Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

The FinSec View #21

Issue: Friday 20 November 2020

With today’s announcement comes a revised plan for FinSec. From Monday, half our team will work from home and the other half from the office. We always love to see you at 10 Greenhill Road and as soon as we know where we stand regarding face to face meetings, we will be in touch accordingly. In the interim, we are always happy to meet via Lifesize cloud.

Should people who work from home be levied a higher tax rate?

A new report released by Deutsche Bank has proposed that white-collar staff reaping the financial benefits of working from home should be taxed to help other workers who aren’t getting the same advantages. Needless to say the report has ignited much controversy.The report which examines ways to rebuild the global economy in the wake of the coronavirus pandemic suggests that a 5 per cent daily tax on each employee that continues to work from home (WFH), should do the trick. They estimate it could raise up to $US48 billion in the US alone.

The argument is of course that people who WFH get a benefit in terms of better work/life balance, less travel time and save money (commuting, takeout lunches, buying and dry cleaning work clothes etc.), which in the process hurts the economy. On the flip side it could be argued they are good for the planet as they contribute less to carbon pollution by commuting less, so maybe they should get a tax cut?Perhaps a more likely, rationale is that our societies have already been built to accommodate in-office work. That’s good for real estate and other supporting services (the sandwich shop that supplies lunch for instance) This also just happens to be very good for banks.

In a view we think sums it up quite sensibly, Economist Shane Oliver says

“It’s a whacky idea no matter what. Because if there was a benefit in working from home market forces will work out what it is and it will be priced into wages (ie lower wages relative to those who have to go to into work), the financial saving from working from home will be re-allocated to other forms of spending (like less on wasteful commuting costs and more on holidays) – why should the government need to intervene in all of this with an arbitrary tax”.

Australia’s Retirement Income Review Released

Findings of the much-anticipated retirement income review have been released this morning and are set to reignite the superannuation wars.Concluding that increasing the compulsory superannuation rate could disadvantage low-income earners and cut workers’ lifetime income by 2 per cent, the door is now open for the Morrison government to delay or even scrap the legislated rise (9.5% – 12% by 2025). The government has suggested they will make a final decision on whether to proceed in the May 2021 budget.

The report lends credibility to our own view that ultimately we need to achieve the rate of 12% but, right now and for the foreseeable future both business and consumers are doing it tough. The concern is (a view also held by the The Reserve Bank of Australia) that increasing too soon will inevitably result in a trade-off with employment and real wage growth, both necessary for a return to a healthier economy.More broadly the report has found that the three pillars of Australia’s retirement income system compulsory superannuation, voluntary savings and a means-tested age pension are “effective, sound and broadly sustainable” but too complex, while the dominant role of superannuation contributions is in question. “More efficient use of savings in retirement can have a bigger impact on improving retirement income than increasing the super guarantee (SG)”.

It also pointed strongly towards policies that encouraged greater home ownership and those which allow retirees to unlock equity in their homes to make “the most of their assets when in retirement”.

Our view: A good idea in theory but this is an incredibly complex piece given people’s psychological attachment to their home, their desire to leave it as a nest egg for their children and the basic fact that property valuations differ substantially between cities and regions. There is a bit to play out here.

Chaired by former IMF director and senior Treasury bureaucrat Michael Callaghan with Carolyn Kay and Deborah Ralston, the final report does not make recommendations but instead makes a series of findings on which governments can craft retirement policies.

Key findings of the review include:

- Australia’s retirement system is effective, sound and sustainable but too complex

- The Age Pension provides a social safety net and helps to reduce income inequality

- Without compulsory super, middle income earners would not save enough for retirement

- Higher superannuation contributions come at the cost of lower wage growth

- Increases in the super guarantee benefit high income earners the most

- Accessing home equity is an underutilised opportunity

Reset Button for the Australian Insurance Market

In recent times Australian Income Insurers have struggled to balance the need to offer competitive policies with sustainable premiums and meet their claims expectations. Higher than expected claims experiences have resulted in a loss of $3.4 billion over the last 5 years and $1.35 billion since the December quarter alone.

An extremely competitive market, to date insurers have chosen to protect their market share rather than address the problem. Consequently, APRA has stepped in to hand down its own sustainability measures for Australian Insurers to adopt.

What does this mean for you?

For those of you with existing policies in place, the insurer cannot negatively change the policy terms and conditions as long as you continue to fund your insurance premiums. It is likely however, the underlying premium rates for existing policies will increase and a number of new offerings will enter the marketplace – lesser terms in exchange for lower premium rates. For those entering the insurance market it has the propensity to become increasingly harder to find the comprehensive insurance policies of old.

The next 12-18 months will see one of the biggest overhauls of the insurance industry we have witnessed. This, in conjunction with the unintended consequences of the government’s Protecting Your Super reforms and we are left with a situation that only exasperates Australia’s underinsurance problem.

It has never been more important for people to receive advice from a specialist.

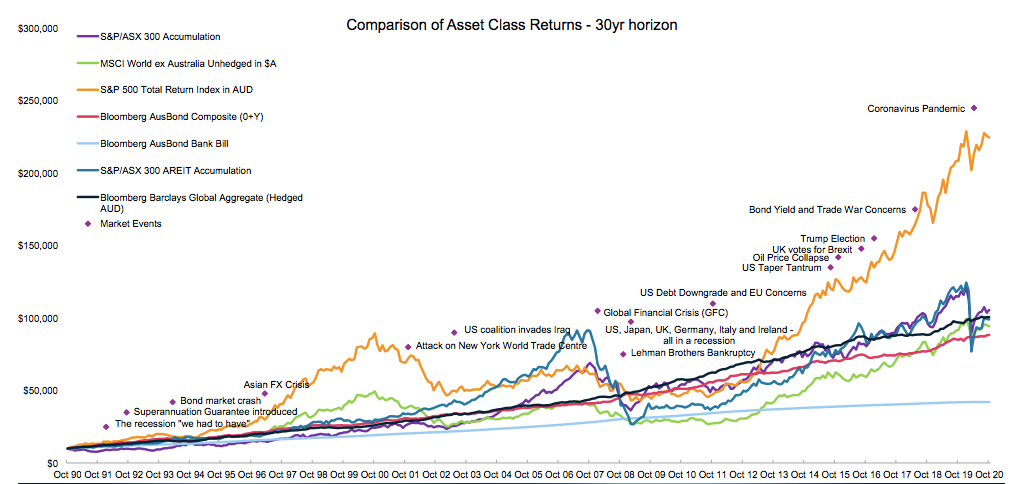

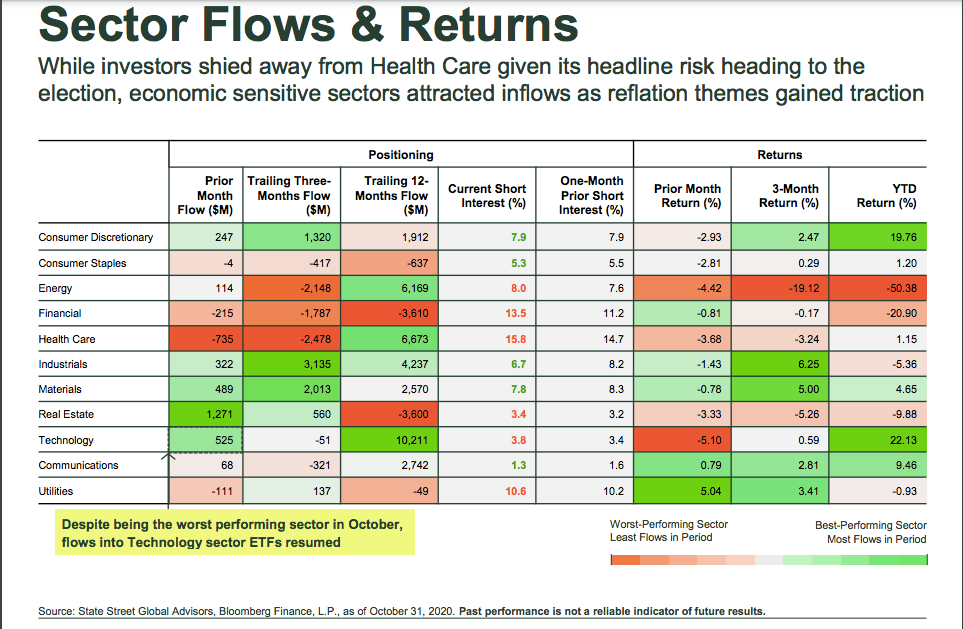

Chart(s) of the Week

Our first chart depicts the value today of $10,000 invested 30 years ago. The extraordinary trajectory of the S&P 500 is a timely reminder as to why diversification across global equity markets, is so important.

Our second chart highlights the big winners and losers of the year, including some impressive COVID pivoters. Far right, represents sector returns year to date (YTD).

A Redefining of our Client Services Team

As we continue to grow, so does our team and too the necessity to adapt our operating model to ensure we continue to deliver the level of service you have come to expect. After months of designing and testing, today we are pleased to announce an exciting enhancement to our team structure.

As of December 2020, our client services team will be re-defined to include both Client Service Administrators (CSAs) and Client Service Officers (CSOs). Whilst they will continue to work as one team, there will be a clear division of duties.

Our CSAs will take responsibility for the day to day administrative functions, e.g. booking meetings, data entry and integrity and document management, leaving our CSOs available to respond to your specific service needs in an agile manner.

What this will mean for you?

You will maintain direct contact with your adviser’s CSO, and they will continue to be your second key relationship in the business. Your CSO will be responsible for implementing your advice and any changes, assisting with your queries and working with your adviser. However, in addition, and when necessary, you will also deal with the CSAs for administrative tasks.

This initiative is founded on our desire to ensure our entire team is engaged, agile and responsive to your needs.