Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 28th May 2021

Investment markets and key developments over the past week

- Global share markets rebounded over the last week as inflation fears faded a bit and economic data indicated that the recovery continues. The positive global lead saw the Australian share market shake off worries about the dip in the iron ore price and the latest Victorian snap lockdown and rise to a new record, led by very strong gains in telcos, IT, retail, energy and financial shares. Bond yields actually fell, and the iron ore price continued its correction, but metal and oil prices rose. The $A rose slightly despite a slight rise in the $US.

- More central banks getting a bit hawkish. The Reserve Bank of New Zealand and the Bank of Korea have joined the Bank of Canada and the Bank of England in becoming a bit hawkish. Reserve Bank of New Zealand communication has been erratic and confusing in recent years and that continued at its latest meeting with the RBNZ reinstating its cash rate projections which now show a rate hike from next year which is earlier than most were assuming and upgrading its outlook, but at the same time continuing with dovish commentary around the need for “considerable time and patience” to meet its goals. The RBNZ’s erratic swings make it dangerous to read too much into them let alone project to what it might mean for other central banks, notably the far more stable RBA. But it is consistent with central banks generally becoming more upbeat and inclined to start easing up on the stimulus.

- Fed speakers remain dovish – but the Fed’s “taper talk” is getting closer. Most Fed speakers continue to see the pick-up in inflation as being transitory, but two more officials added weight to the view that if the economy continues to recover as expected then it will be appropriate to begin discussing tapering its bond buying in future meetings. Expect Fed discussion about tapering to get underway in the next three months with tapering starting around year end. But don’t forget that tapering is not monetary tightening, the US share market rose through the 2014 taper and rate hikes are still a long way off – last decade it took two years from the start of tapering in December 2013 to the first rate hike in December 2015.

- There is likely more upside to go on the inflation scare front in the months ahead as base effects, the lagged impact of commodity price hikes and bottlenecks continue to feed through, but there are now a few more signs that it will be transitory. First, we are continuing to see a loss of momentum in commodity prices – partly helped by China’s removal of stimulus and crackdown on commodity speculation. Second, recent US data has surprised on the downside – notably home sales and consumer confidence – suggesting the risk of overheating may be fading a bit. Of course, there is a long way to go yet on this issue, but it partly explains why bond yields in the US and Australia remain relatively calm. And it will support the case for rate hikes being a long way off, even if tapering starts later this year at more central banks.

- Don’t expect the crypto slide to have much of a flow on to other markets or the global economy. Sure, there may be some short-term impact as crypto speculators sell shares to cover their crypto losses, but it looks marginal with Bitcoin having had a 50% fall since mid-April but shares remaining around record highs. What’s more most investors have a zero or negligible exposure to cryptos, any negative wealth effect will be swamped by ongoing stimulus and the banking system has little exposure to them.

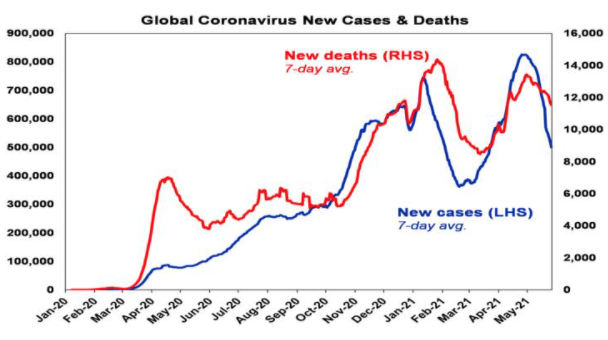

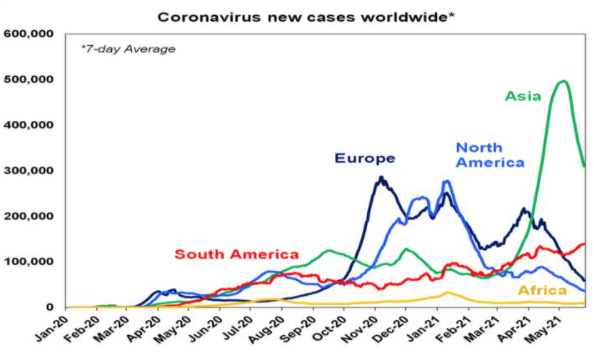

- Fortunately, the trend has remained down in new global coronavirus cases and deaths over the last week with developing countries falling sharply (including Japan slowing again) and India continuing to see a decline. But there is no room for complacency as this continues to mask various countries that are seeing renewed upswings including Brazil, South Africa, Malaysia, Vietnam and Taiwan.

