Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View #19

Issue: Friday 16 October 2020

Federal Budget 2020 – 2021 – What Lies Ahead

This year’s Federal Budget (6 October 2020) saw an enormous spending and borrowing binge of war-time proportions. On a mission to plug the economic hole left by lockdown measures in the fight against COVID, this budget is all about recovery.

Recovery will cost a record $213.7bn this financial year, around 11% of GDP with further deficits extending into the never-never (experts are touting we will see gross debt reach more than $1 trillion over the next few years).

The focus of the recovery budget is heavily on business with incentives, massive tax cuts on investment and a herculean focus on job growth designed to move people from jobkeeper back into employment. For individuals, you would have seen the bringing forward of income tax cuts.

The stimulus is a no brainer, and while debt has grown significantly, interest rates are low and our capacity for debt is still manageable (we carry much less than the rest of the West). In short, the stimulus had to happen. The long lens of the 2021 budget is firmly focused on the golden goose of repair which involves reining in unemployment levels (let’s say below 6%) and inching back to a surplus, albeit with big implications for the next generation. Of course, our recovery relies on a return to business as usual, which translates to overseas tourism, international students and more than anything immigration let’s hope the vaccine we’re all factoring in eventuates.

What does it mean for markets

From an investor perspective, we are less concerned with grand debates about whether deficits are inherently good or bad, nor about inter-generational inequity, rather we are interested primarily in whether it will be enough to maintain market confidence while the economy recovers?

With the help of central banks, it’s worked so far! Australia’s rare AAA credit rating and relatively low debt level afford us the capacity to take on more. As long as the government maintains some fiscal discipline, the current spending plans should be enough to ‘keep the party going’, for now.

This said The ASX always has and most likely always will follow the US markets. How the US fares through the upcoming election, and it’s stimulus negotiations (The Coronavirus Aid, Relief, and Economic Security Act ‘CARES Act’) will play a big part.

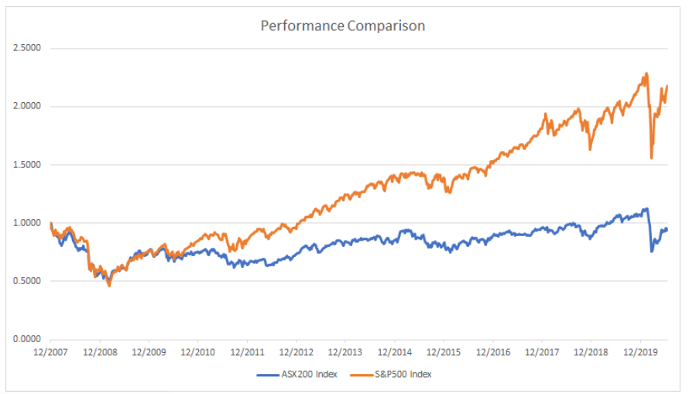

Market Update

The September quarter was a good one for global share markets on the whole, returning +8% in US dollar terms, although the month of September was down -3%. Global share markets are now ahead (just) for the 2020 year to date so they have now recovered from the sharp coronavirus sell-off in February-March. Not bad for the deepest economic contraction since the 1930s Great Depression. The rebound has of course been due to a tidal wave of support from governments and their central banks.

Tech stocks in China and the US are the market winners with oil/gas stocks the biggest losers, followed by banks hurt by rising bad debts from the virus lockdowns, margin squeeze from zero/negative interest rates, plus huge (self-inflicted) regulatory penalties.

At the time of writing The S&P 500 index has retreated for a second day on vanishing hopes that a fiscal stimulus deal can be inked before the US election.

US Election update: Can you hold your breath for 18 days?

Analysts and investors worldwide will be holding theirs! The outcome of the election will take the world’s biggest economy in opposite directions. Deep inhale.

At this stage pundits have Biden ahead, and markets are reacting positively as a result.

The current theory (which could change at any time) is that a Biden-Democrat outcome for President and Senate appears to be the most bullish outcome, but a Biden-Republican outcome the most bearish. A second term for Trump would probably be just as volatile as the first.

One target that has been smashed this election is Joe Biden’s fundraising goals as he swanned into October with $432 million in the bank. Online donations have become key with Biden who has even capitalised on a fly that upstaged the Vice Presidential debate by landing on Mike Pence’s head and remaining for several minutes. Within 2 hours of the debate concluding, Biden was selling $10 “Truth Over Flies” swatters and within a few more hours had sold out (nearly 35,000 swatters.) Thanks in part to Louis the fly, Biden is greatly outspending Trump in advertising as their campaigns near the end.

We wait for the exhale.

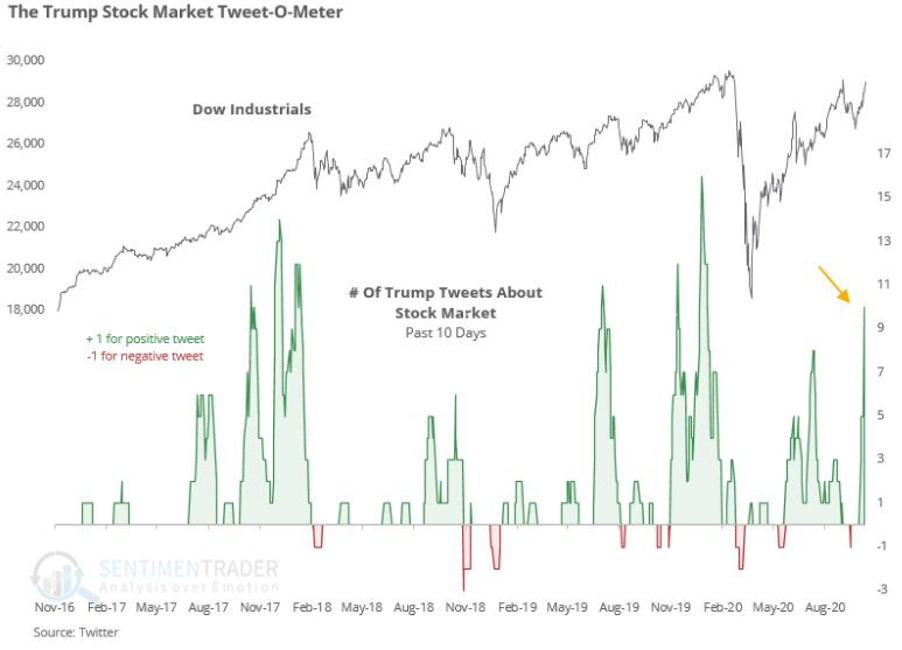

Chart of the Week

Trump’s tweet-o-meter celebrated a lull during his COVID treatment recently, sending the people (and algorithms) who screen them into a nail biting frenzy. The chart of the week plots the effect Trumps ‘good stock market tweets’ versus the ‘not so good tweets’ against the Dow Jones.

17.9 million dollar super saver?

“By 1 July 2021, MySuper products will be subject to an annual performance test. If a fund is deemed to be underperforming, it will need to inform its members of its underperformance by 1 October 2021. When funds inform their members about their underperformance they will also be required to provide them with information about the YourSuper comparison tool. Underperforming funds will be listed as underperforming on the YourSuper comparison tool until their performance improves. Funds that fail two consecutive annual underperformance tests will not be permitted to accept new members. These funds will not be able to re-open to new members unless their performance improves. By 1 July 2022, annual performance tests will be extended to other superannuation products.”

The government says that “Once implemented, these measures will benefit Australians by $17.9 billion over the next 10 years.” Can it really?

Comparing super fund performance is a far cry from comparing apples with apples, which makes for a confusing and possibly misleading new tool for the general public.

As the MySuper Product Heatmap already produced by the Australian Prudential Regulation Authority (APRA) shows, comparisons and disclosures are difficult to understand. Independent research suggests that most superannuants struggle with even the most basic aspects of adjusting performance for risk.

On disclosures, the Australian Securities & Investment Commission (ASIC) recently stated:

“Disclosure cannot solve complexity that is inherent in products and processes. Simplifying disclosure, for example, does not reduce the underlying complexity in financial products and services. Nor does it ease the contextual and emotional dimensions of financial decision making, both at the point of purchase and over time.”

There are legions of factors influencing performance – defensive versus growth assets, growth versus value style or even funds built on investment philosophies with purpose driven mandates – Take for instance a fund manager that takes a strong sustainability position against fossil fuels just as oil prices rise rapidly. Is the fund manager and its members to be punished for attempting to reduce carbons? Mmm… “Everything is paradox. The danger is one dimensional thinking” (Lesley Hazleton) comes to mind here.

The fear is that superannuation fund trustees become so worried about the fund closing to new members and the shame of public underperformance that they stop the investment team backing its views. Not to mention the behaviours it may indirectly encourage (imagine the pressure of being a valuer for an underperforming fund holding hard assets).

Aspects of the Government package, such as reducing fund duplication and creating efficiency, are to be commended, but we can’t help but think the performance comparison component will be the bearer of unintended consequences.

Limelight on Aged Care

For people looking for an alternative to aged care facilities, the budget has offered some pleasing morsels. A Capital Gains Tax exemption for granny flat arrangements where there is a formal written agreement in place is expected to start in July 2021.

The budget also provides $1.6 billion for an additional 23,000 home-care packages which is still well short of the investment required to clear the backlog (more than 100,000 people remain on the waitlist). And it would seem all ideas are on the table. Former Prime Minister Paul Keating suggests that the problem could be solved through a similar mechanism to the Higher Education Contribution Scheme (HECS), that is, the Government could claim any aged care costs owed against the assets of the estate. Whilst we need to find a dignified way to fund the care needs our ageing population, we can’t help but feel this idea sounds more like a death duty.

The reality is, that whilst all things COVID are foremost in our mind, we still have the rest of our lives to manage and aged care is a very real part of this. We would all like to live happily and healthily in our own homes, but a more likely reality is declining health and later-life challenges. The spotlight may be firmly on aged care but it remains a funding grey area.