Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 30th June 2017

Investment markets and key developments over the past week

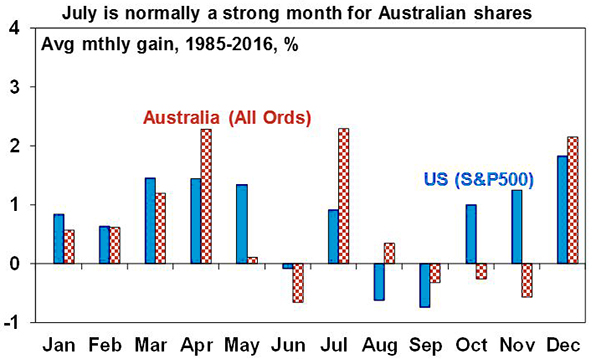

- Global share markets had a rough ride over the last week as somewhat more hawkish comments from central banks weighed and pushed bond yields higher. This was particularly the case in Europe with Eurozone shares down 2.6% for the week, against falls of just 0.6% in the US and 0.5% in Japan. Chinese shares actually rose 1.2%. Meanwhile, commodity prices rose solidly from oversold and under loved levels – particularly oil (up 7%) and iron ore (up 14%). Reflecting higher commodity prices and a weaker US dollar, the Australian dollar bounced back to around $US0.77 although it’s worth noting that it’s been stuck between $US0.72 and $US0.78 for more than a year now. Despite the weakness in US and European shares, Australian shares managed a 0.1% return over the last week helped by a rebound in commodity prices and inflows into superannuation funds ahead of limits affecting some members, which will apply from July. July is normally a strong month for Australian shares although the forward payment of superannuation flows into June could reduce payments in July this year.

Source: Bloomberg, AMP Capital

- Taper tantrum 2.0 – some more hawkish noises from central banks, but don’t get too excited. Central bankers from the US Federal Reserve, the European Central Bank, the Bank of England and the Bank of Canada all sounded a bit more hawkish over the last week, with the last three signalling an eventual end to ultra-easy monetary policy. However there are several points to note in relation to this:

- First, the shift in the tone of central bank commentary – notably at the European Central Bank, Bank of Canada and Bank of England – in large part just matches the improvement seen in growth and the receding risks of deflation so should be seen as good news. However with underlying inflationary pressures remaining weak, global monetary policy remains a long way from anything approaching being tight and this is likely to remain the case for some time.

- Second, Federal Reserve Chair Yellen is just reiterating her long stated comments that it is appropriate for it to gradually remove monetary accommodation providing the US economy continues to improve. However, while she does not appear to be too concerned about inflation running below target because the labour market is so tight, others have expressed concern about the inflation undershoot and so there is now a high chance that the Federal Reserve will skip a September rate hike and wait until December before moving again. There is nothing in what Yellen has said pointing to a faster tightening.

- Third, while several officials (Yellen, Fischer and Williams) referred to strength in the US share market/asset prices, it is noteworthy that Yellen referred to the ongoing debate about shares looking a bit expensive on absolute measures, (like price/earnings ratios) but less so on a relative basis (if one allows for low bond yields). What does seem clear though is that at the current point in time the Federal Reserve does not see the share market price level as a constraint on raising rates. If it has a sharp fall reflecting growth worries, then this would be different.

- Fourth, European Central Bank President Draghi is clearly (and rightly) becoming more upbeat with the threat of deflation receding and “political winds…becoming tailwinds” (presumably a reference to President Macron’s pro-reform and pro-Europe election victory in France in particular). And why wouldn’t he with Eurozone economic confidence at its highest in nearly a decade?

- As such he is right to warn that policy will need to adjust once inflation rises. But at this stage there is still little evidence of much of an increase in underlying inflation and political risk around Italy will likely slow Draghi from moving too quickly. Views remains that it will announce a 2018 taper to its quantitative easing program later this year, but that rate hikes are a while away. Moreover the Bank of Japan remains years away from any easy money exit.

- More broadly there has been concern for some time that global shares are vulnerable to a correction. As seen over the last week, worries about central bank tightening have provided a potential trigger. However, as we have seen with the US Federal Reserve since it first started the process of monetary tightening with taper talk four years ago, monetary tightening is likely to remain very gradual and conditional on further economic improvement. A share market correction is certainly possible – just like we saw with the 2013 taper tantrum – but we are a long way from the sort of tight monetary policy that could bring the bull market in shares to an end.

- The rally in bonds this year had arguably gone a bit too far – things weren’t that bad – and positioning had become excessively long and complacent leaving them vulnerable to a rebound in yield that we are now seeing. However, with inflationary pressures remaining weak and monetary tightening likely to remain gradual (and non-existent in many countries including Australia for some time) the uptrend in bond yields is likely to remain gradual too.

- Delay in the US Senate vote on healthcare reform by a week or two is unlikely to be fatal. The delay looks to be more about allowing time for Republican Senators to discuss changes to the bill. Recall that healthcare reform was also thought dead in the House earlier this year when a vote on it was cancelled – only to see it pass a month or so later. Since Republicans and President Trump agree on reforming Obamacare and tax reform (tax cuts) views remains that it will be passed clearing the way for the latter.

- Eight rate hikes over the next two years from the Reserve Bank of Australia? Highly unlikely. Former board member, John Edwards commented that if its forecasts – for growth to pick up above 3.0% and inflation to be around 2.5% by mid-2019 – come to fruition then it “will want the cash rate to be 3.5% at least by end 2019” coming on the back of more talk of monetary tightening globally over the last week have naturally sparked a bit of interest. However, it’s doubtful this will happen. First, even if its forecasts are correct it’s likely that the rise in household debt ratios means that the neutral rate of interest (appropriate for an environment of 3% growth and 2.5% inflation) has fallen to maybe 2.5-3.0%. A 2.0% rise in mortgage rates on top of the rate hikes for investors and interest only borrowers already announced would mean a 50% plus rise in interest servicing costs relative to household income from late last year and likely cause a significant slowing in consumer spending and risk a rapid decline in home prices in Sydney and Melbourne. And the central bank knows this (and so won’t be that extreme). Second, it only forecasts underlying inflation around 2.0%, i.e. the low end of its target range, out to the end of 2018, making it hard to justify much in the way of rate hikes over the next 18 months. Third, eight rate hikes would likely push the Australian dollar higher damaging our competitiveness and services exports like tourism and higher education when we still need to see strong growth from them. Finally, the risks to the Reserve Bank’s growth and inflation forecasts are likely on the downside. Views remains that rates are on hold ahead of a rate hike maybe in 2019.

Major global economic events and implications

- US data was mostly good over the last week. Durable goods orders and new home sales were softish, but consumer confidence saw an unexpected rise (to around its highest since the early 2000s), home prices continue to rise, inventory levels rose more than expected in May, unemployment claims remain ultra-low and March quarter gross domestic product growth was revised up slightly to 1.4% annualised, due to a stronger consumer. May data showed that consumer spending looks to be on track for a solid June quarter gain, but the rate of inflation as measured by the core personal consumption deflator dipped to just 1.4% year on year which will help keep US interest rate rises gradual.

- Meanwhile, major banks in the US were cleared by the Federal Reserve to pay out hefty dividends and undertake share buybacks following recent stress tests that indicated capital levels at banks are healthy. The post GFC US bank capital rebuild is now complete and the tide is turning against heavy handed regulation.

- In Europe, economic confidence rose to its highest in a decade driven by both consumer and business confidence pointing to stronger economic growth. Similarly, the German IFO business conditions index was stronger than expected reaching a post-reunification high. Meanwhile, core inflation edged up in June, but only to 1.1% year-on-year.

- Japanese data for May showed strong jobs vacancies to applicant’s data (aided by a falling population), strong growth in industrial production on an annual basis and less negative household spending, but core inflation is still stuck around zero. With core inflation well below the Bank of Japan’s 2% target, no change to the Bank of Japan’s ultra-easy money is in sight.

- China’s official business conditions purchasing managers’ index data was surprisingly improved in June, suggesting that the recent slowing in growth may have come to an end.

Australian economic events and implications

- Australian data was light on with only second order releases. Credit growth remains moderate with weak personal and business lending and some moderation in property investor lending as recent APRA measures took effect. Continued solid growth in jobs vacancies over the three months to May, according to Australian Bureau of Statistics data, adds up to confidence that employment growth will remain solid in the months ahead. Meanwhile, population growth picked up to 1.6% in 2016 from 1.4% in 2015 confirming that underlying demand for housing remains strong and helping underpin potential growth in the economy. About 60% of the increase was due to net immigration and Victoria remained the fastest growing state with a 2.4% population gain in 2016. Western Australia and the Northern Territories were the weakest.

What to watch over the next week?

- In the US the focus will be on the Institute for Supply Management manufacturing conditions index to be released Monday and jobs data to be released Friday. Expect the manufacturing conditions index to remain solid at around 55 and jobs data to show solid payroll growth of 175,000 and unemployment remaining very low at 4.3% but wages growth still subdued at around 2.6% year on year. All of these will be enough to keep the Federal Reserve on track for gradual rate hikes. In other data, expect the non-manufacturing conditions index (Thursday) to have remained solid at around 56 and the trade deficit (also Thursday) to improve slightly. The minutes from its last meeting (Wednesday) will also be reviewed for clues on the outlook for interest rates.

- Expect the Eurozone unemployment rate for May to be released Monday to show a fall to 9.2%.

- In Japan the Tankan business survey for the June quarter (Monday) is expected to show improved conditions.

- China’s Caixin manufacturing purchasing managers’ index will be released Monday.

- In Australia, the Reserve Bank is expected to leave interest rates on hold for the 11th month in a row. While there could be downside risks to its growth and inflation forecasts, it has recently indicated a preparedness to look through recent volatility in gross domestic product growth data, remains optimistic that growth will pick up to around 3% and likely lacks confidence that the Sydney and Melbourne property markets have cooled enough just yet. While at some point the Reserve Bank may talk about exiting easy money – causing a bit of premature excitement in the process, the case remains that it will leave interest rates on hold for the next year at least, but for the next year there remains more risk of a cut than a hike.

- On the data front in Australia, expect CoreLogic data for June to show a bounce in home prices (Monday) after seasonal weakness seen in May but to confirm softer conditions overall and building approvals for May (also Monday) to show a decline, retail sales to rise 0.2% (Tuesday) and the May trade surplus (Thursday) to bounce back as coal exports recover. The AIG’s business conditions purchasing managers’ index data and ANZ job advertisements will also be released.

Outlook for markets

- Shares are still vulnerable to a short term setback as we go through a weaker seasonal period for shares with risks around the US Federal Reserve and other central bank exit talk; President Trump, North Korea, Chinese growth and the Australian economy all providing potential triggers. However, valuations remain ok – particularly outside of the US, global monetary conditions remain easy and profits are improving upon stronger global growth, so it is likely to see the broad 6-12 month trend in shares remaining upwards.

- Low yields point to low returns from sovereign bonds. Expect a resumption of the gradual uptrend in yields.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the ongoing search for yield, but this will wane eventually as bond yields trend higher.

- Australian residential property price gains are expected to slow, as the heat comes out of the Sydney and Melbourne markets.

- Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.5%.

- It is likely that the downtrend in the Australian dollar from 2011 will resume this year. The rebound in the Australian dollar from the low early last year of near $0.68 has lacked upside momentum, the interest rate differential in favour of Australia is continuing to narrow and will likely reach zero early next year (as the US hikes rates and Australia holds or cuts). Expect a fall below $US0.70 by year-end 2017.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer