Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View – The long game, robotaxis, alternatives and more

|

Issue: 20th August 2021 |

|

U.S. equities traded in a volatile session overnight, as investors assess the Fed’s likely taper later this year, rising cases of COVID-19 and deaths in the U.S. and ongoing pressure on supply chains. Details from the July meeting of the US central bank showed most policymakers judged that it could be appropriate to start reducing the pace of asset purchases this year, although there was some division over when to start and how quickly to dial back the stimulus. Yesterday’s moves served as a wake-up reminder for just how much markets are conditioned to be running on central bank support. Add to all this some mixed retailer results (US), the havoc in Afghanistan and an apparently weakening Chinese economy and it has been a week to test the mettle of many investors. All said the main indices are still comfortably in positive territory for the year. As NSW’s lockdown drags on with no clear end in sight, and Melbourne reaches over 200 total days in lockdown over the course of the pandemic, many are asking if it’s time to do away with COVID-zero and simply ‘live with the virus’. The sad reality, however, is this just isn’t a choice. The Delta variant is so infectious that we’d lose control and have overwhelming case numbers, ICU admissions and deaths as we’ve seen overseas. It is hard not to recognise just how lucky we are here in South Australia, remembering, however, that it can all turn on a dime. We acknowledge just how tough these times are, and our thoughts are with all those living the inevitable hardship these lockdowns bring! On a brighter note, we wish all Paralympians the best of luck as they begin their Olympic journey on Tuesday. A special mention to Ahmed Kelly, who through the Children First Foundation (at the time sponsored by Associated Planners) has been a friend of FinSec since he was 5 years old. Ahmed’s story can be found here https://www.paralympic.org.au/athlete/ahmed-kelly/

|

|

|

In this article, Phil Ruthven AO (founder of the Ruthven Institute and IBISWorld) takes a broader look at long-term trends in growth, inflation, markets and sectors and implores policymakers to overcome their “short-termism”. A problem he attributes to the West’s diminishing resolve for growth based on the following reasons.

As always, Ruthven’s views are data-driven and insightful. The full article can be read here.

|

|

|

Speaking of long-term views, staying the course isn’t always easy for investors, especially when there’s so much ‘noise’ in the world. But by looking at how markets have performed over time, we can place our current market situation in context and appreciate how our investments can grow in the long term. As the 2021 Vanguard Index Chart shows, while markets do fluctuate, asset values have steadily increased over the last 30 years. We can’t control how markets behave, but by setting a clear plan, diversifying across multiple asset classes, and minimising costs, we can stay in control of what matters: our long-term investment strategy. Download ‘The power of perspective – 2021 Vanguard Index Chart’ here.

|

|

|

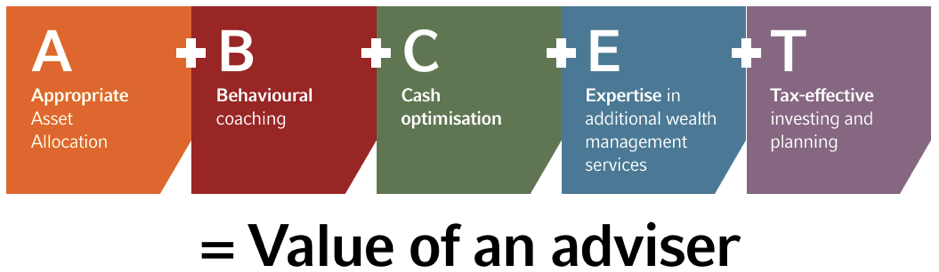

A new report by Russel Investments has put a definitive number on the value of a financial adviser during the market’s most tumultuous days of the COVID-19 pandemic. According to the report (Value of an Adviser Report), the portfolio of advised Australians was approximately 5.2 per cent better off last year than the non-advised. Not surprisingly, the biggest knowledge gaps were reported as asset allocation and market timing. “Often, non-advised investors are tempted to chase performance and overreact to market events, like the sudden periods of market volatility witnessed in recent times,” said Russell Investments’ director, head of business solutions, Bronwyn Yates. In a welcome sign, the report also notes that investors across generations are becoming more engaged with their finances. On the flip side, however, is the rising ranks of Millennials and Gen Z turning to ‘fintok’ and ‘finfluencers’ as the source of their financial advice. The latest iteration in a long line of consumers sharing views about financial markets, not unlike “taxi drivers giving stock tips” or “the bloke down at the pub who wants to tell you all about the really great company he just invested in” (Minister Jane Hume), this unregulated advice is, of course, an inevitable part of a modern financial ecosystem. Unfortunately, however, it was much of this cohort that faired the worst during the market volatility. ASIC estimates that from new or re-activated share trading accounts in the early days of COVID, over $230 million worth of losses were incurred by new retail investors. Making education more important than ever! As the Finsec formula touts when it comes to investing Knowledge + Clarity = Confidence. Beyond the material value of financial advice, investors who have been educated by a professional adviser will inevitably make more informed decisions throughout their investment journey.

|

|

|

Last View, we talked semiconductors. This week it’s autonomous vehicles in part 2 of our Capital Group series on the 10 most exciting (and in some cases life-changing) developments they believe will shape the world to come. Ready for a ride in your robotaxi? Imagine getting into your car, typing—or, better yet speaking—a location into your vehicle’s interface, then letting it drive you to your destination while you read a book, surf the web, or even take a quick nap. Self-driving vehicles—the stuff of science fiction since the first roads were paved—are coming, and they’re going to radically change what it’s like to get from point A to point B. Equity portfolio manager Chris Buchbinder believes that in 2030 we will have broadly deployed fleets of autonomous electric vehicles operating in cities throughout the world. “Ownership of a personal vehicle will go from being a necessity to a luxury. Many people will still have vehicles — just like people ride horses or bicycles for fun —but they will no longer be necessary as a primary form of transportation in major cities. “This is an area I believe the market has yet to fully appreciate. At the moment, the market leaders are embedded in other companies — such as Alphabet’s Waymo, Amazon’s Zoox or the Cruise division of GM — so investors can’t buy a pure-play autonomous driving company. But as these fleets roll out more publicly, the market should start to re-evaluate these companies and realise this is a real business, not a science project. As vehicles become more about technological components and less about traditional manufacturing, winners will emerge from a variety of industries. “I also think 2030 is when we’re likely to see hybrid electric engines and hydrogen engines introduced into commercial aircraft, with widespread deployment over the following 5 to 10 years. The impact on global emissions could be significant if we transition to a world with autonomous electric vehicles on the road and aircraft transportation shifting from oil-based fuel to a mixture of oil, electricity and hydrogen.”

The hype around driverless cars has grown rapidly over the past several years, with many big technology companies (as mentioned above) getting behind the concept. With the adoption of any new revolutionary technology, it is predicted there will be problems for businesses that don’t adjust fast enough to future developments. Futurists estimate that hundreds of billions of dollars (if not trillions) could be lost by automakers, suppliers, dealers, parking companies, and many other car-related enterprises. And think of the lost revenue for personal injury lawyers and the profound impact on insurance companies. After all, who needs a car made with heavier-gauge steel and eight airbags if accidents are so rare? Who needs a parking spot close to work if your car can drive you there, park itself miles away, only to pick you up later? However it plays out, these vehicles are coming— their full adoption will take decades, but their convenience, cost, safety, and other factors will make them ubiquitous and indispensable. Such as with any technological revolution, the companies that plan ahead, adjust the fastest and imagine the biggest will survive and thrive. And companies invested in old technology and practices will need to evolve or risk dying.

|

|

|

A recent survey by JLL has revealed that across the world’s biggest cities, 56% of companies are waiting until the second half of 2021 to make a decision on whether or not to return to the office. And when they do, many have indicated that the hybrid model (employees having the option of working remotely for part of each week) will be the new order. Interestingly, half of the firms surveyed indicated that if and when they do return, they expect to increase the amount of floor space per person by as much as 20% for the obvious health and hygiene factors but primarily to accommodate different styles of working in particular collaborative spaces. In Australia, as outbreaks have eased, office occupancy rates have risen. Although, even in those cities relatively unscathed by COVID, occupancy is still 10 per cent to 30 per cent lower than before the pandemic (source: RBA). Of course, the full picture won’t properly emerge because of the long length of many existing office leases, which will likely take a number of years to resolve. Does the office have a place in a post-pandemic world? In our view, the office isn’t dead – it’s just evolving. People still crave the collaboration and interaction that comes with an office environment. And, while employees have learned that they can be productive remotely, what is fundamentally missing is human cohesion, the bringing together of a diverse array of ideas, people and experiences to inspire creativity. Research shows that the human need to be together is as essential as ever for fortifying workplace community, social relationships, and a company’s mission and culture. As the world moves towards the hybrid model, it’s our view that the purpose of the office will definitely evolve but not diminish. People used to leave the office to achieve work-life balance. Perhaps in a post COVID world, people will now go to the office to achieve work-life balance… Some of the key global trends affecting the core office market going forward.

|

|

|

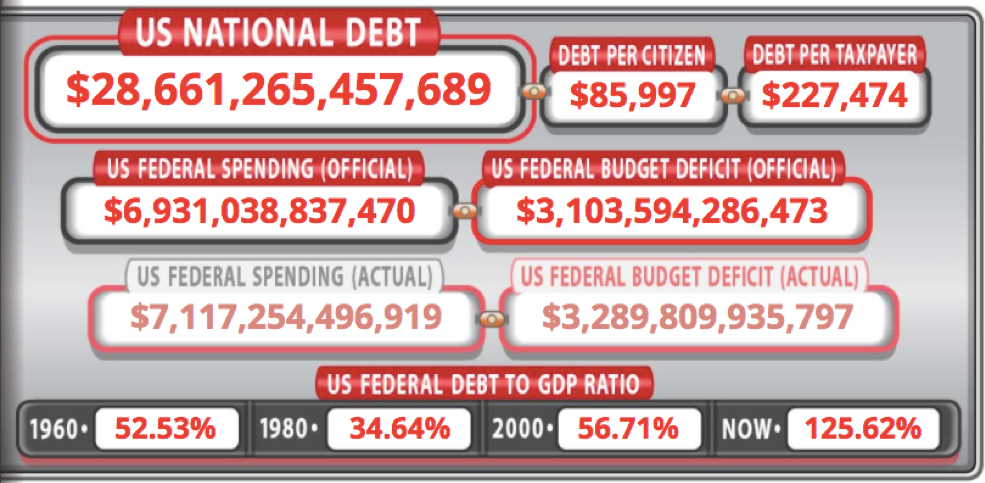

It’s fascinating to watch the US debt clock in real time. Faster than you can take a screenshot it’s out of date. National debt is nearly at US$29 trillion, an increase of US$5 trillion in the last year. It is estimated to reach US$89 trillion by 2029, even without the US$1.5 trillion infrastructure bill recently approved and a coming US$3.5 trillion antipoverty and climate change plan. The US Congressional Budget Office projects that US GDP will reach US$34 trillion in 10 years. In this context, what’s a few trillion on some decent roads? Such big numbers we’ve become inured to them! You can find the live US debt clock by clicking here.

|

|

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser. |