Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

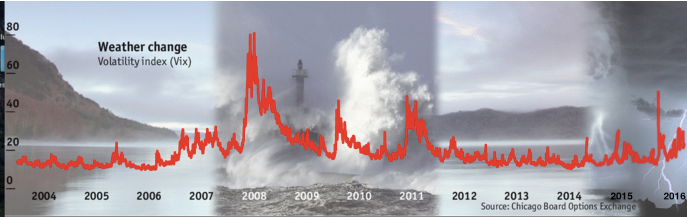

2016 The Year of Volatility

Given the relentless media coverage of the issue, it will come as no surprise that markets have been in a state of volatility since the start of the year. This volatility comes off the back of the second half of 2015, seeing a 10% reduction in the value of the Australian market. So all in all, not a market that is causing investors to sleep without a tad of anxiety.

Having mentioned the media, let’s not forget that good news doesn’t sell papers, make ratings or lead to web site hits. So, the abundance of bad news has been a boon for the news cycle.

So, where to from here? There is no doubt that the world is still grappling with the ongoing issues that caused the financial crisis of 2008. The GFC, as it is commonly known, was fuelled by debt which, in the main, remains. In the regulators’ attempts to avoid financial Armageddon, more debt (cheap debt) was introduced. Recently there has been commentary about $200 trillion of debt, which will never be repaid. Whilst this is a wonderful headline, it fails to mention that with current low interest rates, debt repayment doesn’t make sense. We must, as a result, focus on borrower’s capacity to meet their interest obligations and, in the majority of cases, they are coping.

Central banks have printed money to kick start economic activity and lift inflation. Over time, this will dilute the real value of all this debt. But falling commodity prices around the world have acted as a foil for this desired inflation. It has also sharpened the focus on the ability of commodity revenue dependant emerging economies, to service their debt. This is further complicated by the rising US dollar, given much of their debt is US denominated.

These are all reasonable arguments to justify some anxiety in markets. But let’s reset.

The US economy has turned a corner. Housing has recovered, the unemployment rate is less than 5% (which purists would argue is full employment), the Federal Reserve has had the confidence to raise interest rates (albeit only once at this stage) and company profits are growing. Europe appears finally, to be getting its act together and may well yet “muddle through”.

China is in transition and its economic growth is slowing, however, there are still hundreds of millions to the urbanised. It is fair to say China’s internal consumer demand is yet to gain momentum, and their government continues a “whatever it takes” approach to maintaining their status as the wunderkind of the East! Lets’ not forget that China has doubled the size of its economy over the last 10 years meaning growth at today’s rate of 6.5%pa, is still creating more new wealth than when it was growing at 10%pa, 10 years ago.

While there are many cultural differences and strategic challenges that will make India’s journey to urbanisation different, it will follow a similar path in that they require the same services and resources available from the Australian economy that China does. This is a good news story for our economy over the longer term.

Much has also been written about the collapse in oil prices which has seen the likes of our local darling, Santos, decimated. What hasn’t been widely written about, however, is why the oil price has collapsed. Demand has moderated, yes, but it’s the growth profile that has moderated, not total consumption. We are still consuming more oil than ever and, as the developing world introduces power stations, motor vehicles, transport infrastructure and industrialisation, fossil fuels will be a staple for the revolution.

The issue for oil is “supply”, and supply has been driven by geopolitics. While trying to kick-start their economy with little left in their monetary policy armoury, it has suited the US Federal Reserve to have oil prices fall. There is speculation that forces have been at work to drive down the cost of energy to compromise Russia’s funding of the Ukraine conflict. Finally, the OPEC nations have a vested interest in challenging the shale oil producers and other higher cost suppliers.

Our view is these political games are near an end and supply will be tapered. This may not result in a return to the prices of three years ago, but it will see a normalisation in the oil price. In turn, this will lead to stabilisation in the valuations for oil producers and their downstream suppliers. It may also deliver the desired modest rise in inflation that will give the US Federal Reserve the confidence to normalise interest rates, and finally reset their economy for the post GFC world.

So what does all this mean?

Our view is that 2016 will continue to be a volatile year with regular swings of 100 points or more a day. Much of the volatility will be driven by the markets response to the US Federal Reserve’s approach to interest rates not long term trends. Hedge fund managers constantly reposition their portfolios based on what they know now and bet on what they think will happen next. The weight of money that flows when these decisions are made has the potential to swing markets wildly, albeit in short bursts. Based on what we can see at this point, we don’t see the market spending too much time below 5000 points on the All Ordinaries Index as a foundation is put in place for growth beyond 2016.

We have had a relatively good run since 2012, where our market bobbed around 4000 points while we digested the implications of the Greek debt crisis. There has been a dearth of volatility throughout the last three years and, in fact, what we are now seeing is a return to more normal market behaviour. There is no doubt blood pressures will be tested through this period of volatility. However, we remain committed to the tenet that the patient and unemotional investor will be rewarded through appropriate diversification across asset classes and markets, aligned with risk profile, pragmatic manager and stock selection and the implementation of good strategy.

I can only hope that by the time this reaches you, things have not changed again!

Author: Andrew Creaser, Managing Partner at FinSec