Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Jackson Hole, a cartoon rock, best & worst performers and more…

Issue: 3rd September 2021

Next Thursday, the FinSec team head off for our annual offsite. In FinSec terms, this means two constructive days away from the office as a team, workshopping our processes, improving on our client journeys and planning out the year ahead.

As our offices back onto the showgrounds, normally, offsite is an escape from the hustle and bustle of show week. But, for a second year running there will be no show and showbags are once again relegated to supermarket shelves. It is sad to see such an iconic event cancelled, but in the context of what our Eastern seaboard friends are having to endure it is a small price to pay.

This week Australians in lockdown were delivered the significant admission that COVID-zero is not going to be possible. An acknowledgement that the pandemic is now ‘endemic’ brings new considerations: what number of daily cases can we ‘live with’? How do we balance that with the inevitable strain on the hospitals and the deaths that will occur?

Given many states in Australia remain relatively COVID-free, these are vexed questions indeed.

Interesting to read what the rest of the world thinks about Australia’s efforts during COVID-19. This is The Economist on 28 August 2021.

“Early in the pandemic, Australia appeared a shining success story. By closing its borders, tracing contacts and rigidly enforcing quarantine restrictions, its “covid zero” strategy seemed to be working. (Geography helped, too: it is easier to keep a virus at bay on a remote island than in a country with long land borders.) The Delta variant has ended that strategy. As one doctor in Melbourne noted, even if contact tracers find an infected person within 30 hours, that person’s contacts would already have passed the virus down several chains of transmission. The country is now putting its hopes in vaccines, and will allow cases to rise as long as hospitals can cope.”

It’s a fair summary as we get within striking distance of our vaccination targets and a gradual acceptance that we will need to live with the virus.

As a consequence of the lockdowns, Australian GDP growth slowed in the June quarter but to a stronger than expected +0.7%qoq. For the September quarter, we are expecting reports of around a 4% contraction.

While it may feel that there is lots of gloom around, many Economists believe that there remains a strong reason to be optimistic regarding economic growth in 2022. The vaccines seem to be effective in helping prevent serious illness; Australia’s vaccination rate has increased dramatically; pent up demand will help drive recovery, and global growth is likely to be strong.

AMP Chief Economist, Shane Oliver’s views on the topic can be found here.

Jackson Hole Symposium

All eyes were on the Jackson Hole Symposium last Saturday when the Federal Reserve Bank of Kansas City held its annual Economic Policy Symposium.

The symposium has been held for more than three decades and brings together central bankers, private economists, academics and policymakers from around the globe. The main speaker is traditionally the US Fed Chair, and asset managers with trillions under their control hang on their every word, listening for the slightest hint of a policy change.

Powell did not disappoint, indicating the Fed will remain cautious in any eventual decision to raise interest rates as it tries to nurse the economy to full employment.

“We have said that we will continue to hold the target range for the federal funds rate at its current level until the economy reaches conditions consistent with maximum employment, and inflation has reached 2% and is on track to moderately exceed 2% for some time,” he said. “We have much ground to cover to reach maximum employment, and time will tell whether we have reached 2% inflation on a sustainable basis.”

On the potentially imminent decision to begin reducing its $120 billion in monthly bond purchases, Powell said he agreed with the majority of his colleagues that a bond taper could be appropriate this year. However, he was also quick to articulate that this should not be indicative of a rate hike.

“If the economy evolves broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year… The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest rate liftoff, for which we have articulated a different and substantially more stringent test.”

Not surprisingly, markets rallied strongly after his speech.

Our View

Powell’s emphasis on the uneven nature of the economic recovery, the further strides needed in employment, and the risks that come with prematurely tightening policy help maintain the Fed’s flexibility to proceed more slowly, especially if delta-related concerns become more prominent. As one article in the Financial Review put it, “the chairman’s high-wire balancing act was on full display”.

There is no doubt that this ‘steady as you go’ stance will put many investors’ minds at ease. To date, Powell and his central bank colleagues, backed by their governments, have rescued economies from a COVID-inspired collapse, and in so doing, boosted asset prices to all-time highs. There is much in this speech to give confidence that the Fed will do the same thing again if need be.

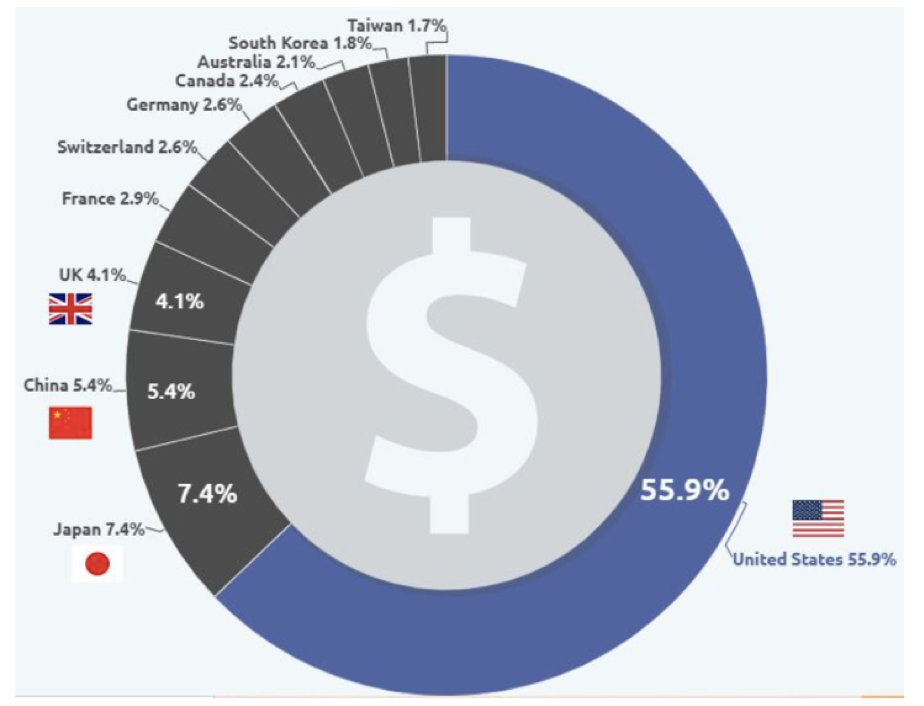

Chart of the week

Ever wondered about the sizes of the world’s stock markets? The US might be the home of bad coffee and ‘french fries’ for breakfast, but it makes up over half of the global stock market. Comparatively, with a market cap of less than US$2 trillion, Australia comes in at a tiny 2.1%. As the old adage goes, no wonder when the US sneezes Australia catches a cold.

NFT – Emerging artform or the internet’s latest craze?

There’s nothing like an explosion of blockchain news to create investor hype. The latest headliner is NFTs.

NFT stands for non-fungible token, a digital asset that is unique and can’t be replaced with ‘like for like’. For example, a bitcoin is fungible — trade one for another bitcoin, and you’ll have exactly the same thing. A one-of-a-kind painting, however, is non-fungible. So if you traded it for a different painting, you’d have something completely different.

In the case of NFTs they signify ownership of a virtual item that represents a real-world object like art, music, in-game items, and videos. The trending view is that NFTs are an evolution of fine art collecting, only in digital terms. Mmm… if you were thinking that anyone can copy a digital file as many times as they want, including the art that’s included with it, then you’d be right. What you are paying for with an NFT is a digital certificate of the item, unique because it has been signed and verified by the creator (a glorified autograph by any other name?).

Helping NFTs to gain notoriety is a long list of recent high-profile sales. Including a cartoon rock that went for US$1.8 million (pictured below), Twitter founder, Jack Dorsey’s first ever tweet selling for just under US$3 million and a Beeple image that was auctioned off at Christie’s for US$69 million, which, by the way, is US$15 million more than Monet’s painting Nymphéas sold for in 2014.

A total of US$897 million in NFT sales were recorded during the 30 days up to 18 August, according to the most recently available data from the NFT tracking site NonFungible.

Rest assured, NFTs will not be on the FinSec Investment Committee’s agenda anytime soon.

Best and worst performing super funds

It has been a huge week for large superannuation funds and trustees, with APRA releasing its performance list under the Your Future, Your Super legislation.

The Government’s Your Future, Your Super reforms (the YFYS reforms) came into effect on 1 July 2021. The reforms require the superannuation industry to improve its efficiency, transparency and accountability.

As commented in previous Views, when considering the scoreboard, it is important to be mindful of the context and purpose of the report.

This report refers to the performance of the “MySuper” funds promoted by both the retail and industry fund community and is designed to ensure that people are aware if their fund is under-performing but also to ensure that the fund trustees are held accountable through greater transparency and consequences.

Most fund promoters offer a suite of options for members, and whilst some members choose to be in the “MySuper” option, most are in this option by default as they have not made a choice as to the fund or the investments they hold.

Unfortunately, people often identify with the brand names of the fund promoters rather than the underlying funds, which creates confusion.

Brands like BT, Asgard and Colonial First State have funds that have appeared on the underperformers list. However, these companies also offer superannuation administration services (wrap accounts) for investors who in collaboration with their advisor, are more proactive with their underlying investments and have discrete portfolios based on their personal situation. Unfortunately, because of the branding, these wrap accounts are often confused with the “Mysuper” accounts when these results are issued.

If you are unsure of your situation and are concerned about whether you are in one of the underperforming funds, please do not hesitate to contact us for clarification.

Previous commentary on the subject can be found here.

Silver lining for UK pensions

As investors wait for future moves from the US Fed and/or the RBA to lift interest rates, this could be the best time for those with a UK defined-benefit (final salary) pension to consider a transfer to the Australian super system.

Low UK Gilt Rates (UK government bond rates) have inflated transfer values exponentially. Traditionally we have seen 15-25 times annual pension as the Cash Equivalent Transfer Value (CETV). Over the last 12 months, we have seen multiples in the range of 30 – 60 times.

Whether it makes sense to transfer will depend on your personal circumstances, and a specialist adviser is best placed to help understand the options.

If you have a friend or family member that has worked in the UK or migrated to Australia, it is well worth sharing this information with them.

A range of information regarding UK Pension Transfers, including eligibility, can be found by clicking here.

Interestingly…

Gilt-edged securities is a term that has come to mean ‘safe and secure’. Its origins, however, refer to the debt securities issued by the Bank of England on behalf of His/Her Majesty’s Treasury, whose paper certificates had a gilt (gold leaf) edge. Today, they are known as gilt-edged securities, or gilts for short.

Congratulations Ahmed!

In the last View, we spoke of ‘friend of FinSec’ Ahmed Kelly. Representing Australia in his third Paralympics, last week Ahmed swam the race of his life to win silver in the men’s 150M medley. Following in third place was his best mate and fellow Australian swimmer Grant ‘Scooter’ Patterson.

Congratulations Ahmed, we know just how hard you have worked for that medal and couldn’t be more proud of your achievements.

An inspiration to us all, in this short video, Ahmed tells us a little of his journey in the lead up to Tokyo 2020.

Quote of the week

“My ventures are not in one bottom trusted, nor to one place; nor is my whole estate, upon the fortune of this present year.” The Merchant of Venice

Apparently, as far back as 1598 Shakespeare was well versed in the art of diversification…

Source: Getty Images

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.