Source: ourworldindata.org, AMP Capital

Source: ourworldindata.org, AMP Capital

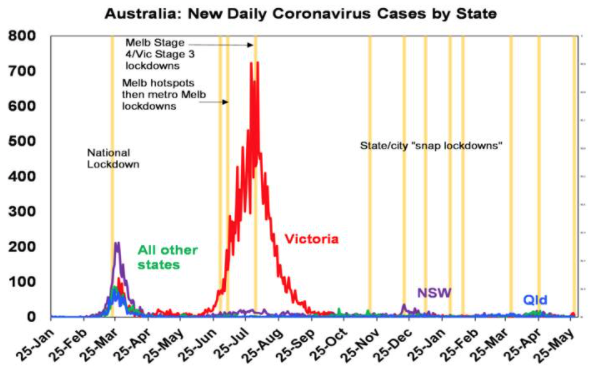

- And of while new cases remain very low in Australia, it is now seeing another worrying outbreak which in turn has led to another snap “circuit breaker” lockdown for the whole of Victoria. Australia has had several snap lockdowns over the last six months and the evidence strongly suggests that if applied early they head off a bigger problem and longer lockdown (in the absence of course of most being vaccinated). Providing they are short the economic impact is relatively “minor” (although still horrible for those directly impacted) as spending and economic activity is simply delayed but bounces back quickly once the lockdown ends. If so, we are looking at an economic cost from Victoria’s snap lockdown of around $1-2bn rather than the $15-20bn or more cost of last year’s July to October lockdown. The good news is that the lockdown has been announced relatively early in terms of the number of new cases at around 10 a day – as opposed to over 60 a day when the Melbourne hotspot lockdown started in July last year or the over 600 a day when the full Victoria lockdown started in August – and this adds to confidence that it will be a short lockdown. See the next chart. But the risk is a bit greater as we are now dealing with the more virulent Indian variant.

Source: covid19data.com.au

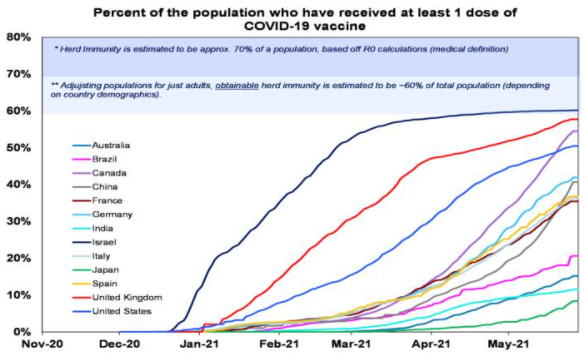

- Vaccine production is ramping up and there should be plentiful supply by early next year but so far only 11% of the global population has received at least one dose of vaccine. In emerging countries its 8% and its 38% in developed countries. Within developed countries the UK is at 58% which is nearing herd immunity allowing for only adults and those have already been exposed, the US is at 51%, Europe is at 36% and Australia is at 15%. As of 23 May, 8.9 million doses of vaccine had been supplied in Australia, but so far only 3.9 million doses have been administered. The success of the vaccines continues to be evident in Israel, the UK and the US which have seen a collapse in new cases, hospitalisations and deaths.

Source: ourworldindata.org, AMP Capital

- The renewed breakouts in Asia and now again in Victoria highlight the risk of reopening too quickly before herd immunity is reached particularly given the more virulent Indian variant and the lack of exposure in many of these countries to coronavirus. The experience of the last year highlights that in the short term the best way to deal with these outbreaks is via snap early lockdowns both in terms of avoiding deaths and making sure the health care system can cope (if Australia had seen the same number of deaths per capita as the US we would have lost 47,000 Australians as opposed to 910) but also in terms of averting a bigger hit to the economy (economies like Australia that kept covid cases down have seen better economic performance). Of course, the only way to end the cycle of snap lockdowns and fully reopen is to get vaccinated until herd immunity is reached – both in Australia and globally. At least Victoria’s plight (along with vaccine passports) may help knock the vaccine hesitant out of their complacency.

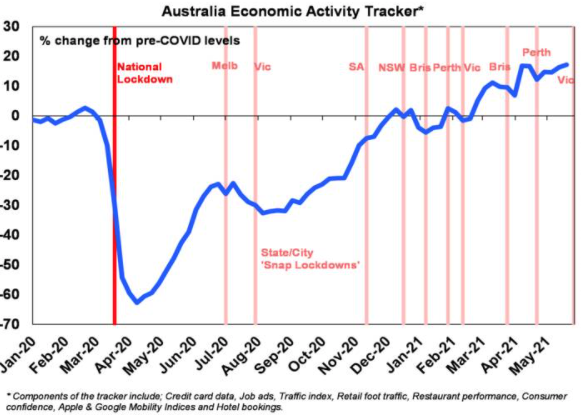

- Our Australian Economic Activity Tracker rose again over the last week and remains very strong indicating that recovery remains on track. However, it’s likely to see yet another dip in the next week or so reflecting Victoria’s snap lockdown just as various snap lockdowns in other states have caused dips over the last six months. See the next chart. If the lockdown is short its likely to see the rising trend in economic activity quickly resume again as seen after the various other snap lockdowns ended.

Source: AMP Capital

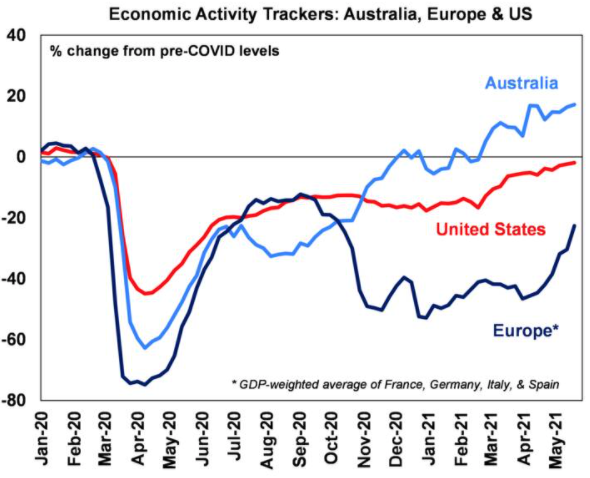

- Our US Economic Activity Tracker is almost back to its pre-coronavirus level, and the European Tracker is now rising rapidly as Europe reopens.

Based on weekly data for eg job ads, restaurant bookings, confidence, mobility, credit & debt card transactions, retail foot traffic, hotel bookings. Source: AMP Capital

Major global economic events and implications

- US data was a mixed bag – but still good. Durable goods orders continued to trend up in April, jobless claims continue to fall and home prices are continuing to rise, but home sales were weaker than expected and consumer confidence fell slightly in May and remains down from pre coronavirus levels. While consumers are seeing jobs as being plentiful their relative caution may suggest that they will take time to spend their stimulus windfall – which may be a good thing in terms of avoiding overheating.

- President Biden’s 8-year $2.25 trillion infrastructure plan (called the American Jobs Plan) remains on track one way or another. This can pass Congress either as a bi-partisan bill (requiring a 60% Senate majority) or a reconciliation bill (with a 51% vote) or some combination of the two. While the gap has narrowed between Democrats (who have compromised at $1.7 trillion) and Republicans (at $800bn or so) it’s still wide so reconciliation remains most likely. Even if there is a bi-partisan deal what does not make the cut there can still be passed via reconciliation to get the full $2.25 trillion. However, the total boost to the deficit is likely to be greater than originally indicated as the corporate tax rate is likely to only rise to 25% not 28% and any portion that gets passed through a bi-partisan bill won’t be funded as Republicans won’t vote for tax hikes.

- German, French and Italian business confidence indicators improved further in May.

- Japan’s jobs market softened slightly in April not helped by the latest covid State of Emergency and core inflation in Tokyo fell to -0.1%yoy in May.

Australian economic events and implications

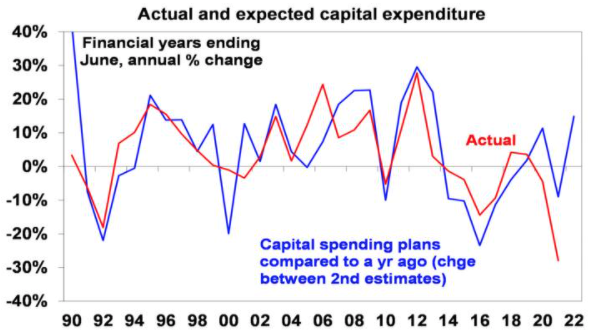

- Housing construction and business investment on the rise. Construction and capital expenditure data for the March quarter provided good news. Dwelling investment rose 5.1% quarter on quarter consistent with surging building approvals with likely more to come. Public construction rose 4.3%qoq and is likely to also remain strong given strong infrastructure investment. And private capital spending rose a stronger than expected 6.3%qoq driven in particular by a 9% rise in plant and equipment investment. What’s more business investment plans for the next financial year are up nearly 15% on plans for a year ago pointing to strong growth in business investment going forward which is consistent with high levels of business confidence, high corporate cash reserves and tax incentives. Adjusting business intentions for the past average gap between intentions and actual outcomes points to investment growth of around 20% in the next financial year with mining investment the strongest but manufacturing and other industries also strong.

Source: ABS, AMP Capital

- Payrolls down into early May but unlikely to be a sign that the ending of JobKeeper has caused a big loss of jobs: JobSeeker benefit recipients have continued to decline into May, suggesting little impact from the ending of JobKeeper; payrolls tend to get revised up after the initial read; and leading indicators of the jobs market such as job ads and vacancies remain strong.

What to watch over the next week?

- In the US, expect the manufacturing and services conditions ISM indexes (due Tuesday and Thursday) to remain strong in excess of 60 with price pressures remaining high and jobs data (Friday) is anticipated to show a 660,000 rise in payrolls and unemployment falling to 5.9%.

- Eurozone unemployment for April is expected to remain high at 8.1% with core CPI inflation for May remaining weak at 0.9%yoy (both due Tuesday).

- Japanese data is likely to show a fall in industrial production for April (Monday) and household spending data (Friday) is likely to soften.

- Chinese business conditions PMIs for May due early in the week will be watched closely given the mixed economic activity data seen in April.

- In Australia, the RBA is expected to leave monetary policy on hold following its meeting on Tuesday as it’s still a long way from meeting its requirements for a rate hike. While the jobs market has tightened more rapidly than expected, it’s still a long way from full employment let alone being strong enough generate wages growth “sustainably above 3%” which is necessary to be confident of sustainably achieving the 2 to 3% inflation target. While this may come in 2023 that’s still a long way off and the RBA is likely to reiterate that it does not expect to raise interest rates until 2024 at the earliest. Meanwhile, views are that with the economy recovering faster than expected the RBA will stick with the April 2024 bond as the target bond for the 3-year yield target and cut its bond purchases in half from September but its indicated that it won’t consider this until the July meeting.

- On the economic data front in Australia, the focus is likely to be on March quarter GDP data (Wednesday) which is expected to show a 1.1% gain driven by growth in services consumption, dwelling investment, business investment and public spending offsetting detractions from inventories and net exports. This will leave GDP up 0.3% on a year ago and see it back at its pre pandemic high. Meanwhile, expect credit data (Monday) to show a 0.4% rise in April driven by accelerating housing credit, net exports to show a -0.1 percentage point detraction from March quarter GDP growth, April building approvals to show a 10% pull back after a 17% HomeBuilder driven surge in March and May CoreLogic dwelling prices to show a 2.3% rise in average home prices driven particularly by a crazy 3% rise in Sydney (all due Tuesday), final retail sales data to confirm a 1.1% rise and the trade surplus to have remained strong (both Thursday) and housing finance to show a -4% decline (Friday) after another strong rise in March.

Outlook for investment markets

- Shares remain at risk of a short-term correction with possible triggers being the inflation scare, US taper talk and rising bond yields, coronavirus related setbacks, US tax hikes and geopolitical risks. But looking through the inevitable short-term noise, the combination of improving global growth and earnings helped by more stimulus, vaccines and still low interest rates augurs well for shares over the next 12 months.

- With the Australian share market at record highs and already nearly at the year-end ASX 200 target of 7200 it has been revised up to 7400 reflecting stronger than expected earnings growth, a faster than expected rebound in dividends and ongoing low interest rates keeping shares relatively attractive.

- Still ultra-low yields and a capital loss from rising bond yields are likely to result in negative returns from bonds over the next 12 months.

- Unlisted commercial property and infrastructure are ultimately likely to benefit from a resumption of the search for yield but the hit to space demand and hence rents from the virus will continue to weigh on near term returns.

- Australian home prices are on track to rise around 17% this year before slowing to around 5% next year, being boosted by ultra-low mortgage rates, economic recovery and FOMO, but expect a progressive slowing in the pace of gains as government home buyer incentives are cut back, fixed mortgage rates rise, macro prudential tightening kicks in and immigration remains down relative to normal.

- Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

- Although the $A is vulnerable to bouts of uncertainty and RBA bond buying will keep it lower than otherwise, a rising trend is likely to remain over the next 12 months helped by strong commodity prices and a cyclical decline in the US dollar, probably taking the $A up to around $US0.85 by year end.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer