Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – Economy, Markets, Super and Federal Budget

Issue: Friday 16th April 2021

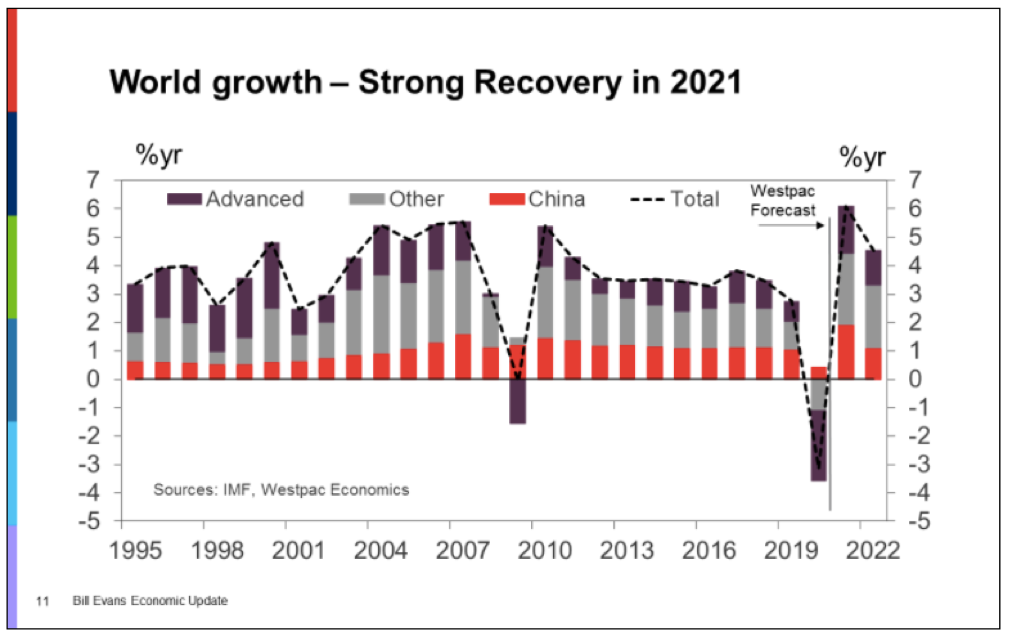

At the risk of sounding like a broken record… ‘we are in an economic environment never seen before’. Global equities trade near record highs, in Australia the property market is explosive, consumer and business confidence is at a 10 year high, and our economy is growing faster than ever. And it’s not just Australia. Globally, experts are now forecasting 10% economic growth in just two years.

Free money is compelling indeed!

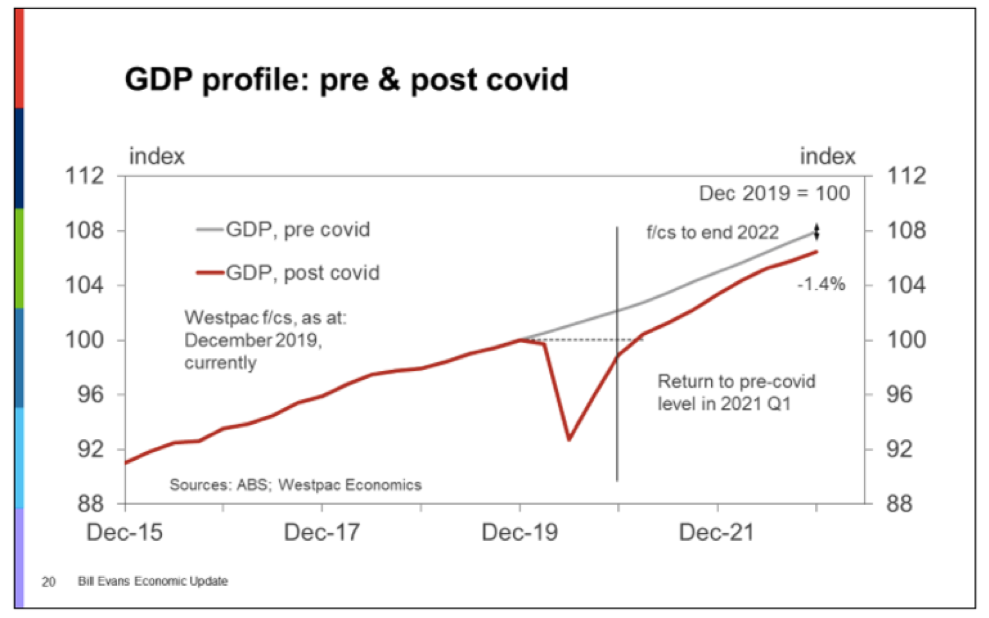

In Australia, activity is back to pre-COVID levels (red line in chart below). Not quite at the level we thought we’d be before we knew COVID was a thing (grey line). However, this gap represents the spare capacity needed to maintain the downward pressure on inflation and wages in the short term.

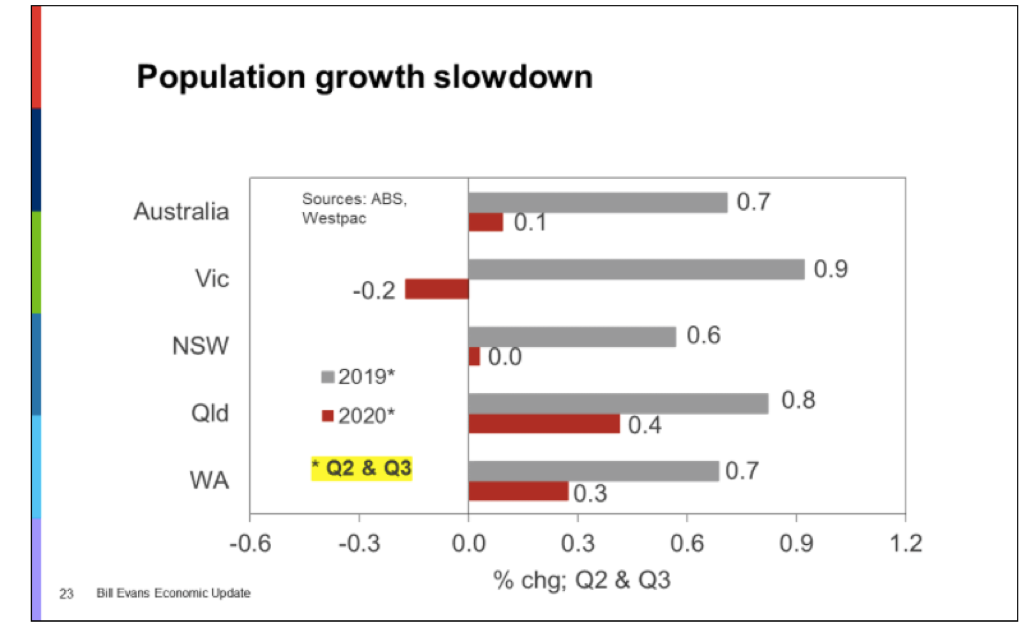

What’s really interesting is the disparity across the states. The recovery outside of NSW and Victoria has been much more rapid. And, when we look at population growth (a key indicator of economic growth), we can see where the pain was felt. In 2020 both NSW and Victoria suffered the heaviest from intrastate migration (people moving away from the big cities) and the impact of closed borders on foreign migration.

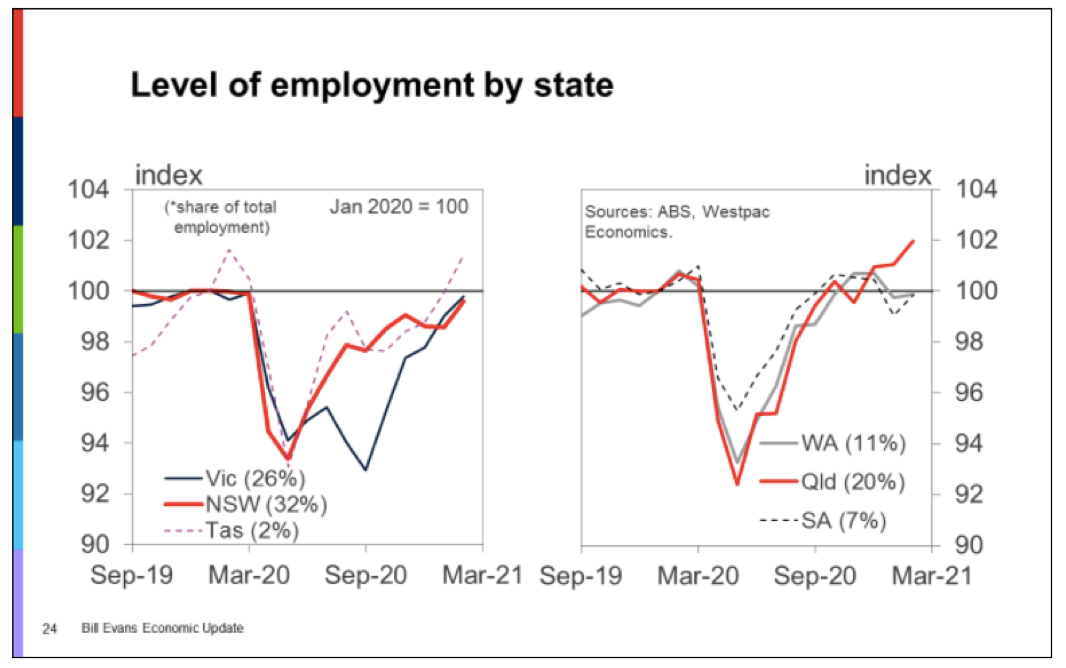

The same story has also played out in Labour markets. Spectacular recoveries in all of the nation but relatively stronger recoveries in the smaller states.

The big driver of the economy is, of course, our propensity to spend.

Across Australia, we have seen unprecedented rises in Household savings over 2020 as significant portions of government payments were saved (refer The FinSec View). Add closed borders, and we have forced savings of a different kind. In 2019 Australians spent $55 billion offshore, compared to around $25 billion that foreign tourists spent in Australia – an extra $30 billion per year we can hope to see spent domestically. All hail the mighty consumer!

With similar stories unfolding across the globe, what does it mean for equity markets?

Firstly, we must recognise there have been huge divergences within markets. On one side, we have companies that were significantly hurt by the events of 2020. Their stock prices plummeted and are/will rebound in line with the recovery, e.g. commodities and travel.

On the other side, we have the companies investors have pursued with unwavering aggression – Companies in e-commerce, software, payments, electric vehicles and renewable energies. This part of the market has been gripped by speculative mania, with plenty of evidence to support this claim:

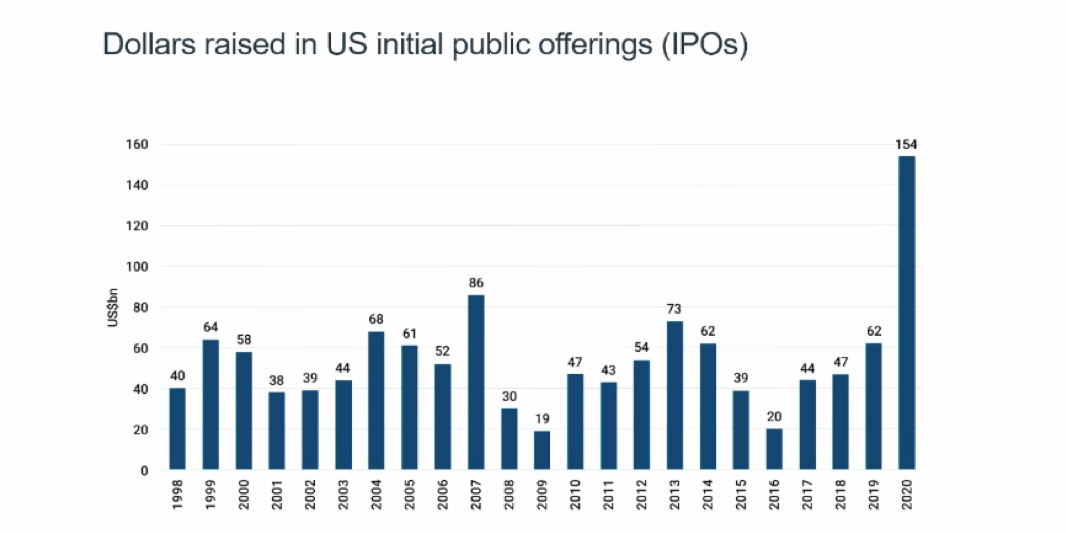

- The huge supply of initial public offerings coming to the market and the incredible performance of these companies on day one of trading.

- High levels of retail investor activity in the options market that is perhaps best exemplified by the short squeeze GameStop engineered by the Wallstreet bets on Reddit (refer The FinSec View).

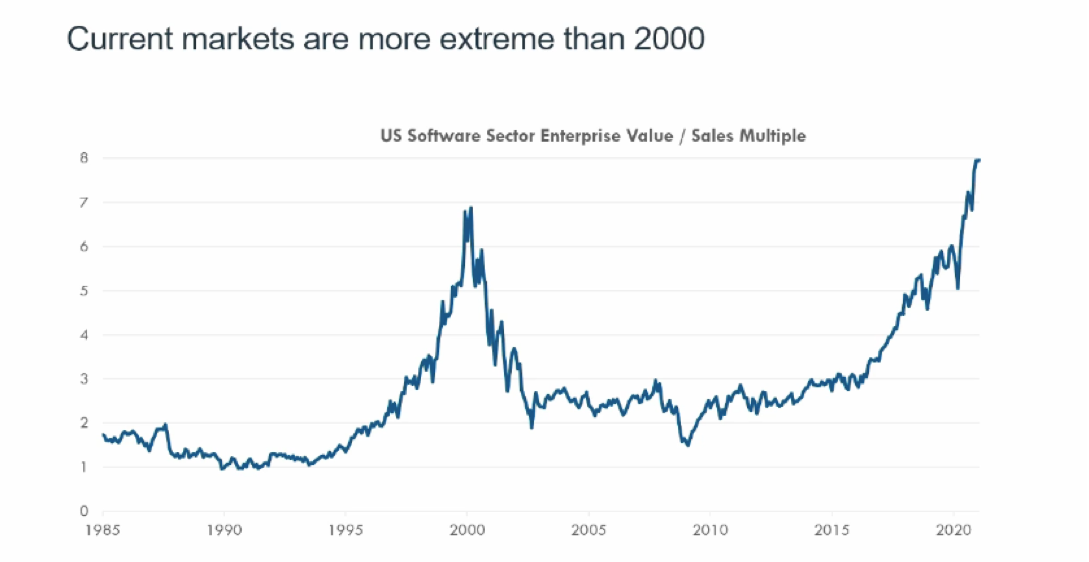

- But perhaps the most compelling piece of evidence is the valuations of these fast-growing companies. We’re not talking about the FANGS here (Facebook, Apple, Netflix, Google) but rather the companies trading on 20x, 30x and in some cases even 50x sales or more. Note: We talk about sales because for the majority there are no profits.

Companies such as Tesla (people say that Tesla made more in 2020 from its Bitcoin buy than the company itself) and locally, Afterpay by way of example. And here is the thing – most of these companies have done extraordinarily well to get to where they are. For the most part, we do not doubt the prospects of these high fliers. The issue is this – we simply have to make heroic assumptions about their business to make any sense of their stock prices. Some will make it, but with 100’s of companies and billions of market cap, it is safe to say some will not. When people say this not like the 2000 tech bubble, we agree, this appears to be a much larger bubble.

The question is, when does it end, and what does it mean for the more rational component of the market?

To answer this, we focus on interest rates. As part of the economic recovery, they will rise. Aside from the fact they can’t go any lower, the simple truth is they always do when activity strengthens, and they already are in the form of 10 year government bond yields. A natural outcome of a strengthening economy where liquidity is drawn into financing real businesses and investment.

The impact of this on equity markets is not so straight forward. On the one hand, economic growth is good for many companies, and it will be reflected in their profits. However, on the other hand, higher 10 year interest rates increase the cost of debt capital and therefore both theoretically and practically mean lower valuations for stocks (unless their profit growth outstrips the rising cost of debt), and this is most concerning for companies where valuations are the highest. Rising long-term interest rates are a real threat to the speculative end of the market, and as such, we predict a challenging year for investors in this sector. Indeed, it looks like this has already begun. The hot tech stocks were the best industry sector last year in terms of share price gains and the worst this year so far.

Beyond this, there are two other concerns.

The first is inflation. We already see some tightening across commodity markets and goods manufacturing particularly supply chain issues. Shortages and price movements bring with it early signs of inflationary pressures. As we saw earlier, there is some capacity in the Australian economy, but if governments continue to spend (as we strive for full employment), the question is how much more does this impact bond markets?

The other issue is the level of debt. Much discussed over the last decade as a result of the GFC but somewhat brushed aside as governments have spent to deal with the pandemic. At the end of this recovery, we will have significant levels of government debt. An issue that at some stage will need to be addressed. Will governments introduce policies and tax measures to deal with the problem, or will they continue to spend adding to the inflation risk?

Government and Central Banks have a fine line to walk and it will only take a slight divergence from that line to spook markets.

Here at FinSec, we select funds based on our philosophy that higher quality, more robust portfolios do not own companies that lack a sound track record. Our managers look past the valuations of speculative companies that don’t make any money and look for those that will be around in decades to come – profitable income streams, free cash flow, higher dividend yields and higher quality management. Actively managed portfolios will always lag slightly in mad booms (they may not get the benefit of a Tesla jumping 300%), but they will more than add value in any big sell-off, as they did in 2011, 2015, the GFC and 2020.

We look after our client’s life savings and treat their money as if it is the last dollars they have left (for many, it is). We seek to be trusted advisers and with this comes the responsibility to protect our client’s wealth to ensure it is still there in 10, 20 or even 30 years time.

Superannuation news

Your Future, Your Super Legislation (YFYS)

David Bell, Executive Director of The Conexus Institute, presented this week to the Senate Economics Committee on the proposed Your Future, Your Super legislation. Touting the institutes’ findings on the performance test, which they believe will drive unwelcome changes. A succinct summary of the report can be found here.

As David Bell points out, unfortunately, as it stands today, the YFYS performance test ignores asset allocation (which has a significant impact on performance) and only assesses implementation performance. It does this by mapping portfolio exposures to a limited set of public market indices. In effect, this renders the test ineffective in truly distinguishing between ‘good’ and ‘bad’ performers.

For super funds, the penalties for failing the performance test are severe. If present investment strategies are maintained, funds may find they have to frequently adjust their portfolios in reaction to short-term underperformance, which could incur sizable transaction costs. This could lead to a future state whereby super funds will seek a more stable investment strategy, which provides a high likelihood of passing the performance test and a low likelihood of frequently altering their portfolios. In short, these constraints could translate to less investment choice and super funds that simply strive to hug the average for average returns.

The reform package is undoubtedly well-intended. Therefore, it is critical that it achieves its intended purpose. The worry is, the commencement date of 1 July 2021 is only three months away, and the bill has not been drafted, never mind passed.

Early Access to Super Final Report

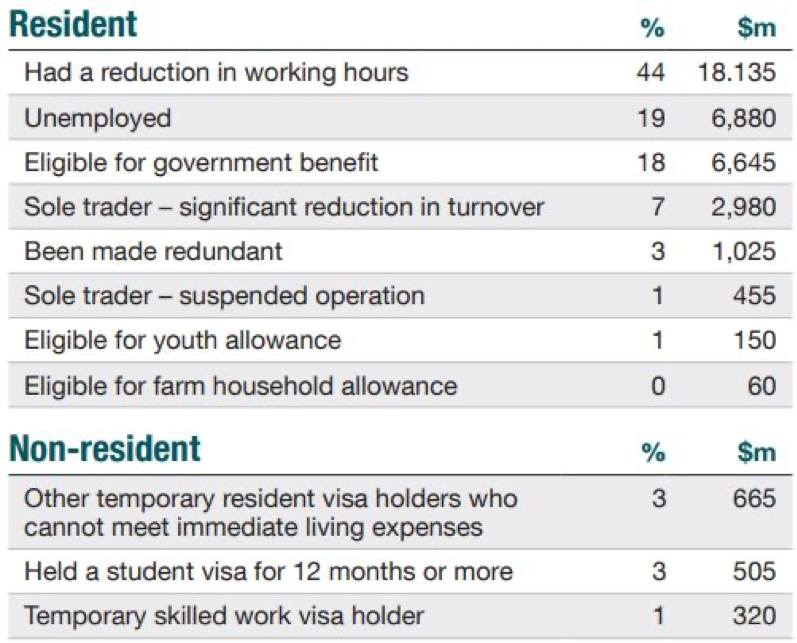

This week, the ATO issued a final report on the early access to super scheme, which permitted withdrawal of up to $20,000 per person. It showed that many people will drain their super if permitted with 4.8 million applications for $39 billion received. The ATO approved 4.6 million applications for 3 million people citing the following reasons:

Not surprisingly, the report demonstrated that SMSFs hold larger balances with members who do not want to withdraw early. Only 40,000 of the applications worth $395 million came from SMSFs. This is only about 1% of the total amount withdrawn, although SMSFs hold over 25% of super balances.

Short-term gain for long-term pain.

Whilst allowing access to super during the pandemic was crucial to many in our community (not everyone qualified for JobKeeper, mortgage/rent relief); unfortunately, many Australians have now wiped out their entire super balances. While the short-term impact is simply a reduction in their super by the amount they withdrew, the long-term impact on their retirement savings could be significant (particularly the younger they are). The flow-on to Australia’s social security system also bares thinking about – $39 billion compounded over a number of years is a ‘super’ shortfall.

Things that make you go mmm…

Taking some of the shine off the cryptocurrency is new revelations that China owns around 75 per cent of bitcoin mining. It’s also been revealed that the cost of mining this Bitcoin is set to consume as much energy as Italy by 2024. Mmm… will the world really want to be exposed to a transactional currency that China potentially controls? Will investors continue to support a product using so much energy before we can transition to a more renewable energy environment? We think not.

This new information adds more uncertainty to our already less than favourable view of Bitcoin (refer FinSec View). In reality, China’s grip on bitcoin mining and deteriorating relations between it and the West underlines the potential for the currency to be used to manipulate economies. We can’t help but feel that the Bitcoin story has much to play out.

Chart of the week

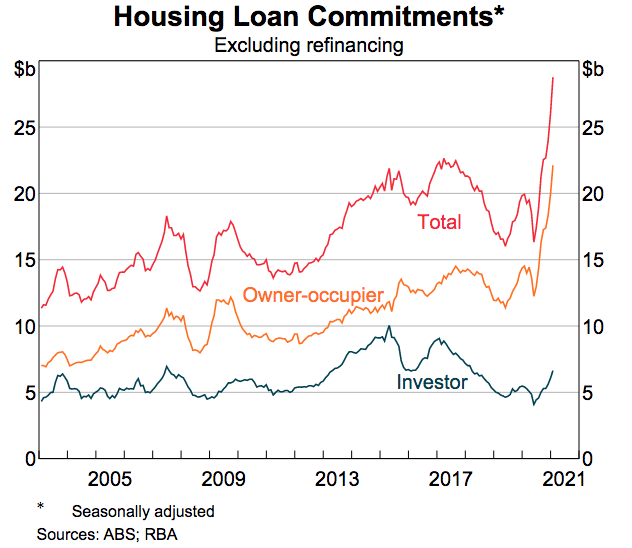

Our chart of the week is straight from the RBA’s chart pack released last week. It depicts housing loan commitments over the last decade.

New lending (upgraders and first home buyers) is through the roof, pun intended. Of significance is the fact that investors have been slow to join the party. The last two times that the central bank and regulators moved into the market to slow things down (2015 and 2017) it was to slow down investors.

The central bank knows that supporting the housing market is the the way to re-boot the economy, but they watch investors closely and as this graph shows investors are beginning to make their move. For this reason we expect to see some activity from the regulator in the next 12 months.

Federal Budget – What to expect

Delivered on the second Tuesday in May, the 2021 Federal Budget is less than 4 weeks away.

The fiscal position is expected to be a lot better than the government was predicting. This is namely off the back of the recovery and iron ore prices. Nonetheless, still pretty extraordinary debt numbers. Some of the big themes we’ll be watching for this year include:

- Will we see radical budget repair policies, such as a repair levy like we saw in 2014? Perhaps an extra tax for the mining sector or other sector that did well through COVID (pharmaceutical, digital)?

- Policies to address housing affordability – Initiatives aimed at boosting supply rather than demand.

- Business investment and productivity – Depreciation allowances are maxed out, and appetites to cut corporate tax will be low. Will we see something more subtle targeting certain sectors?

- Preserving education and tourism – The last Budget was framed around the assumption that foreign borders would be open in the second half of 2021 (not going to happen). What will the government do to preserve education and tourism infrastructure, both fundamental to Australia’s future and our ability to sell services to the Asian middle class?

- We’ve been promised a ‘female friendly’ Budget – We expect to see initiatives that enhance women’s ability to top up their super and perhaps further reforms to childcare.

- High on our agenda will be reforms to ensure more Australians can access affordable financial advice (we’re not holding our breath).

- Amid all of this, Frydenberg and the government have an eagle eye on the next Federal election, which must be held in the next 12 months. At the moment, with support for the government faltering and the Labor Party having an election-winning lead in the polls, Frydenberg will want to frame policy decisions in the budget and the overall economic management issue in favour of the Coalition.

The responsibility of building a strong budget framework is not a job many would covet. We’ll be tuning in on Budget night with anticipation and look forward to bringing you our synopsis from a FinSec perspective.

Stay safe and look after one another. Enjoy the weekend and as always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.