- In the past few weeks, financial markets have been pricing in aggressive rate hikes from the major central banks over the next year because inflation data has been surprising on the upside. However, this week numerous central banks banded together and pushed back against market pricing which led to a fall in government bond yields, particularly at the front end of the yield curve. US 2-year yields are now at 0.42% from 0.49% a week ago, Germany yield are -0.71% now versus -0.59% last week and Australian yields are 0.67% from 0.77% last week. Sharemarkets benefited from lower odds of near-term rate hikes because this means that monetary settings will remain accommodative which is positive for earnings growth and economic activity. US shares reached a record high again, up by 1.6% this week, Euro shares are 2% higher, Australia is up by 1.4%, Japan is 3.1% higher (which also reflects Prime Minister Kishida preserving his Liberal Democratic Party majority in the election which removed uncertainty for the share market) while Chinese shares fell by 0.8%. Commodity prices took a breather this week with oil prices lower (Brent oil prices are around 6% below their recent peak) as US crude inventories have been rising, metals prices were also weaker with iron ore now just under $100/tonne (this is after reaching around $240/tonne in May). And coal and gas prices continue to be well below recent highs. The $US rose this week and the $A fell to 0.738 US dollars.

- The RBA started the central bank calendar this week. The central bank decided to keep the cash rate on hold at 0.1% (this was expected), continue to buy bonds at the rate of $4bn/week to at “least mid-February 2022” (also expected) but drop its 0.1% yield target for the April 2024 bond. The removal of the yield target reflects expectations of a stronger economy post lockdowns, faster inflation and the RBA’s own expectations of a rate hike occurring before 2024 which diminishes the effectiveness of the yield target. The guidance around a rate hike not expected “before 2024” was replaced with reference to conditions for a hike being bet with a tighter labour market and materially higher wages growth which are “likely to take some time” to be met. This changed guidance is still very far from market pricing of the cash rate which is now predicting three rate hikes over the next year, which is less than where it was before the RBA meeting. While the RBA is probably underestimating upside inflation risks to Australia in 2022, the market is getting carried away with concerns about inflation and being too aggressive in its pricing of hikes. Views see rate hikes starting in a year’s time, with a lift in November 2022 taking the cash rate to 0.25%.

- The US Federal Reserve announced a tapering of asset purchases at this week’s meeting, as expected. Total monthly asset purchases will be reduced from $120bn/month to $105bn (made up of $70bn of Treasury securities and $35bn of mortgage-backed securities) from November, with asset purchases expected to run until mid-2022, although the Fed could adjust its purchases at any time depending on the outlook. The post-meeting statement was balanced and highlighted that the Fed wants to see inflation moderately above 2% “for some time” given the undershoot on inflation over recent years. The Fed still sees the factors lifting inflation to be “transitory” but did sound more uncertain about this. The market is pricing in two Fed rate hikes over the next year.

- Markets were expecting the Bank of England to hike interest rates (but economist consensus was “no change”) but the Committee voted 7-2 to keep the Bank Rate unchanged at 0.1% (a win for the economists!). While the Committee upgraded inflation forecasts over the next few years, there is uncertainty around how the labour market will shape up after the furlough scheme ends which argues for more patience in raising rates, meaning rate hikes are likely in early 2022. While the ECB had their meeting last week, ECB President Lagarde pushed back against market pricing for interest rate hikes in 2022 this week which makes sense given the low growth low inflation environment Europe has been in recent years.

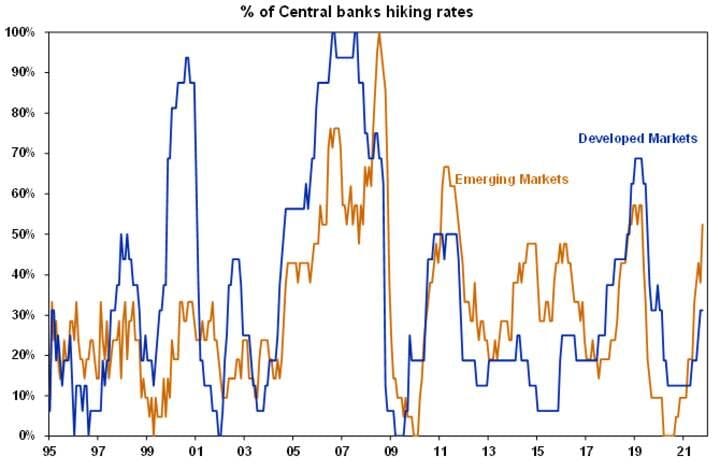

- Emerging market central banks have been hiking interest rates faster than across the developed world (see the chart below). On the BIS count, 52% of emerging market central banks hiked rates in October, compared to 31% of developed markets. In November, this count will increase for the emerging world with the Central Bank of Poland shocking the market this week with a 0.75% increase in interest rates and the Czech National Bank hiking by 1.25% to maintain control of inflation.

Source: BIS, AMP Capital

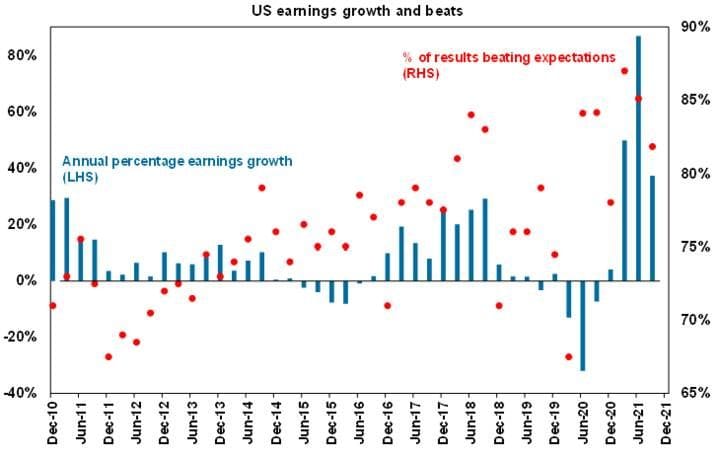

- A positive US third quarter reporting season has been driving sharemarkets higher. Nearly 82% of companies have beaten expectations which is better than the average long-run beat of 76%. Annual earnings growth has slowed to around 37% but this comes off the back of very strong earnings growth in recent periods and is well above the usual growth in annual earnings (see the chart below).

Source: Bloomberg, Credit Suisse, AMP Capital

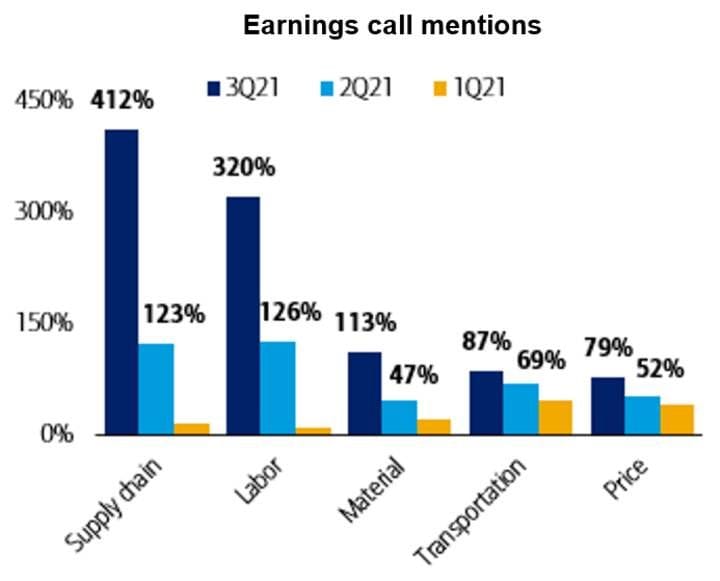

- Strong earnings and profit growth is occurring despite issues of higher inflation and supply chain problems which were mentioned a lot in the earnings results. The chart below shows the increase in mentions of things like “supply chain” and “labour” compared to the last quarter.

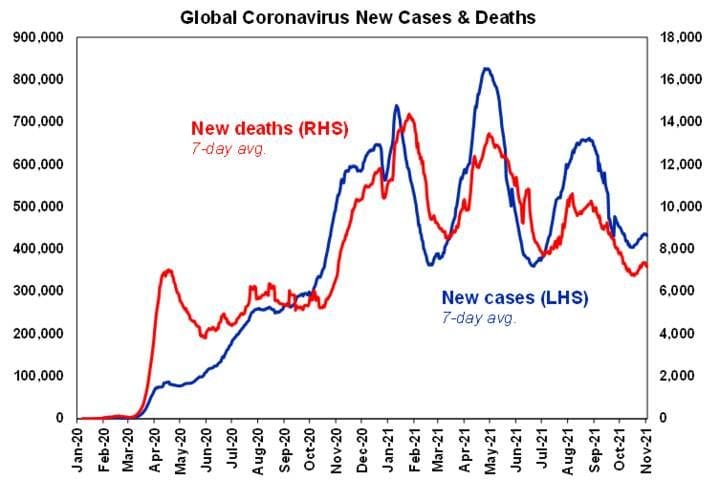

- Global COVID-19 cases have been trending up slightly over recent weeks, but new cases are still running well below prior peaks (see chart below) and deaths are running well below prior waves. In Australia and the UK, deaths are running at less than 20% of the level suggested by the December/January wave, which are all signs that vaccines remain effective.

Source: ourworldindata.org, AMP Capital

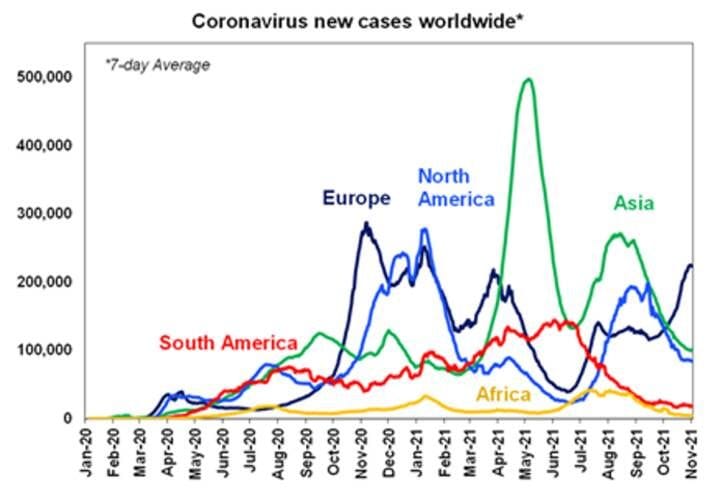

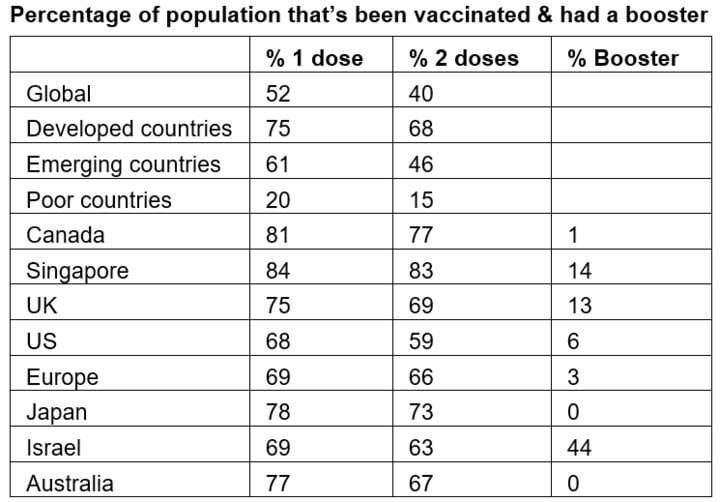

- Most of the recent upswing in new cases has been from Europe (see chart below) particularly in Germany and the UK which is a risk going into the European winter and shows the requirement for booster shots, as Europe started vaccinating its population in early-mid 2021. Europe has given around 2.6% of its population booster shots, while the UK is at 12.6%.

Source: ourworldindata.org, AMP Capital

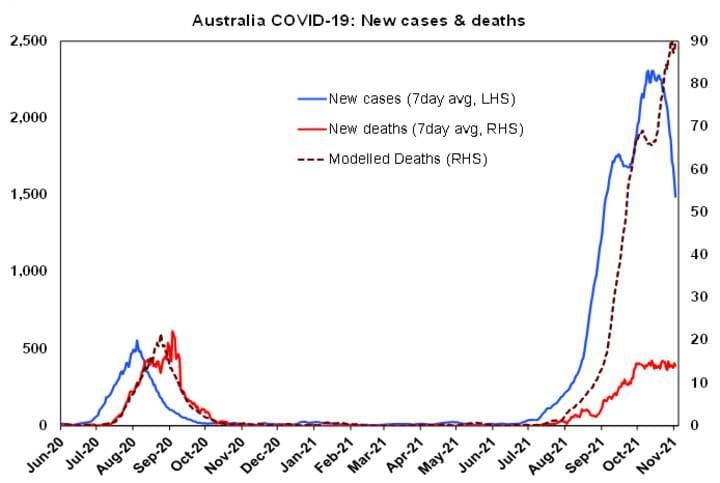

- In Australia, predicted deaths on current case numbers are around 90/day while they are averaging around 14/day.

Source: ourworldindata.org, AMP Capital

- Out of interest, The Economist estimates that the real death toll from COVID-19 is probably closer to 17mn (nearly four times its current level) based on “excess deaths” which is looking at the number of current deaths, compared to what is normal. This is still well below the approximately 50mn killed by the Spanish Flu.

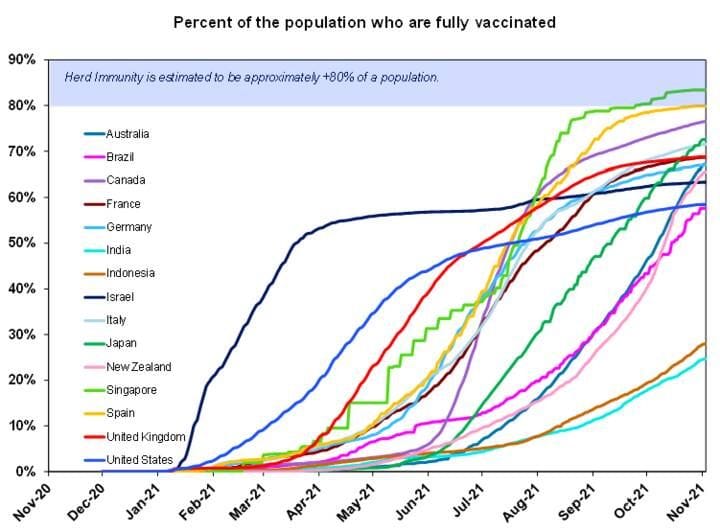

- A lot of countries seem to be reaching a ceiling for vaccinations at around 70% of the total population (see chart below).

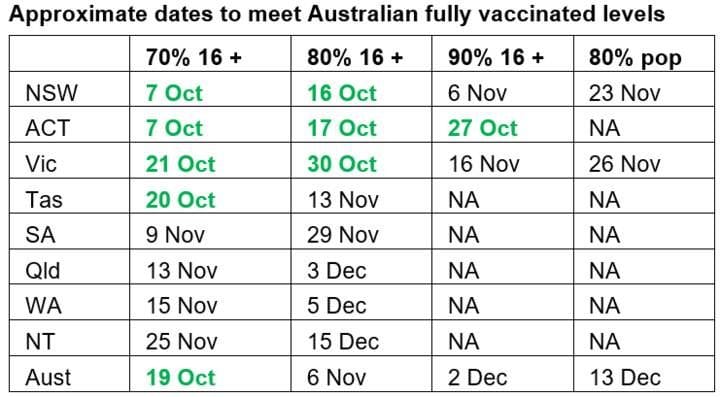

- In this respect, Australia (despite being a late starter) should have at least 80% of its population vaccinated which is currently projected to occur on 13 December (see the second table below).

Source: ourworldindata.org, AMP Capital

Source: covid19data.com.au, AMP Capital

- Once children aged between 5-12 start to be vaccinated (likely to start soon with the US approving a children’s Pfizer vaccine), this will lift the share of global populations vaccinated.

- The NSW government adjusted the reopening roadmap with some further easing of restrictions for those who are fully vaccinated from Monday 8 November, including no limit on the number of visitors to each household, venues allowing more patrons allowed in businesses with one person per two square metres (down from four) and an easing in capacity for outdoor recreation facilities. However, those who are unvaccinated will only be able to exit lockdown when the state reaches 95% vaccination rate for the total population (or December 15, whichever is earlier), which is two weeks later than the originally proposed 1 December (done to increase the vaccine take-up). WA released its plan for living with COVID-19 and is still taking a very conservative approach to opening its borders to the rest of Australia and overseas, which will only happen once 90% of its population aged 12 and older is double vaccinated, this is likely in late January/early February.

- There are still risks with COVID-19 disrupting economic activity including if new variants of the virus that are more immune to vaccines emerge in poor countries (which have lower vaccination rates) and if pockets of outbreaks cause a pause in economic activity (because of targeted lockdowns), especially in important trade regions which is the case recently in China.

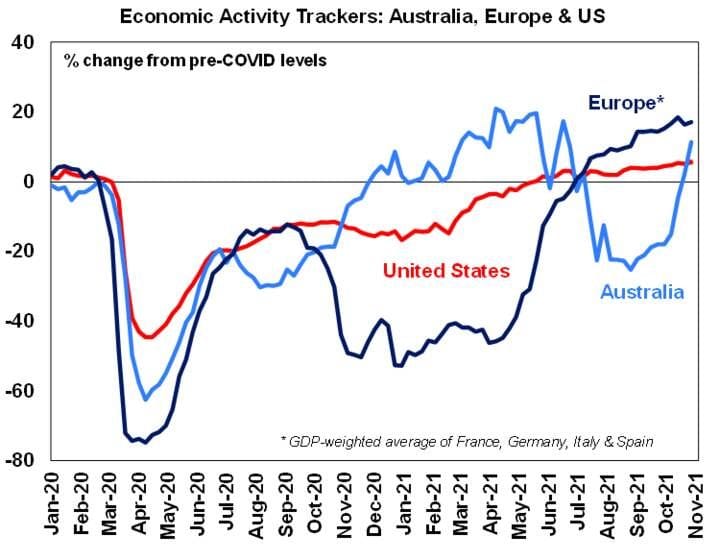

- The economic activity tracker for Australia shot up this week, as re-openings in NSW and Vic continue to lift activity, with a pick up in restaurant bookings, credit card spending, mobility and foot traffic. The Australian tracker is now above the US (and above its pre-COVID levels) which shows the high level of pent-up demand from consumers and means that December quarter GDP is likely to be strong after the fall in the September quarter. The Europe tracker also continues to run above its pre-COVID rate, despite the recent uptick in cases.

Source: ourworldindata.org, AMP Capital

|