Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A Finsec View #16

Issue: Friday 04 September 2020

Australia Enters Recession

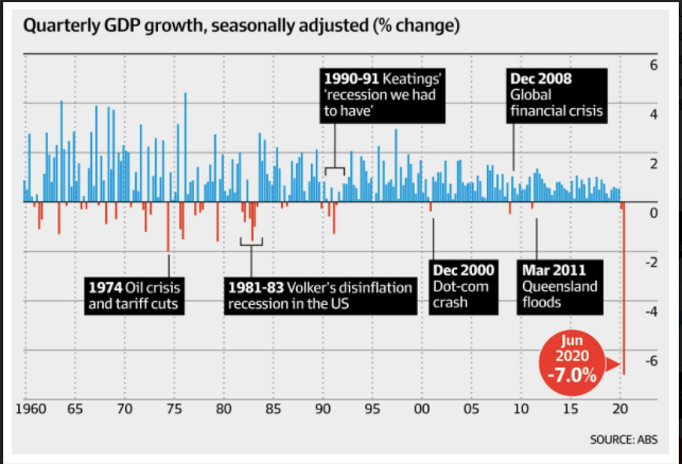

Australia is officially in recession for the first time since 1991 after posting a 7% fall in GDP for the June quarter. The ‘official’ definition of a recession is two consecutive quarters of negative growth, and the June contraction follows a 0.3% decline in the March quarter, bringing a remarkable run to an end.

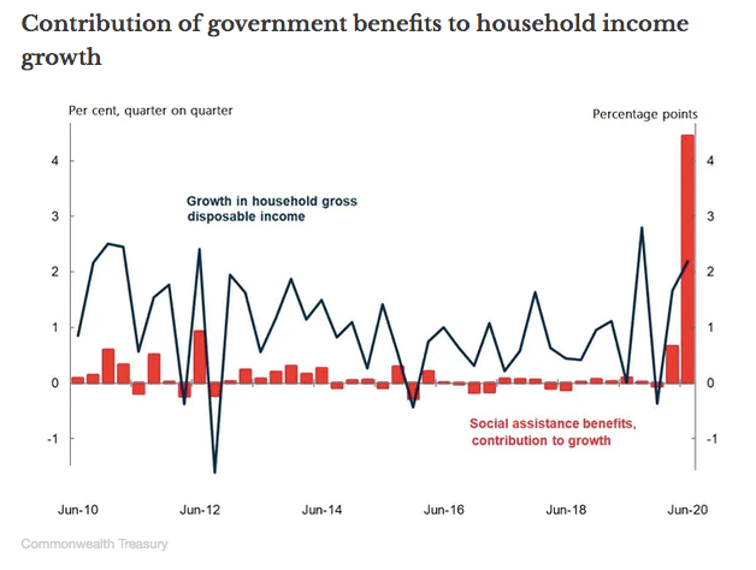

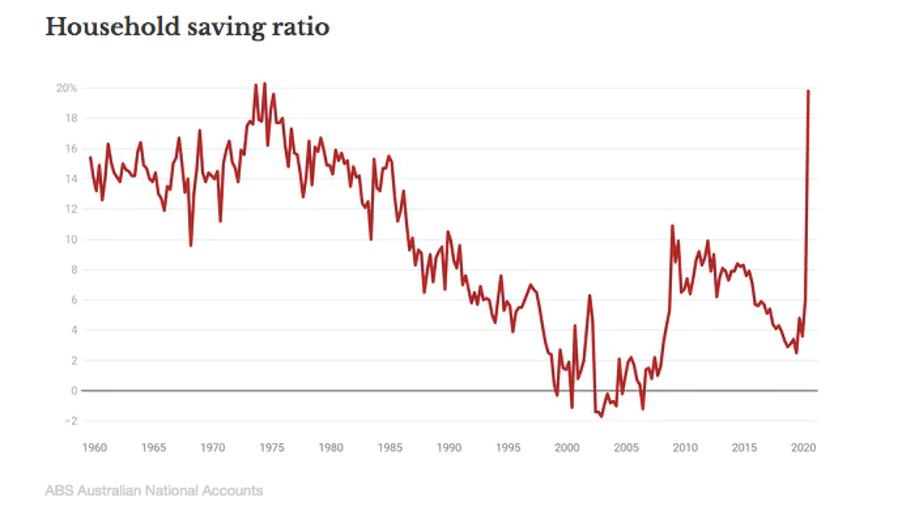

However, the data release revealed some bright spots. The national savings rate rose to 20% from 6% and companies had a record quarter, mainly because of the various government support packages. Remarkably, household income actually rose slightly due to the social assistance benefits.

The Outlook

The outlook will rely on confidence, namely consumers willing to spend and businesses willing to invest Given the current state of the world it’s a hard one to predict and a reality that Treasurer, Josh Frydenberg seems to acknowledge.

This said, his review remains optimistic in that for the next quarter, (encompassing the three months to the end of September), the Treasury is expecting economic activity to shrink only a little further or no further at all.

A lot depends on how soon Victoria’s Stage 4 restrictions and other restrictions are eased, which like everything to do with this virus means a lot depends on things that are unknown.

From an investment perspective, the treasurer will deliver the budget in a little over four weeks. He has announced that a key part of this will be measures to make it easier for businesses to do business, unlocking “entrepreneurship and innovation” at low cost.

Whilst the Reserve Bank (Tuesday) made available an extra $57 billion at low cost for banks to advance businesses and households, businesses are only likely to want to invest more when they can see returns.

Propping up our economy at present, or as former Reserve Bank economist Callam Pickering called it “holding it together with duct tape” is JobKeeper and JobSeeker. At his press conference, Frydenberg resisted suggestions that he will revisit the wind-downs of the Coronavirus Supplements due to take place over the next six months.

But, with the Victorian situation far worse than when he announced the original schedule (late July), he might find there’s a case for more duct tape, for a while longer.

A Note on Markets

At time of going to print the volatility we’ve been predicting reared it’s head in US markets overnight, followed by around a 3% loss in Australia. We wait with bated breath to see how it plays out tonight. Further context to come in our Weekly Market Update on Monday.

Dow Jones

This week the company with the longest record in the Dow Jones Industrial Average (DJIA), Exxon Mobil fell out of the index and was replaced by a software company, Salesforce. A historic sign of the times indeed!

Established in 1896, this historical barometer became the first index of stock market activity, when Charles Dow and his business associate Edward Jones chose the 12 most influential corporations of the day, added up their stock prices and divided by 12. In 1928 the index increased to 30 stocks where it remains today, still carrying enormous influence.

Interestingly only one of the original companies comprising the index exists today, General Electric. The other companies include: Salesforce, Procter & Gamble, DowDuPont, Amgen, 3M, IBM, Merck, American Express, McDonald’s, Boeing, Coca-Cola, Caterpillar, JPMorgan Chase, Walt Disney, Johnson & Johnson, Walmart, Home Depot, Intel, Microsoft, Honeywell, Verizon, Chevron, Cisco Systems, Travelers Cos, UnitedHealth Group, Goldman Sachs, Nike, Visa, Apple, Walgreens Boots.

The members of the Dow have changed only rarely in recent years. While Apple was added in 2015 and Nike and Goldman Sachs gained entry in 2013, the majority of companies within the Dow on Monday had been in the index for more than 10 years.

Whilst the relevance of the index is subjective (in modern terms), it is certainly a ‘who’s who’ of household names and it’s hard to imagine any of these companies ceasing to exist. A sentiment we’re sure our ancestors shared over 100 years ago, when considering the line-up back then.

Observations on the Bipartisan War on Super

The fires of the superannuation debate were further fuelled this week.

Paul Keating turned up the heat claiming the Liberal Party wants to end compulsory super.

“Not take a chink out of it, but to actually destroy it. They intend to do this in two ways. That is, they want to drain money out of the bottom of the system, and stop money coming into the top of the system … This malarky they talk of, ‘if they take it in super, they won’t get it in wages’, there’s been no wages growth for eight years and there’s not going to be.”

Ex-Labor PM, Kevin Rudd, also weighed in, which caused Senator Jane Hume to take to the airwaves shrugging off the attack by referring to Labor opening “the crypt”.

“I find it quite extraordinary that the Labor Party feel the need to open the crypt and bring out two former PMs to essentially fight an ideological battle,”

As we predicted last view, the arguments have a long way to play out.

For those seeking background, please click here to read our recent article ‘Super is back’

Risky Business

Another hot topic of debate, this one among economists, is between the proponents of MMT and more conventional economics. A topic we’ve covered a few times in recent views,

The debate centres around whether printing money is actually radical at all. The argument being what is the difference between central banks buying second-hand government bonds and paying for them merely by crediting the seller’s bank account “quantitative easing” vis-à-vis printing money?

In this article Economist Ross Gittins (Sydney Morning Herald) brings it back to simple demand for real resources. He outlines, in his opinion why “letting politicians off the leash to spend as much as they like” (AKA printing money) is risky business.

Video of the week

A brilliant take on Quantitative Easing from The late John Clarke and Bryan Dawe – Circa 2012.

Happy Fathers Day – Wishing all of the fathers within the FinSec community the happiest of days this Sunday!

Enjoy your weekend and as always, if you have any concerns or questions at any time, please reach out to your FinSec adviser.