Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 29th January 2021

Investment markets and key developments over the past week

- Global share markets fell over the past week hit by a combination of concerns around coronavirus vaccine efficacy & roll out and delays to extra US stimulus as US retail day traders added to volatility. For the week US shares fell 3.3%, Eurozone shares lost 3.1%, Japanese shares fell 3.4% and Chinese shares lost 3.9%. Australian shares fell reflecting the weak global lead and a fall in iron ore prices with resources, IT, financial and industrial shares seeing the biggest falls. Bond yields fell in the US but were flat in Germany & rose in Australia & Japan. Reflecting the risk off tone commodity prices and the US$ rose, and this weighed on the A$.

- The US and other share markets including Australia’s had a huge rally from early November supported by positive news regarding vaccines, more fiscal stimulus and monetary easing. This left them stretched and vulnerable to a correction which we may now be starting to see unfold as investors wait for hard evidence that the vaccines are working and that more US stimulus will actually be passed by Congress. It’s quite common for US shares to rally after the President is elected in January and then see a correction in February as investors wait for the new Administration to deliver. Global and Australian shares will also be impacted by any broader correction out of the US through February and it wouldn’t be surprising to see a 10% or so top to bottom decline. That said, this could be viewed as just a correction in a rising trend as the combination of stimulus and vaccines drive economic and earnings recovery and monetary policy remains easy. While investor sentiment is stretched, it’s too early to expect a cyclical bull market top with earnings still being revised up, inflation low and central banks remaining dovish.

- The frenzy of US retail day traders pushing up stocks that have been shorted by high profile hedge funds causing their prices to surge is creating a lot of noise and messing up the shorting strategies of some hedge funds, but it’s unlikely to have a lasting fundamental impact. It’s certainly interesting with elements of the little guys and the young versus the big guys and the old. But every so often something like this comes along – eg. various flash crashes, high frequency trading, day traders in dot com stocks, etc – that creates a lot of chatter and volatility. Ultimately if the hedge funds were fundamentally right then the stocks will go down and the day traders will get very badly burned which will serve to damp down such activity in the future. Of course, if it’s all just a bit of manipulation by the hedge funds then the day traders who got in early might have picked up bargains although it may not be so good for those who got in latter. Either way it’s really just a bit of short-term noise and will likely be largely forgotten about in a few months.

- Developments on the policy front in the US are not particularly surprising. First, it’s clear that Biden’s $1.9bn stimulus plan will take time to pass through Congress and will get cut back to say $1-$1.5bn to get enough Republicans and moderate Democrats on side, either as a regular bill (which needs support from 10 Republicans) or as part of the budget reconciliation process or a combination of the two. Some minor delay and a cutback to $1-$1.5 trillion are not major concerns given its hot on the heels of the $900bn stimulus, the ambit claim of $1.9 trillion risks overcooking the economy and even another $1 trillion at 4.5% of GDP is a lot. But the argy bargy around this may keep investors on edge until its finally passed.

- Second, the Fed left monetary policy on hold as expected, sticking to its commitment not to raise rates until inflation is at target and set to exceed it for a period and full employment has been reached with Powell reiterating that it’s too early to consider tapering quantitative easing. Powell also indicated that any pick-up in inflation in the months ahead is likely to be transitory, which means the Fed will look through it.

- The past week has seen a further decline in new coronavirus cases – particularly in the US, Europe, the UK, Japan and Canada. This largely reflects the tighter lockdowns and other restrictions seen since late last year rather than vaccines where deployment is still limited in most countries.

Source: ourworldindata.org, AMP Capital

- Investors are concerned about vaccine roll out and efficacy – but more vaccines are coming, and efficacy will need to be assessed against severe infections and deaths as well as new cases. The past week has seen Novavax report that trial results showed its vaccine is 89% effective in the UK and 60% in South Africa. Johnson and Johnson reported 72% effectiveness for its vaccine in the US, 57% in South Africa and 66% in Latin America and that it prevents 66% of moderate to severe cases, 85% of severe infections and 100% of hospitalisations and deaths. The obviously good news from this is that two new vaccines will now add to those from Pfizer, Moderna and AstraZeneca in fighting coronavirus and as production is ramped up this will overcome supply delays in the months ahead. The bigger concern is about efficacy with investors now fretting about the weaker trial results in South Africa adding to concerns about the impact of the new coronavirus mutations. However, vaccines don’t work just in terms of preventing infection but also in terms of preventing severe infection and death and the results from J&J are very positive on this front. This may mean that we have to live with coronavirus sticking around for a while, but this will not be a problem if severe cases, hospitalisation and deaths collapse thanks to the vaccines. This would still allow a gradual reopening globally once sufficient vaccines have been deployed. Of course, it means we will need to monitor the trend in new deaths maybe more importantly than new cases.

- Meanwhile, the past week has seen a further lift in vaccinations in several countries with around 35% of Israelis having had at least one shot, more than 10% of those in the UK and more than 6% in the US.

Source: ourworldindata.org, AMP Capital

- Out of interest Israel is seeing a declining trend in new cases with data showing a decline in new cases and hospitalisations amongst those vaccinated about 13 or 14 days after the first shot.

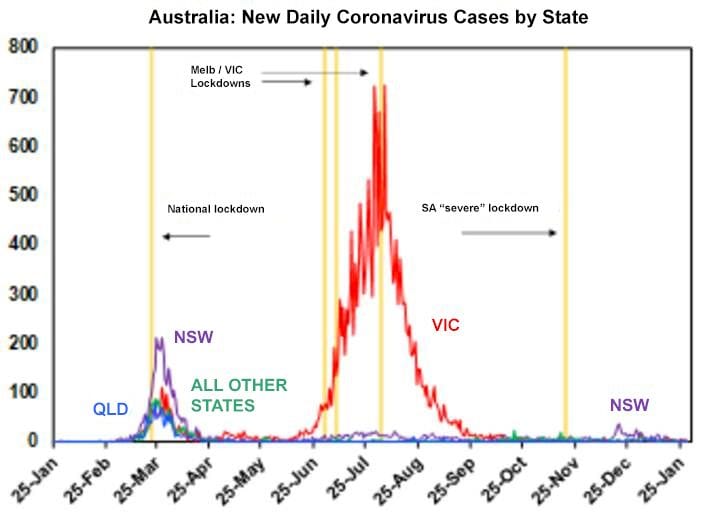

- In Australia, the number of new coronavirus cases remains very low and lately confined to returned travellers.

Source: covid19data.com.au, AMP Capital

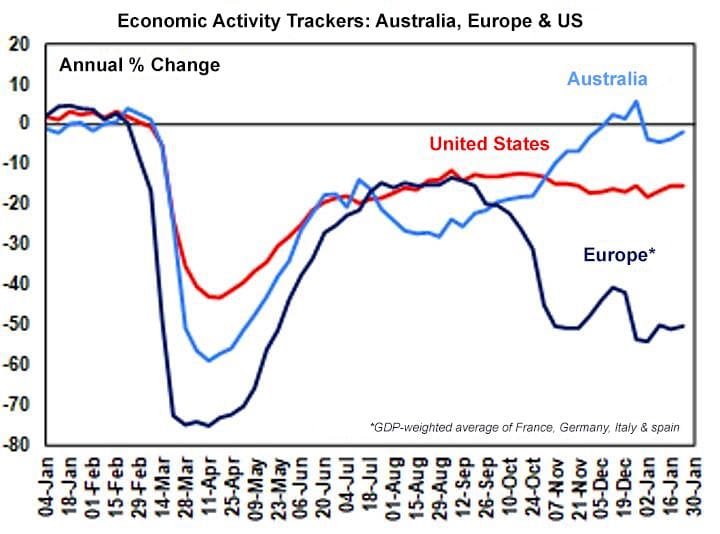

- Consistent with coronavirus coming back under control in Australia and restrictions being eased the weekly Economic Activity Tracker for Australia moved higher over the last week to be now back to around flat on a year ago. By contrast the US Economic Activity Tracker moved sideways and remains soft and down from its September high. And the European Economic Activity Tracker rose slightly over the last week but remains very soft.

Source: AMP Capital

- The IMF revised up its global growth forecasts. This is probably old news and private forecasters were already there. But after years of growth around 3%, the global economy is estimated by the IMF to have contracted -3.5% last year, which is bad but at least not as bad as the -5.2% contraction it was forecasting in June. It revised up its 2021 growth forecast to 5.5% (mainly due to the US) and is forecasting +4.2% in 2022. These forecasts are similar to others and also assume that thanks to vaccines and better containment coronavirus will reach low levels everywhere by end 2022.

Source: IMF, AMP Capital

Major global economic events and implications

- US GDP growth slowed as expected in the December quarter to just 1% quarter on quarter as the third wave of coronavirus cases took a toll, after the huge 7.5% reopening and stimulus driven rise seen in the September quarter. GDP is still down -2.5% from its pre coronavirus level but the latest $900bn stimulus will see growth supported this quarter. Other data releases were mostly ok with continuing strong capital goods orders, a slight rise in consumer confidence (albeit it’s still weak), a very strong Chicago PMI and continuing strength in mortgage applications, home sales and home prices but mixed jobless claims. Personal spending was soft in December, but income was stronger than expected and stimulus payments and a 13.7% saving rate will help spending ahead. Core private final consumption deflator inflation rose to 1.5% year on year but remains well below target.

- The US December earnings reporting season has now seen 37% of S&P 500 companies report, with results remaining strong. 82% of companies have so far surprised on the upside (compared to a norm of 75%) by an average 19% and 74% have beaten on revenue. As a result, consensus earnings expectations have been revised up to -1.4% yoy from -9% two weeks ago and are likely to end up back at pre-Covid levels.

Source: Markit, AMP Capital

- Eurozone economic sentiment was soft in January but is well up from its April low despite the recent lockdowns.

- Japan’s jobs market was flat in December with unemployment flat at 2.9% and no change in the ratio of job openings to applicants but industrial production fell more than expected.

Australian economic events and implications

- Australian economic data was mostly positive over the last week. While the NAB survey showed a fall in business confidence (partly reflecting the coronavirus clusters in late December), business conditions rose to their highest since mid-2018, the ANZ/Roy Morgan weekly measure of consumer confidence rose further above pre coronavirus levels, the terms of trade and hence national income look to have lifted sharply in the December quarter reflecting strong export prices and falling import prices and credit growth accelerated a bit in December driven by owner occupiers and business loans.

Source: RBA, AMP Capital

- December quarter consumer price inflation also came in stronger than expected driven mainly by higher tobacco tax, the impact of the removal of free childcare and free before and after school care and higher domestic travel costs. Underlying inflation remained weak at 0.4% quarter on quarter or 1.2% year on year, albeit this is a little bit above RBA expectations. Expect a bounce in Australian CPI inflation to ~3.5%yoy in the June quarter as last June quarter’s -1.9% plunge (due to free childcare, pre/post school care, the petrol price plunge, etc) drops out. Headline inflation will likely then fall back to low underlying inflation levels so the RBA (like the Fed) will largely look through it until underlying inflation picks up too. Meanwhile producer price inflation remained softish in the December quarter at 0.5%qoq/-0.1%yoy.

Source: ABS, AMP Capital

What to watch over the next week?

- In the US, the focus will likely be on January jobs data due Friday which is expected to show payrolls up 50,000 after last December’s surprise -140,000 fall, and unemployment unchanged at 6.7%. Meanwhile the January manufacturing ISM (Monday) is expected to remain strong at around 60 and the services ISM (Wednesday) is also likely to remain strong at around 57, but the risk is on the downside.

- The flow of US December quarter earnings reports will also ramp up. Strong business conditions readings and results so far point to earnings being roughly flat or slightly up on a year ago.

- Eurozone unemployment for December is expected to rise to 8.4%, December quarter GDP (Tuesday) is expected to show a -1.7% quarterly contraction after the 12.5%qoq September quarter rebound as a result of the return to lockdowns and core inflation (Wednesday) is expected to have remained around 0.2%yoy in January.

- The Bank of England meets Thursday and will be watched to see if it eases monetary policy further given the hit to the economy from its latest lockdown.

- China’s Caixin business conditions PMIs to be released on Monday and Wednesday are likely to have remained strong.

- In Australia, the RBA is expected to make no changes to monetary policy at its board meeting on Tuesday, but the focus will be on the post meeting statement, Governor Lowe’s speech on “The Year Ahead” on Wednesday and the Statement of Monetary Policy on Friday to see whether the RBA becomes hawkish following the recent run of strong economic activity data and higher than expected inflation in December. Expect Governor Lowe to acknowledge the good news but stay the course with a dovish bias. While the jobs market has improved faster than expected we are still a long way from full employment, jobs growth is likely to slow a bit in the months ahead with some jobs (eg, travel related) taking longer to return and some (eg, in parts of retail) likely to never return again, the end of JobKeeper in late March will create a bit of apprehension, coronavirus still has the potential to create upsets in the short term with uncertainty remaining about how effective vaccines will be, the strong A$ is maintaining pressure on the RBA to extend QE and a shift to hawkishness now would be inconsistent with the RBA’s commitment to focus on the achievement of actual inflation sustainably at target. However, Governor Lowe may turn down the RBA’s dovish bias a bit and drop the reference to expecting to not raise the cash rate for at least three years. Its also likely that following the end of the six months $100bn bond buying program at the end of April the RBA will continue it but at a reduced rate.

- On the data front in Australia expect to see a 0.6% rise in CoreLogic average dwelling prices for January and continued strength in housing finance (Monday), a -1% fall in building approvals (Wednesday), a rise in the trade surplus (Thursday) to $9bn, a -4.2% decline in December retail sales (Friday) as already reported in preliminary data with December quarter real retail sales up 1.8%.

- The December half earnings reporting season will likely show a strong rebound on the back of the economic recovery. Reports will start to flow in the week ahead but with only a handful of stocks reporting including GUD, Amcor, James Hardie, NewsCorp and REA. Earnings are expected to rebound in 2020-21 by 24% after the pandemic driven -24% plunge last financial year. In terms of sectors, earnings for resources are expected to rise by 43%, banks by 31% and IT stocks by 114%. Healthcare, media and gaming stocks are likely to see around 17% earnings growth and retailers are likely to surprise on the upside.

Outlook for investment markets

- Shares remain at risk of a short-term correction after having run up so hard recently and 2021 is likely to see a few rough patches along the way (much like we saw in 2010 after the recovery from the GFC). But looking through the inevitable short-term noise, the combination of improving global growth helped by more stimulus, vaccines and low interest rates augurs well for growth assets generally in 2021.

- We are likely to see a continuing shift in performance away from investments that benefitted from the pandemic and lockdowns – like US shares, technology and health care stocks and bonds – to investments that will benefit from recovery – like resources, industrials, tourism stocks and financials.

- Global shares are expected to return around 8% but expect a rotation away from growth heavy US shares to more cyclical markets in Europe, Japan and emerging countries.

- Australian shares are also likely to be relative outperformers helped by better virus control, enabling a stronger recovery in the near term, stronger stimulus, sectors like resources, industrials and financials benefitting from the rebound in growth and as investors continue to drive a search for yield benefitting the share market as dividends are increased resulting in a 4.4% grossed up dividend yield. Expect the ASX 200 to end 2021 at a record high of around 7200.

- Ultra-low yields and a capital loss from a 0.5-0.75% or so rise in yields are likely to result in negative returns from bonds.

- Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to space demand and hence rents from the virus will continue to weigh on near term returns.

- Australian home prices are likely to rise another 5% or so this year being boosted by record low mortgage rates, government home buyer incentives, income support measures and bank payment holidays but the stop to immigration and weak rental markets will likely weigh on inner city areas and units in Melbourne and Sydney. Outer suburbs, houses, smaller cities and regional areas will see relatively stronger gains in 2021.

- Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

- Although the A$ is vulnerable to bouts of uncertainty about coronavirus and China tensions and RBA bond buying will keep it lower than otherwise, a rising trend is still likely to around US$0.80 over the next 12 months helped by rising commodity prices and a cyclical decline in the US dollar.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer