Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 12th November 2021

Investment markets and key developments over the past week

- Share markets were hit again over the past week as more high inflation readings added to concerns about monetary tightening. This left US and European shares down for the week and Japanese shares little changed. Chinese shares bucked the trend and rose. While falls in US shares weighed on the Australian share market mid-week a strong rise on Friday left it little changed for the week with strong gains in materials offsetting falls in health, IT and property stocks. Bond yields rose on the back of inflation concerns. The iron ore price rebounded late in the week after hitting new lows, metal prices rose and the oil price rose slightly. The $A fell as the $US rose.

- Another round of high inflation readings ramping up the pressure on central banks. While the various central banks (notably the RBA with a dovish removal of its 0.1% bond yield target, the Fed with a dovish taper and the BoE leaving rates on hold) pushed back against market rate hike expectations a week or so ago, this has now been undone again by another run of high inflation readings with a 30 year high in US CPI inflation as price increases broadened beyond reopening sectors, a further sharp rise in producer price inflation in the US, China and Japan and strong price readings in US business surveys.

Source: Bloomberg, AMP Capital

- Supply bottlenecks as a result of the pandemic disrupting production and goods transport and boosting spending on goods relative to services remain the key driver. Views remain that inflationary pressures should ease through next year as workers return, production catches up and spending rotates back to services. And there are some signs of some easing in bottleneck pressures: coal and gas prices are of their highs; Russia appears to be preparing to boost gas flows to Europe (although Belarus President Lukashenko’s threat to shut down a Russian gas pipeline to Europe if Poland closes its border over a migrant despite could disrupt this); the US oil rig count is rising; semi-conductor production is up and chip prices are falling, and container freight rates are falling along with the Baltic Dry index. However, it could take 6-12 months and in the meantime the risk that inflation starts to feed on itself via higher inflationary expectations and wage rises will continue to rise which will increase the pressure on central banks.

- The base case remains that the Fed won’t hike till second half next year, but the risk is growing that it may come earlier. Europe and Japan with much weaker inflationary expectations will continue to lag. While higher global inflation will feed through to Australia the lower starting point for inflation here means that the RBA can also afford to lag – however expect stronger growth, wages and inflation than the RBA is allowing for and continue to see the first rate hike coming late next year. That said money market expectations for 3 or 4 RBA rate hikes over the next 12 months still look way too hawkish particularly compared to expectations for the US where only two hikes are factored in. Meanwhile, higher bond yields mean ongoing pressure on Australian fixed mortgage rates which will act as a dampener on housing demand and hence house price growth which will be seen to be slowing to 5% through next year followed by potential price declines in 2023.

- Shares at risk of another mini correction. A solid mostly US earnings driven rise in US and global shares from their early October lows has left them overbought again and vulnerable to another mini correction on inflation and interest rate concerns. While Australian shares have not rallied as much they could be pulled down by a correction in the direction-setting US share market. However, any pullback may be brief as the period into year-end is normally seasonally strong for shares. From a broader perspective though the trend in shares is likely to remain up as economic recovery continues but inflation and interest rate concerns will likely result in rougher and more constrained gains than what we’ve seen since March last year.

- US infrastructure bill passed, Build Back Better reconciliation bill looking likely too but it’s not a big stimulus – so Joe Manchin can relax. There are a few things to note about all this. First, the new spending in the bi-partisan infrastructure bill is $US550bn and will mean a big increase in US infrastructure spending which will be good for productivity. Second, the Build Back Better plan currently sits at $US1.75trn but could still be altered in the House (depending on how the Congressional Budget Office costs it) and by moderates like Joe Machin in the Senate, but its getting closer. Third, both bills are largely funded and are spread over many years and so will only provide a very modest net stimulus to the US economy – serving to only slightly reduce fiscal drag in the next year or two (much of which has already occurred due to the ending of covid programs). Fourth, agreement on the reconciliation bill should help clear the way to raise the debt ceiling in December.

Coronavirus update

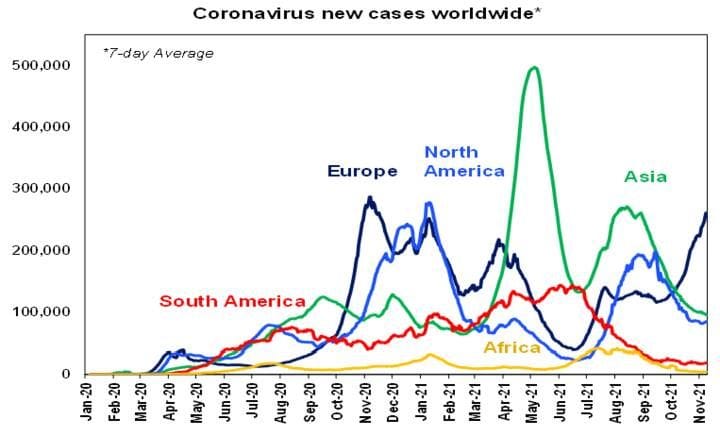

- Most global regions are seeing new cases flat to down but the US appears to have bottomed (with some states seeing a concerning rise again) and Europe is seeing a sharp rise. While new cases in Spain, Italy and France remain low various countries in Europe are seeing a sharp rise including Germany, Austria, the Netherlands, Denmark, Ireland and Finland reflecting a combination of the almost complete removal of restrictions, cold weather, stalling vaccination rates at below 70% of the whole population, fading efficacy against new infection and a slow start to boosters. To take pressure off hospitals some countries are reinstating some restrictions (vaccine mandates, masks, etc) much like Singapore (which has started to see new cases decline again) did.

Source: ourworldindata.org, AMP Capital

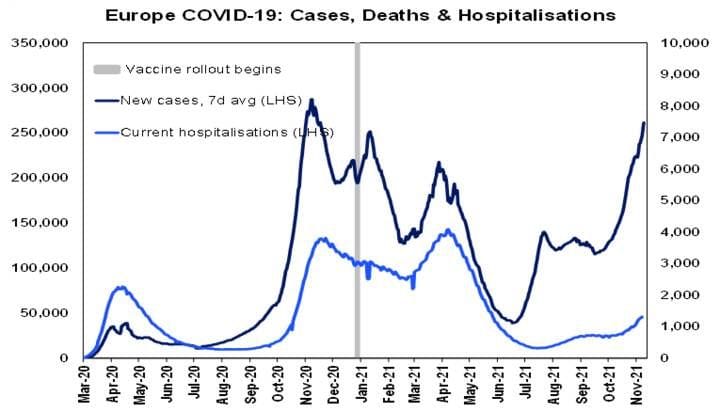

- The UK and US are at risk for similar reasons. There is little political support for a return to hard lockdowns, but this can’t be ruled out if hospitals are overwhelmed. The key to avoiding problems appears to be to get vaccination rates to very high levels (which is still an issue in the US), only remove distancing restrictions gradually and quickly roll out boosters to those whose last shot was 5 months or so ago.

- Key to watch remains whether vaccines stay successful in keeping hospitalisations manageable and deaths down. So far so good in Europe with new deaths and hospitalisations remaining subdued relative to new cases compared to past waves. In the UK deaths are running at less than 20% of the level suggested by previous waves. Of course if too many get coronavirus at once it could still overwhelm hospital systems (regardless of the protection offered against serious illness by vaccines) – hence the need for some restrictions to slow it down.

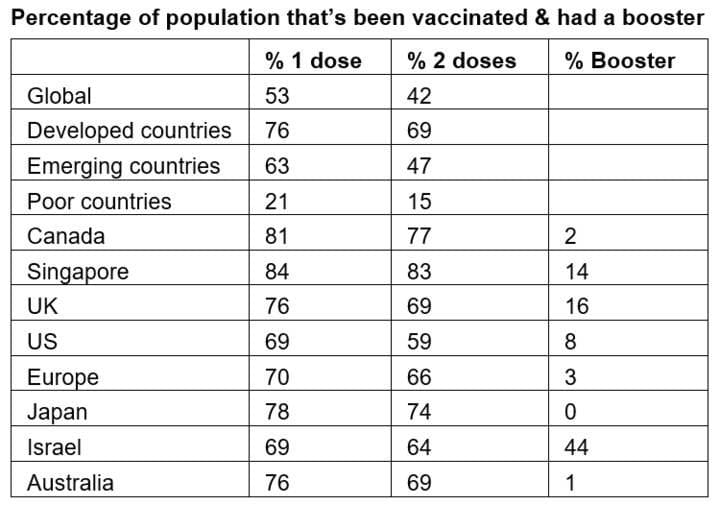

- 53% of people globally have now had one dose of vaccine and 42% have had two doses. Key risks remain that poor countries are lowly vaccinated which increases the risk of mutations and that some advanced countries (notably the US and Europe) have seen vaccination programs stall at levels well below that required against Delta.

Source: ourworldindata.org, AMP Capital

- Australia is now at 90% of adults with a first vaccine dose and has a greater proportion of the whole population fully vaccinated than Europe and the US. Allowing for current trends and the average gap between 1st and 2nd doses the following table shows approximately when key vaccine targets will be met. The ACT (with 96% of adults fully vaccinated), NSW, Victoria and Tasmania have led the charge, but other states are now starting to reach the 70% of adults double vax target. On current trends Australia will average 90% of the adult population fully vaccinated by early December, although the slowing pace of first doses has pushed out the attainment of 80% of the whole population double vaccinated into early January. This could be sped up again though by new coronavirus scares in the laggard states (as being seen in Queensland) along with the likely approval of vaccines for 6 to 11 year olds (which appears closer for the Moderna vaccine).

Source: covid19data.com.au, AMP Capital

- The faster than expected uptake of vaccines is seeing a faster reopening including moves towards reopening some state borders and to allow Australians to travel overseas.

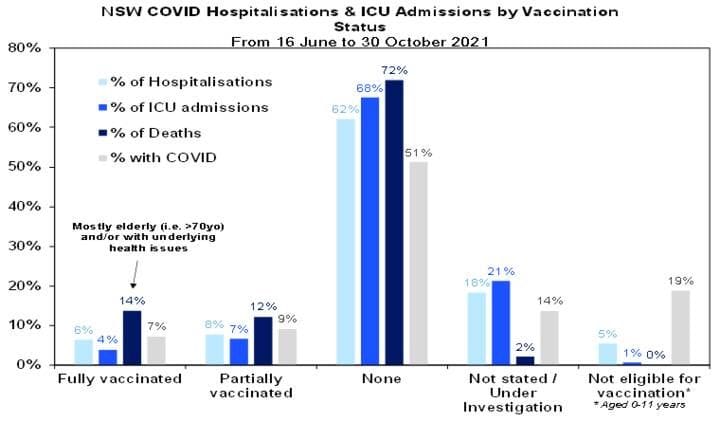

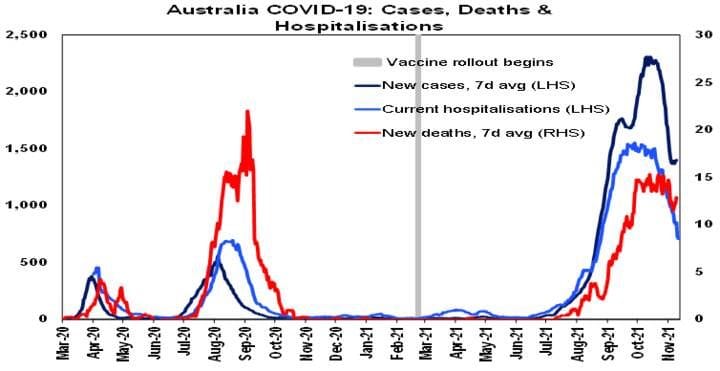

- Vaccination is continuing to keep serious illness down in Australia. Coronavirus case data for NSW shows that the fully vaccinated continue to make up a low proportion of cases, hospitalisations and deaths (despite now being 76% of the total NSW population) and the level of deaths is running below 20% of the level predicted on the basis of the previous wave.

Source: NSW Health, AMP Capital

- The main risk in Australia is a resurgence in new cases following reopening threatening to overwhelm the hospital system necessitating some reversal in reopening. So far so good and a rapid deployment of booster shots to those vaccinated 5 or 6 months ago could minimise the risk. But there are some signs the number of new cases in Australia has stopped falling and the experience in the US, UK, Europe, Singapore and Israel suggests that the risk of a rebound in cases high. Key to watch in the event of such a resurgence will be hospitalisations and deaths – if hospitals can cope then a return to hard lockdowns can be avoided. The UK and Singaporean experience suggests reason for optimism as vaccines have helped keep serious illness subdued.

Source: ourworldindata.org, AMP Capital

Economic activity trackers

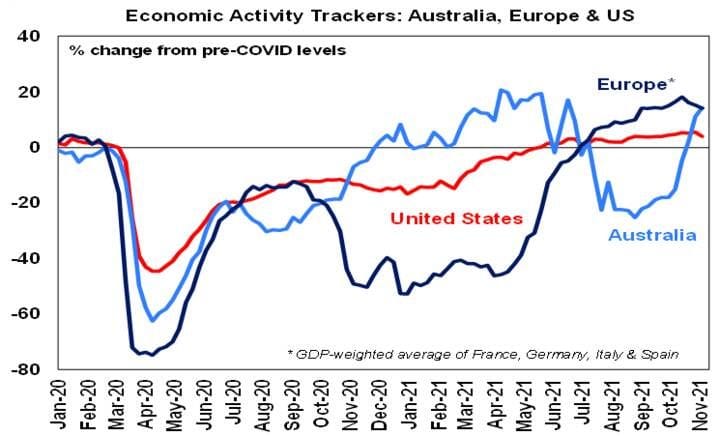

- Our Australian Economic Activity Tracker rose again over the last week with a continuing broad-based improvement in confidence, restaurant and hotel bookings, card transactions, mobility, shopper traffic and job ads. It’s nearly back to pre-Delta levels and is likely to move higher in the months ahead as reopening continues although risks around reopening driving increased cases and associated setbacks could constrain it at times. Expect a strong rebound in December quarter GDP. By contrast the European & US Economic Activity Trackers dipped with supply bottlenecks and covid cases weighing.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP Capital

Major global economic events and implications

- Mixed US economic data but inflation up again. US economic activity data was mixed with a fall in small business confidence but a continuing downtrend in jobless claims. The main concern though is that CPI inflation accelerated further in October to 6.2%yoy which is its highest since 1990 and price increases have broadened out from the reopening driven increases seen in the June quarter (eg, vehicle prices, vehicle rental and hotel costs) resulting in median inflation pushing up to 3.1%yoy. A further surge in producer price inflation to 8.6%yoy and continuing high price and cost pressure readings in business surveys suggest inflation will stay up for a while yet.

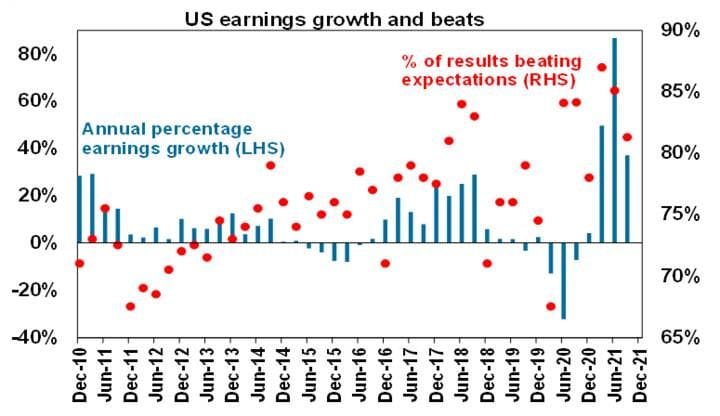

- US September quarter earnings have come in 9% stronger than expected. 92% of S&P 500 companies have now reported September quarter earnings and 81% have exceeded expectations with an average beat of 9%. Earnings growth has slowed due to base effects but at around 38%yoy for the quarter is well up from expectations for a 29%yoy rise at the start of reporting season. The US share market has now rallied through each of the last seven reporting seasons.

Source: Bloomberg, AMP Capital

- Japanese confidence rose sharply in October according to the Eco Watchers survey reflecting an easing of coronavirus restrictions. Producer price inflation also accelerated to 8%yoy, but the flow through to consumer prices is likely to remain weak particularly with wages growth slowing to just 0.2%yoy.

- Chinese economic data was mixed with stronger than expected exports, weaker than expected imports and credit growth looking like it may have bottomed at 10%yoy. Producer price inflation surged further to 13.5%yoy but consumer price inflation remains weak at 1.5%yoy.

- Green monetary easing from the China’s PBOC? The PBOC’s green monetary facility which will see low cost funds going to banks that lend to green projects is a defacto monetary easing. While it appears to have no limit it’s hard to know how significant it will be in terms of boosting total lending growth.

Australian economic events and implications

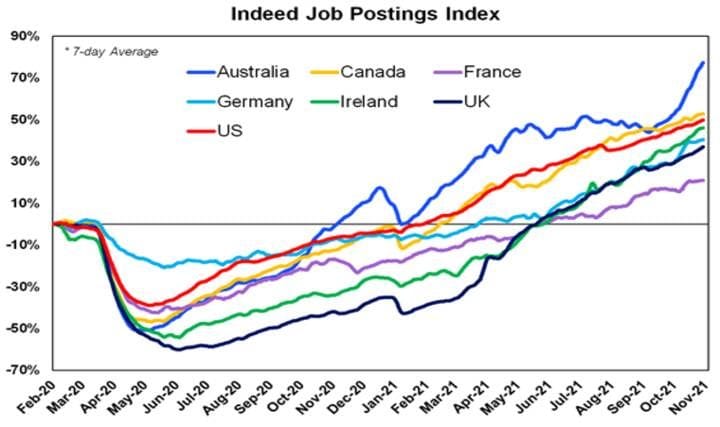

- More noise than signal from Australian jobs data for October. Employment surprisingly fell and unemployment surprisingly rose – but this was because the labour force survey period ended on 9th October which was before reopening in NSW and Victoria and so the lockdowns still weighed on employment and yet participation rose as workers started to return in anticipation of reopening. With reopening now well underway expect to see a sharp rebound in employment starting in November of at least 150,000 jobs. Job vacancies are strong and payroll jobs have started to rebound. And the ABS has noted that there are 537,000 people who considered that they were attached to a job but were not actually working or in the labour force. This compares to 197,000 in October 2019 (ie pre covid) suggesting that as the economy recovers there are many who will return to being defined as employed and in the workforce. So while the unemployment rate is likely to be messy around 5% into year-end (depending on what recovers fastest – employment or participation), by end next year it’s likely to see it around 4% and that the first RBA rate hike will come around November next year.

Source: Indeed, AMP Capital

- Meanwhile, business conditions and confidence are up – more so for businesses than consumers, but even the latter is above long-term average levels.

What to watch over the next week?

- In the US, expect 0.8% gains in October data for retail sales and industrial production, housing data to show strong home buyer conditions and a rise in housing starts (Wednesday) and solid readings of around +20 for the New York and Philadelphia manufacturing indexes.

- Japanese September quarter GDP is expected to show a 0.2%qoq decline reflecting a surge in coronavirus cases. Since then restrictions have eased so GDP should rebound.

- Chinese activity data for October is likely to show a further modest slowing in retail sales growth (to 3.8%yoy), industrial production (to 3%yoy) and investment (to 6.2%yoy).

Outlook for investment markets

- Shares remain vulnerable to short-term volatility with possible triggers being coronavirus, global supply constraints & the inflation scare, less dovish central banks, the US debt ceiling and the slowing Chinese economy. But we are now coming into a stronger period seasonally for shares and the combination of solid global growth and earnings, vaccines allowing a more sustained reopening and still low interest rates augurs well for shares over the next 12 months.

- Expect the rising trend in bond yields to continue as it becomes clear the global recovery is continuing resulting in capital losses and poor returns from bonds over the next 12 months.

- Unlisted commercial property may still see some weakness in retail and office returns but industrial is likely to be strong. Unlisted infrastructure is expected to see solid returns.

- Australian home prices are likely to rise by around 21% this year before slowing to around 5% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a further slowing in the pace of gains as poor affordability, rising fixed rates, higher interest rate serviceability buffers, reduced home buyer incentives and rising listings impact. Ultimately giving way to a 5-10% price fall in 2023.

- Cash and bank deposits are likely to provide poor returns, given the ultra-low cash rate of 0.1%.

- Although the $A could pull back further in response to tightening US monetary policy and the weak iron ore price, a rising trend is likely over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.80.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer