- Global share markets fell over the last week mainly on the back of hawkish central banks and ever rising bond yields. Australian shares also fell slightly with strength in utilities and energy stocks offset by weakness in retailers, IT and materials. Bond yields rose sharply, and oil, metal and iron ore prices fell. While the $A briefly made it above $US0.76 it ended the week little changed, despite a further rise in the $US.

- While shares have had a great rebound from their March lows they appear to be faltering again. Views remain that share markets will be higher on a 12-month horizon, but it’s still too early to be confident we have seen the bottom and volatility is likely to remain high. Key central banks are continuing to sound more hawkish, bond yields are continuing to rise, uncertainty remains high around the war in Ukraine even if the Russia is refocusing on the more limited objective of controlling the Donbas, political risk may re-emerge in Europe with the French election and the return of possible tax hikes in the US to fund a slimmed down Build Back Better program may add to uncertainty ahead of the US mid-terms. And the rebound in shares since early March has lacked the breadth often seen coming out of major market bottoms with defensive stocks leading the charge.

- The Fed has further ramped up its hawkishness. Just when it seems share markets were thinking the worst from the Fed was factored in, the minutes from the Fed’s last meeting and comments by Fed vice-chair Brainard have caused another reset. The Fed now looks likely to start quantitative tightening (ie reducing its bond holdings) from its May meeting at the rate of $US95bn a month with this being phased in over three months. This is far quicker than the $US50bn a month that took a year to reach back in 2017. What’s more there appears to be a greater preparedness to do 0.5% hikes. The US money market is now factoring in another 2.1% in rate hikes this year.

- The problem central banks face is that while the surge in inflation is mainly due to supply side constraints, which they can’t do much about, the longer inflation stays high the more it will be built into inflation expectations and becoming self-perpetuating. Hence the scramble to tighten is all about keeping inflation expectations down.

- The RBA now appears to be coming to the same view, with its April meeting showing a big hawkish pivot as it looks to be gearing up for a rate hike soon. Just as Fed Chair Powell quickly dumped his reference to being “patient” in assessing the inflation outlook earlier this year so too has the RBA. And it has dropped references to “uncertainties” about how sustained the pickup in inflation will be. Although it didn’t say so in its post meeting statement the RBA looks to be shifting to focus on what Governor Lowe described as doing “what is necessary to maintain low and stable inflation in Australia.” It’s now focussed on inflation data due 27th April and wages data due 18th May – both of which are likely to come in well above the RBA’s expectations. So, while a May rate hike in the midst of the election campaign can’t be ruled out if the March quarter inflation data really blows out, the timing of the next wages data does give it an excuse to wait till the June meeting. So, at this stage views remain that it will hike rates in June taking the cash rate from 0.1% to 0.25%, which has now become consensus. However, with inflation risks skewing to the upside there is now a strong chance that the first hike will be 0.4% (taking the cash rate to 0.5%) in order to have a decent impact and either way we now see the cash rate being progressively increased to 1% by year end with the risk that it will be increased to 1.25%. Market expectations for a hike to 2% by year end still look a bit too hawkish though.

- The RBA’s Financial Stability Review suggests the financial system overall is in good shape and should be able to cope with higher interest rates – banks are well capitalised, loan arrears are low and many households have built up buffers on their mortgages. The latter are estimated to be equivalent to a median 21 months of payments for variable rate borrowers which is up from 10 months prior to the pandemic. And as a result of excess payments, roughly 40% of variable rate borrowers would see no increase in monthly payments even with a 2% rise in rates. Against this, around 25% of variable rate borrowers would see their payments rise by more than 30%. And the RBA also notes that a large share of new housing loans have high debt to income ratios and that high levels of household debt have increased the sensitivity to higher interest rates which will make it difficult for some households. All of which means interest rates won’t need to go up as much as in the past to slow spending & control inflation.

- Later this year some of the pressure may start to ease on central banks. Global oil prices may have already seen their peak (Russia/Ukraine war dependent though), shipping freight rates have eased a bit and US used car prices have started to fall again – but of course there is a long way to go and we have seen a few signs of improvement in the last six months only to see another round of supply pressures.

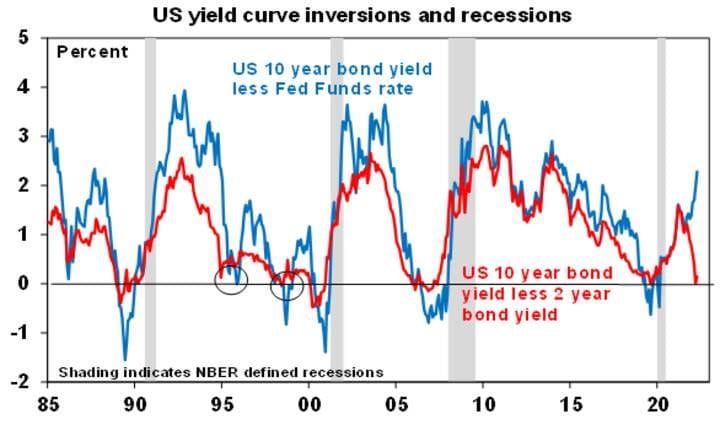

- More on inverting yield curves – rising US recession risk but it’s complicated. The recent flattening and brief inversion of the US yield curve as measured by the gap between 10-year bond yields and 2-year bond yields has led to more talk of recession in the US. This is clearly a rising risk. However, there are several points to note. First, the more traditional measure of the yield curve which looks at 10-year yields less the Fed Funds rate (or the 3-month yield) is actually steepening and this indicator has been seen as a more reliable guide to recessions. So far, it says there is no problem. Second, the 10-year/2-year comparison may be distorted because while the 2-year yield has been pushed up by expectations of an increasing Fed Funds rate the 10-year yield is being suppressed by the Fed’s massive holding of Government bonds. This may soon reverse with the Fed likely to start running down its bond holdings next month. Fourth, investors have been happy to have more bonds in their portfolios in recent times because bonds were seen as negatively correlated to shares which has in turn suppressed long term bond yields. But if bonds now sell off with shares due to a more dominant influence from inflation, then this bond demand may fade and long-term bond yields will rise. Fifth, inverted yield curves have sometimes given false signals. And finally, the gap from an inverted yield curve to recession has averaged around 18 months. So US recession is a risk but more of a risk for 2024 or late 2023.

Source: Bloomberg, AMP

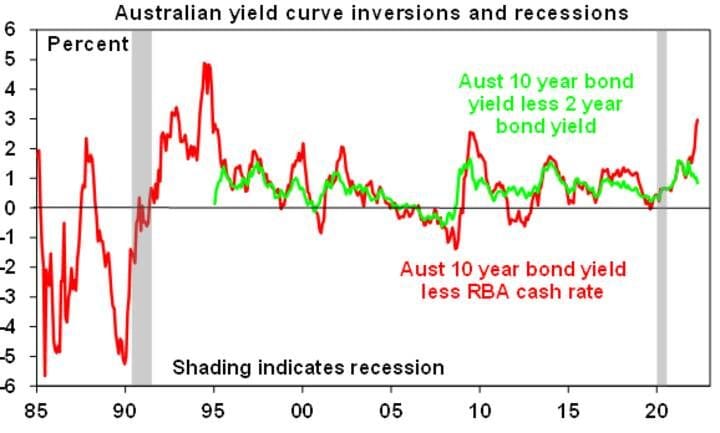

- In Australia, the yield curve has given numerous false recession signals – but it’s nowhere near signalling a recession, albeit the 10yr-2yr gap has been flattening.

Source: Bloomberg, AMP

- The French presidential election race is the latest thing to worry about. Polling has tightened in the last few weeks with Marine Le-Pen of the far-right National Rally (which has been softened from National Front) gaining on centrist President Emmanuel Macron. Macron still looks to be ahead but it has become a closer call. Recent polling shows Macron leading with around 26.5% in the first-round vote on 10th April where there are 12 candidates and Le Pen around 21.5%. An average of major polls then points to Macron beating Le Pen in the second-round run-off on 24th April by around 52% to 48%. However, the gap has been narrowing with Le Pen softening her far right image from five years ago. Euro-scepticism has declined in France over the last decade with around 73% of French in favour of the Euro so the election poses little risk of a Frexit (French exit from the Euro). A Macron victory would likely see him continue to take on the role of leading Europe (after Merkel’s departure) and a continuation of his economic reform program. By contrast a Le Pen win would come as a shock to investment markets and while it’s unlikely to lead to a Frexit, her policies would threaten European unity in terms of economic policy and against Russia and would be bad for the Euro and French shares.

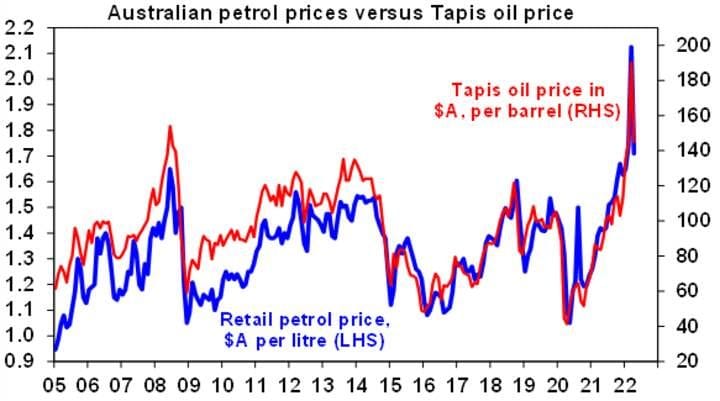

- Australian petrol prices have fallen sharply over the last three weeks reflecting lower oil prices, the higher Australian dollar and the 22.1 cents/litre fuel excise cut. Even ignoring the tax cut, petrol prices should be back to around or below February levels. So far, the fall can mostly be explained by the fall back in oil prices though. Whether it sticks depends largely on what happens to global oil prices.

- Expect an increasing focus on the Australian Federal election in May – but the substantive policy differences between the Government and the Opposition are minimal suggesting little impact on investment markets. Current polling has the ALP ahead by around 54%/46% but it was not a good guide to the 2019 election result. If the election were solely being determined by the state of the economy, then it would point to a victory by the Coalition but its as much about how people feel and right now confidence is subdued as a result of a range of factors including the rising cost of living and increasing warnings of higher interest rates. There is some evidence that Australian shares go through a period of range trading through election campaign periods reflecting political uncertainty. An ALP Government is likely to be more interventionist in the economy, focus more on public services including childcare and the aged and tighten decarbonisation commitments – but so far it’s not offering a significantly different policy approach. Unlike in the 2019 election though the ALP is not proposing a radical tax agenda this time around. Like the Government it is seeking to repair the budget through economic growth rather than austerity and its priority areas of energy, skills, the digital economy, childcare and manufacturing have a significant overlap with the Government. Neither side is proposing a significant reform agenda in key areas like tax, education, industrial relations and housing affordability. So it’s hard to see a big impact on markets.

|