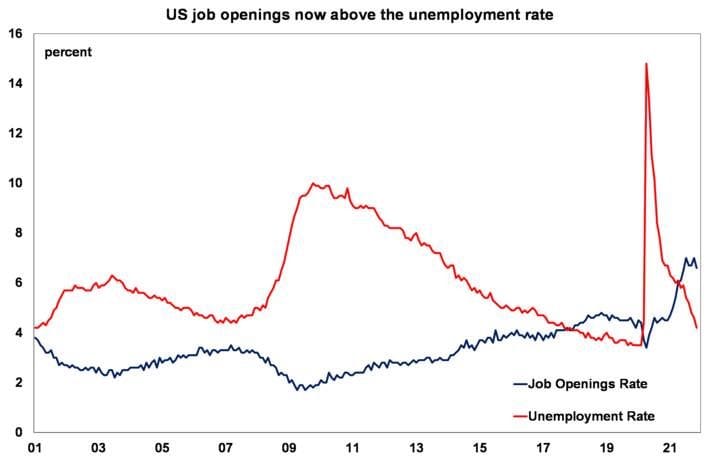

- The economic calendar was fairly quiet in the first week of the new year, but fears of rising US interest rates led to some sharemarket wobbles. US sharemarkets were down 1.5%, with large falls in tech, real estate, healthcare and communication sectors. Rising 10-year bond yields (up by 20 basis points since last week to 1.7%) were negative for tech stocks (with the tech-heavy NASDAQ down 3.6% over the week). Tech shares tend to underperform when long-dated bond yields rise. The ASX fell significantly on Thursday, taking its lead from the US, but managed a turnaround on Friday and was up by 0.4% over the week at the time of writing. European shares managed to squeeze out a gain of 0.6%, Japanese shares were down by 1.1% and Chinese shares fell by 2.5%. The $US rose and the $A was down to 0.71USD. Oil and natural gas prices rose while metals prices were mixed.

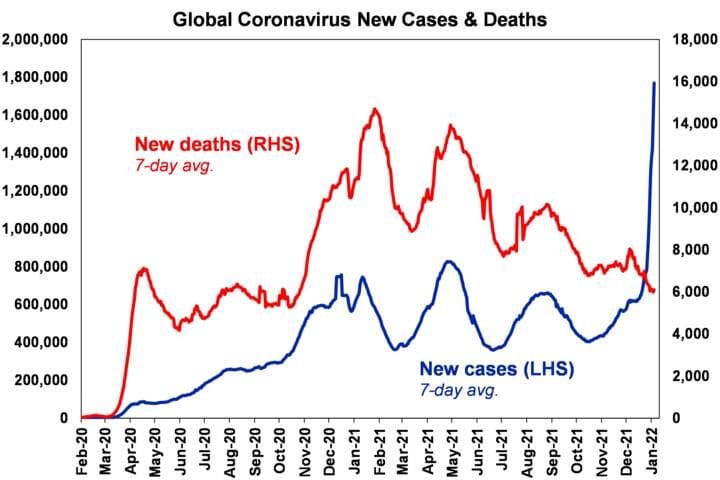

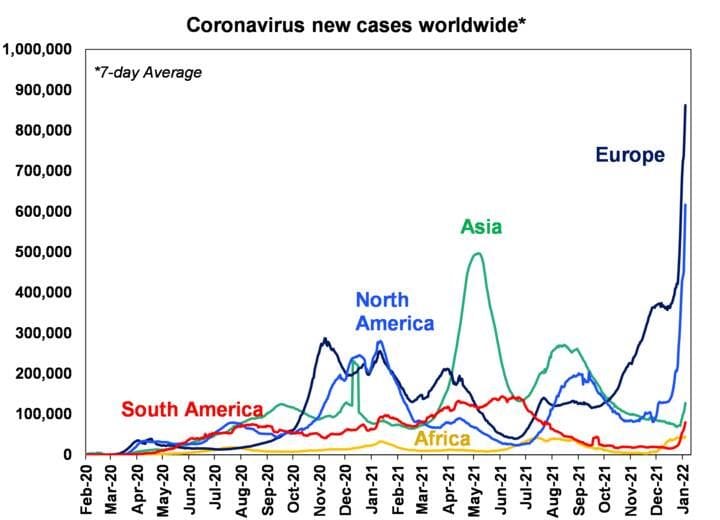

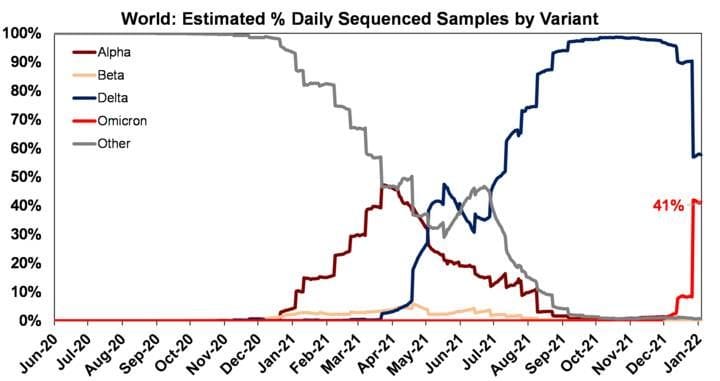

- Global coronavirus cases have skyrocketed over recent weeks across European countries, the US, Canada and Australia (see the charts below) with new cases more than double levels from the previous peak, with the more transmissible but less deadly Omicron variant making up the largest share of new Covid-19 cases around the world. Coronavirus continues to impact economic activity, despite less severe lockdowns, lower deaths and the availability of vaccines, so it is still important to keep an eye on cases and hospitalisations.

Source: ourworldindata.org, AMP Australia

Source: ourworldindata.org, AMP Australia

Source: ourworldindata.org, AMP Australia

- The good news is that Omicron does appear less deadly (which probably also has something to do with the population being protected by vaccines and prior exposure to the virus over the past two years) and while new deaths do tend to lag new cases by a few weeks (so are still likely to rise over coming weeks), they are well below deaths recorded earlier in 2021.

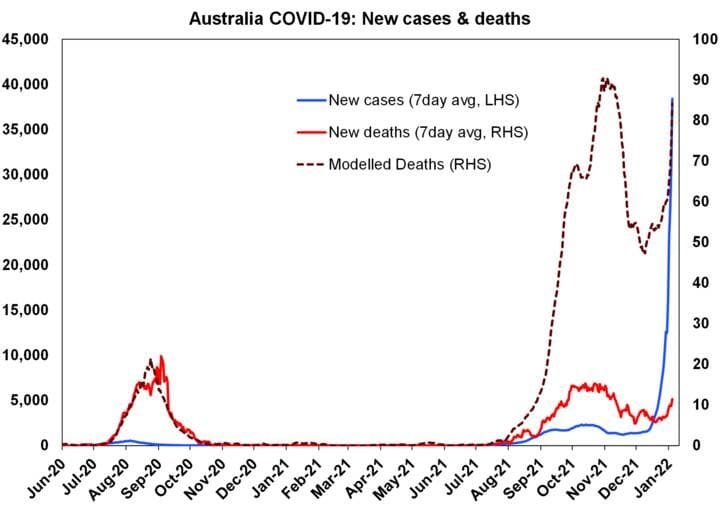

- Australian modelled deaths are running at around 13% of predicted deaths based on the Delta wave (see the chart below).

Source: ourworldindata.org, AMP Australia

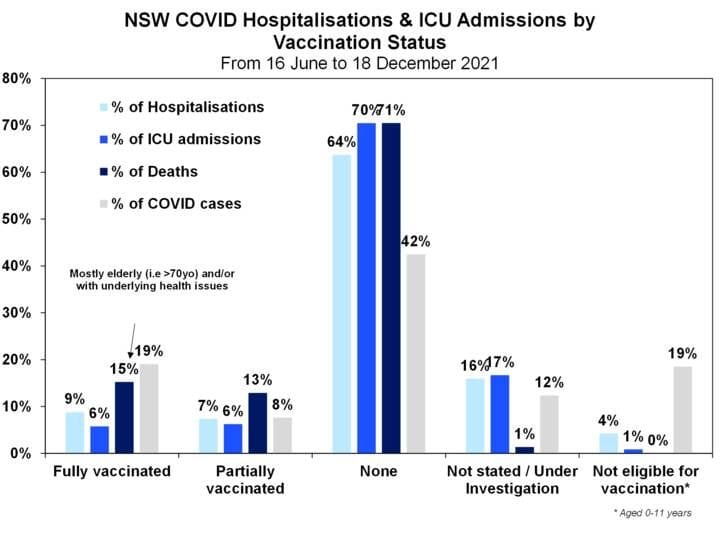

- And most of those needing hospitalisation remain the unvaccinated (see the chart below) which is more proof that vaccines work to prevent serious illness.

Source: NSW Health, AMP Australia

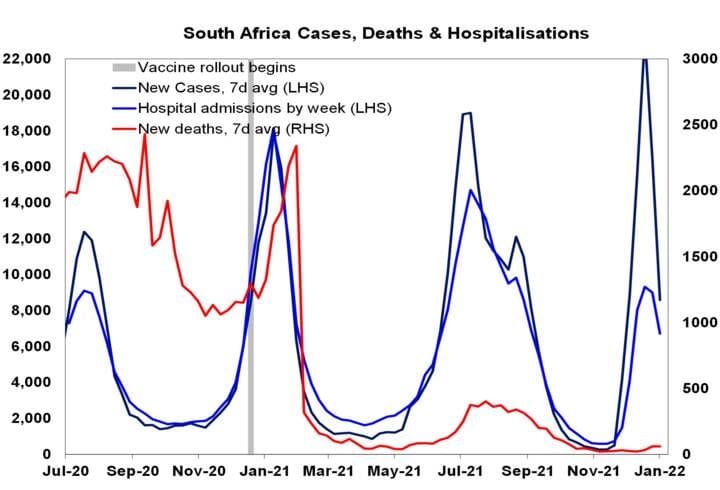

- Out of interest, in South Africa new Covid-19 cases spiked in mid-December but have since started to decline which has given some hope that Omicron will eventually see Covid-19 turn out to be a less severe disease. Although it’s probably also related to some restrictions imposed by the government in response to the outbreak of Omicron.

Source: ourworldindata.org, AMP Australia

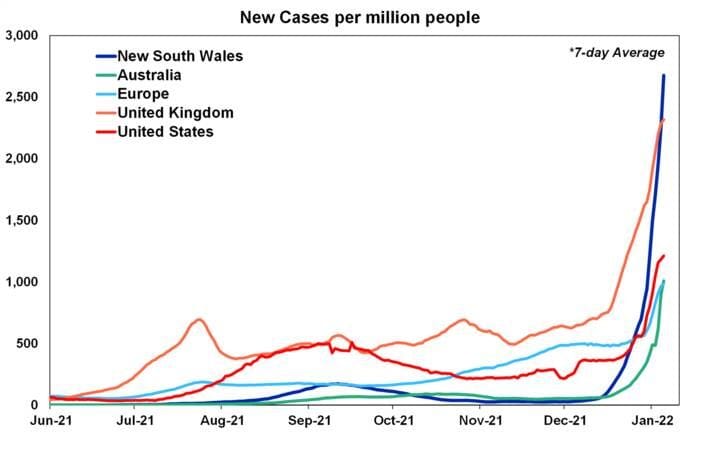

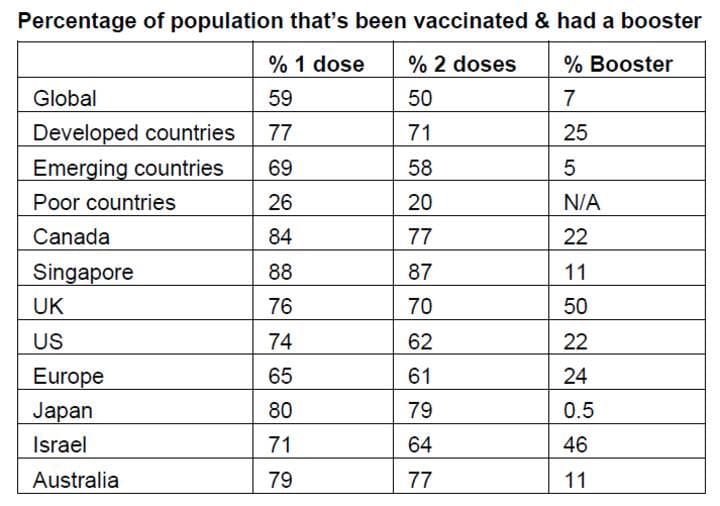

- Australia is in a bad position with the spread of coronavirus with NSW and Vic recording new daily record highs in cases. This boils down to the easing of virtually all restrictions in December at a time of a new, more transmissible variant, very early stages of the booster rollout (see the table below of booster rollout comparisons around the world, Australia has given 11% of its population a booster vs the UK at 50%) and the holiday season which means more travel and interactions. NSW cases per capita are currently higher than the US and UK on a 7-day average (see chart below). And of course the difficulty in getting a PCR test means that many cases are going uncounted with people relying on rapid antigen tests (if you are lucky enough to get one… hopefully this situation resolves itself in a few weeks once supply is higher).

Source: ourworldindata.org, AMP Australia

Source: ourworldindata.org, AMP Australia

- While we need to live with Covid-19 in our daily lives, the easing of restrictions in NSW and Vic could have been done in a safer and slower way, to allow the system to cope with higher cases while also supporting economic activity. And while lockdowns hit economic activity, a high case load does the same thing. People will choose to self-regulate mobility and live lockdown “light” and businesses will get disrupted by sick or isolating staff which is already becoming clear in the fall of the economic activity indicator. Previously was expecting March quarter GDP to increase by 1.6% but given the high case count it has been revised down to a smaller increase of around 0.6%. Of course this could mean that GDP growth will rebound again in the June quarter, if coronavirus cases decline.

- Now, it is likely that more restrictions will have to be imposed in NSW to slow down case growth and allow the hospital and testing system to cope with higher cases. While the state government assures us that hospital capacity is still manageable, the cancellation of elective surgeries tells a different story. Today’s media is reporting that some restrictions are going to be announced soon, like nightclub closures and stopping singing and dancing in pubs.

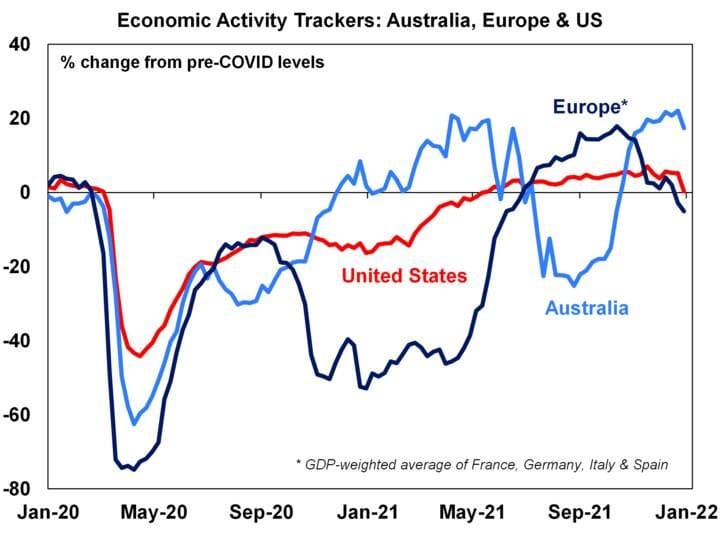

- Our economic activity trackers moved lower this week (see the chart below) across Europe, Australia and the US as coronavirus cases continued to rise. In Australia, consumer confidence weakened, restaurant bookings fell and mobility worsened. In the US, mobility fell a lot, hotel bookings were down, mortgage applications declined and job advertisements growth was also weaker. The fall in the Europe tracker was mainly because of lower restaurant bookings and retail traffic.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP Australia

|