Bloomberg, AMP Capital

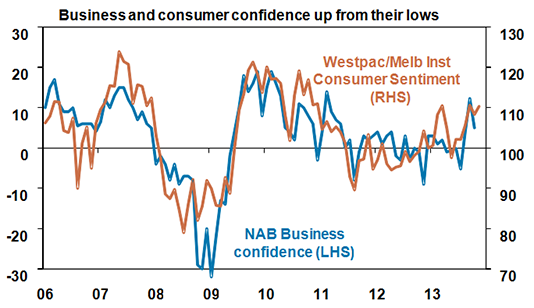

- While the recovery has been more gradual than normal, consumer and business confidence are well up from their lows of a year or two ago and seem to be trending up.

Source: Westpac/MI, NAB, Bloomberg, AMP Capital

- The combination of improved confidence, rising wealth and rising housing construction is likely to drive a recovery in retail sales growth over the year ahead. This should see nominal annual retail sales growth break out of the 2-3% range it has been in for the last four years and move up to around a 4-5% pace in the year ahead. This may already be underway with retail sales showing improved growth over the last six months and annual growth picking up to 3.6%.

- The latest survey of investment plans for 2013-14 indicated that while mining investment has likely peaked, the overall outlook has improved a touch reflecting an improvement in non-mining investment. Three months ago investment intentions were pointing to a 1% slide in investment this financial year. Now they are pointing to a 1% gain and most of the turnaround is due to investment outside of the mining and manufacturing sectors. In fact investment in what the Australian Bureau of Statistics calls “other selected industries” (mainly services, which is six times as big as manufacturing investment) is now expected to expand 3% this financial year versus a 3% contraction indicated three months ago.

- Finally, it should be noted that while mining investment is likely to trend down going forward, its impact on economic growth will be partly offset by reduced mining related capital goods imports and a pick-up in resources exports as new projects start producing.

More significant fiscal cutbacks likely to be announced in the May Budget will act as an additional drag on growth next year. As a result interest rates need to stay low and the $A ideally needs to fall further to aid in the recovery process. But the indicators above suggest that a sustained improvement is gradually coming into sight. Through next year we see GDP growth picking up to around a 3% pace. In the absence of fiscal cutbacks it will likely be stronger.

If this occurs as we expect then the RBA will probably hold the cash rate at 2.5% through most of next year, ahead of an eventual rate hike later in the year (around September/October).

Profits should start to pick up

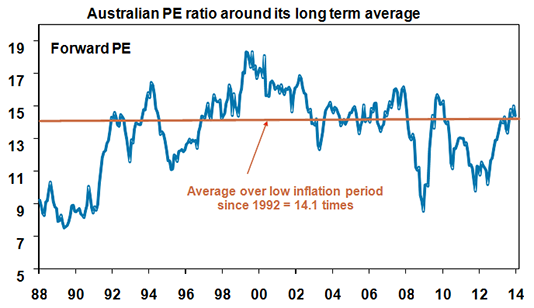

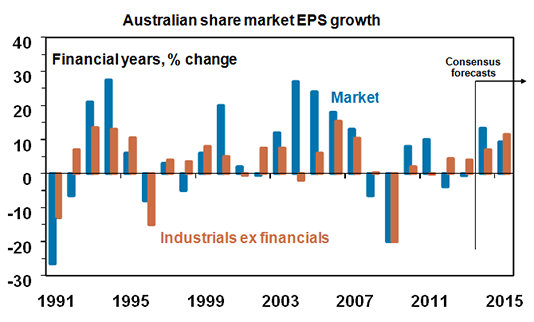

As alluded to earlier the recovery to date in the share market has come via what is often called multiple expansion (ie a rise in the price to earnings multiple) as profits have been weak. This is often the case during the initial recovery phase in the share market as the market cycle leads the economic cycle. However, as the price to forward earnings ratio, currently at 14.4, is now around long term average levels of 14.1 times (over the last 20 years), profits need to start picking up in the year ahead. See the next chart.

Source: Bloomberg, AMP Capital

Otherwise there is a risk the market rebound will start to falter or will become increasingly driven by a “chase for yield” which would ultimately leave it vulnerable.

Reflecting tough economic conditions, the last two years have seen falls in profits for the market as a whole. This has particularly been the case for resources which have been hit by weak commodity prices and cost blow outs associated with investment. The market ex resources has actually seen modest growth after four pretty terrible years (2008-2011) led to a renewed focus on cost control. See the next chart.

Source: UBS, Deutsche Bank, AMP Capital

For 2013-14 consensus earnings growth expectations are around 13%, made up of a 35% gain for resources and 8% growth for the rest of the market. For 2014-15 earnings growth expectations are around 9%. While the 2013-14 consensus earnings estimates could prove to be a few percentage points too optimistic, earnings are likely to rise 8 to 10% over the year ahead. Resources profits are likely to see a strong gain reflecting the resilient iron ore price, the lower $A and reduced cost pressures.

For the market ex resources, a pick up to 8% earnings growth through next year is likely to be supported by the pick-up in economic growth that we anticipate. This will drive stronger revenue growth at a time when the large scale cost cutting of the last two years will result in strong leverage.

This should see profits take over as a key driver of the share market. While returns are likely to slow after two strong years and the risk of a decent correction is high, taken together with the combination of still okay valuations, 8-10% earnings growth and still very low interest rates points to further gains in the Australian share market in 2014. We anticipate the Australian share market to have reached 5800 by end 2014.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist

AMP Capital

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.