Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 12th August 2022

Investment markets and key developments over the past week

- The share market rebound continued over the last week helped by weaker than expected US inflation data. Australian shares were little changed though with strong gains in resources largely offset by sharp falls in IT, health and property shares. Bond yields generally rose as the fall in yields in prior weeks had gone a little too far too fast. Oil prices rose partly due to US supply disruptions and increased demand forecasts on the back of higher gas prices. Metal and iron ore prices also rose. The $A rose as the $US fell.

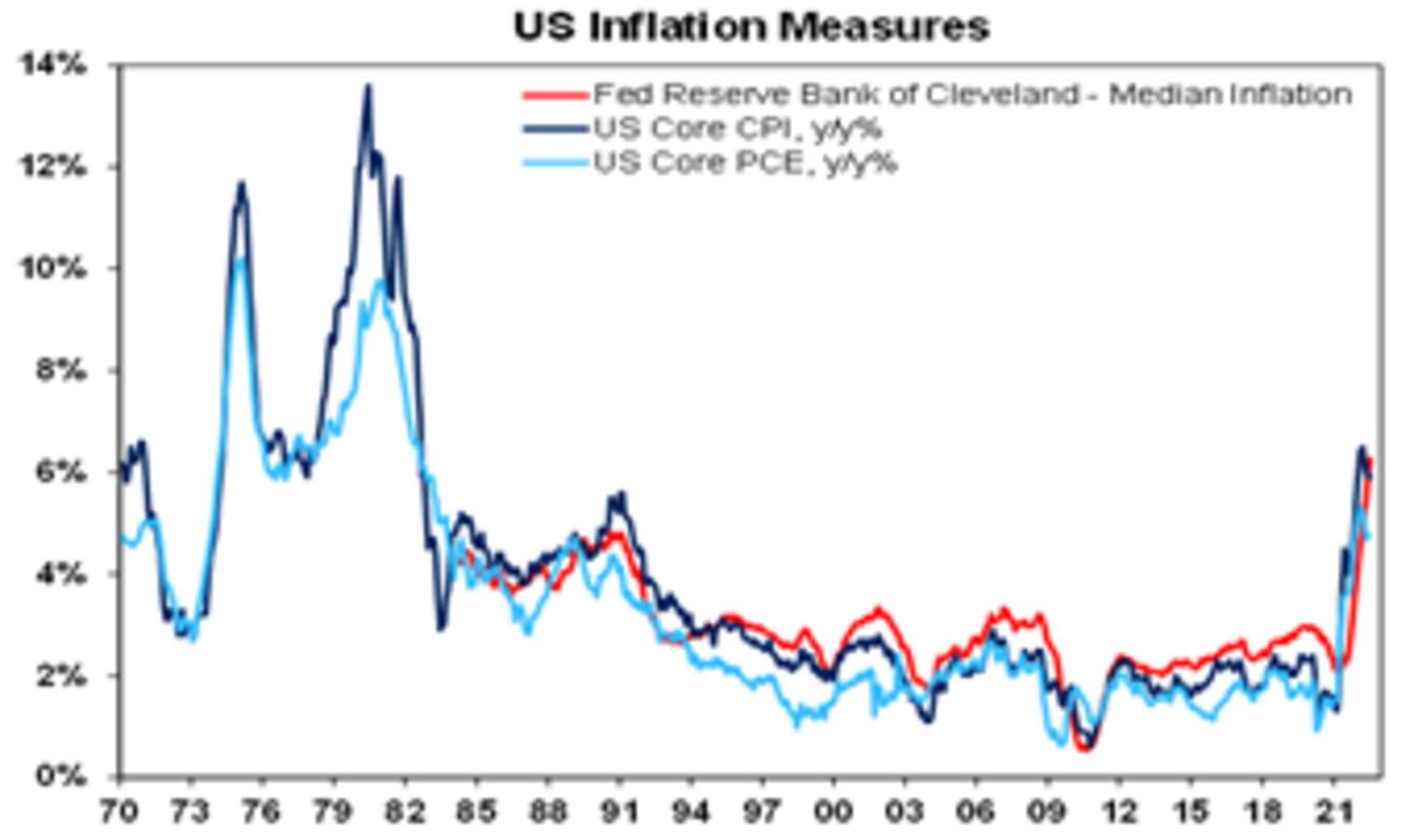

- More signs of “peak inflation” in the US. CPI inflation came in weaker than expected in July at 8.5%yoy (down from 9.1%) with core inflation remaining unchanged at 5.9%yoy and down from a peak of 6.5% in March. The decline in inflation came from lower gasoline prices (which has continued) and softness in prices for used vehicle, airfares and hotels. Producer prices also fell with annual PPI inflation continuing to trend down further adding to evidence of peak inflation.

Source: Bloomberg, AMP

- It’s premature to get too excited just yet. Goods price inflation has slowed and is likely to fall further – reflecting rising inventories, lower delivery times and falling freight rates – and energy inflation may also have peaked depending on the oil price. See the next chart. However, services inflation is still trending up reflecting rising labour costs (which are more sticky) and this is reflected in a still rising breadth of price rises with the median inflation rate rising to a new high of 6.3%yoy and the proportion of CPI components with price gains above 3%yoy rising to 89%. And of course, it will take a while to get inflation back to target. So more rate hikes from the Fed still lie ahead.

Source: Bloomberg, AMP

- However, while the Fed still has more work to do the increasing evidence of a peak in US inflation is good news:

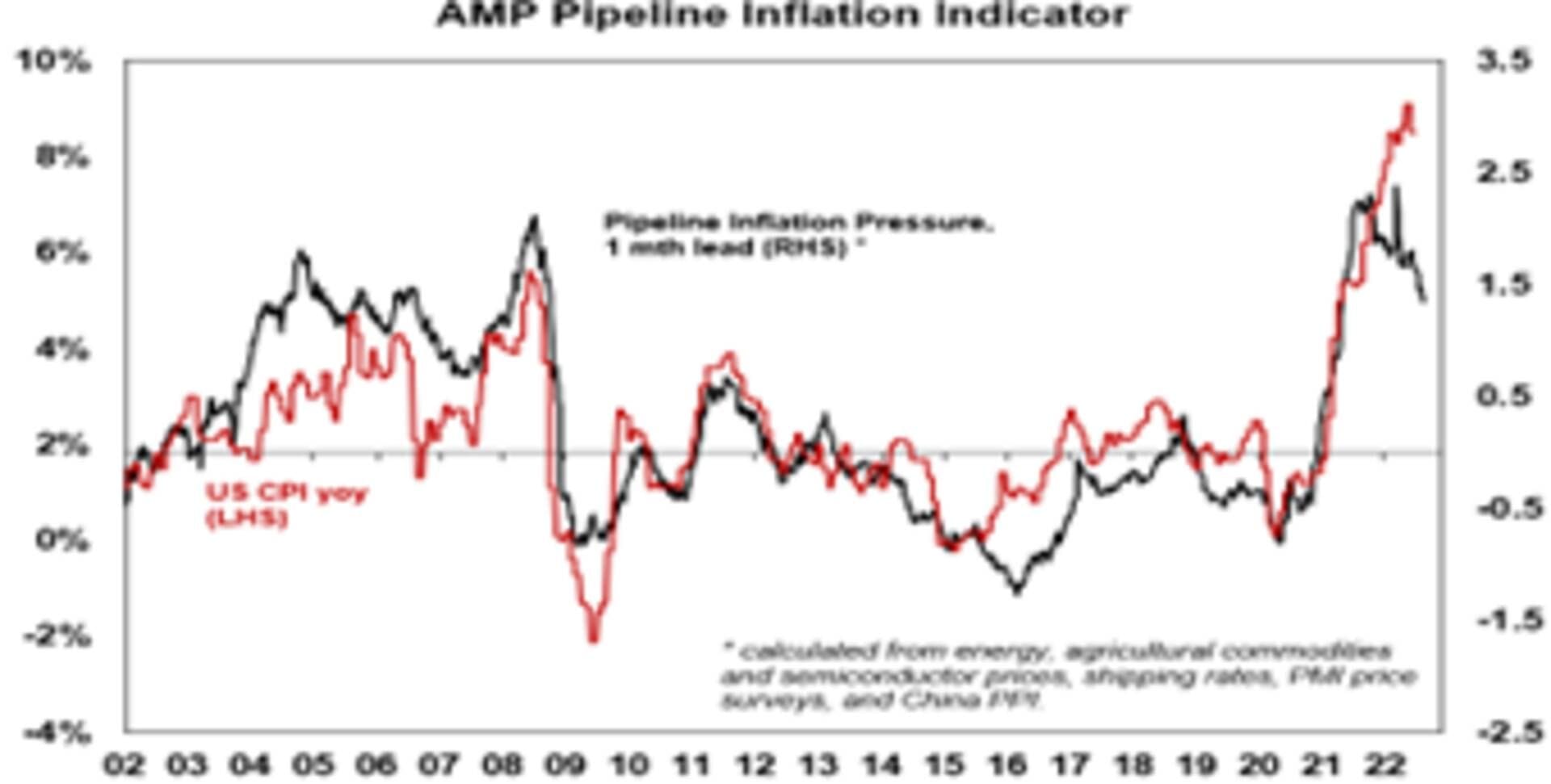

- First, its consistent with the Pipeline Inflation Indicator so it’s good to know that it has given the right signal. It’s still pointing to further falls in US inflation.

- Second, the better US inflation news along with ongoing signs inflation expectations are being contained will likely enable the Fed to go a bit easier in the months ahead – possibly hiking by 0.5% in September rather than by 0.75%.

- And third, the US led other countries including Australia in the inflation blowout so a cooling in the US is a positive sign for inflation in Australia too – with about a siX-month lag which would be consistent with a peak next quarter.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components. Source: Bloomberg, AMP

- Despite the better new on US inflation, still likely to see shares as vulnerable to a pull back over the next few months as: central banks are still a way off from peaking and actually cutting rates; recession risk is still rising (as evident in the inverting US yield curve); this runs the risk of significant earnings downgrades; and geopolitical risk is still on the rise with the escalation in China/US tensions over Taiwan and the upcoming US mid-terms. However, increasing signs of a peak in US inflation, 20% or so falls in share markets possibly having already anticipated a mild recession and the continuing strength of the rebound (with the direction setting US share market up 15% from its low) maintain the possibility that we may have seen the bear market low and any pull back may just be a partial retracement of the rally since mid-June. Time will tell. Either way, on a 12-month horizon remain optimistic on shares as inflation recedes, central banks become less hawkish and at least a deep recession is likely to be avoided.

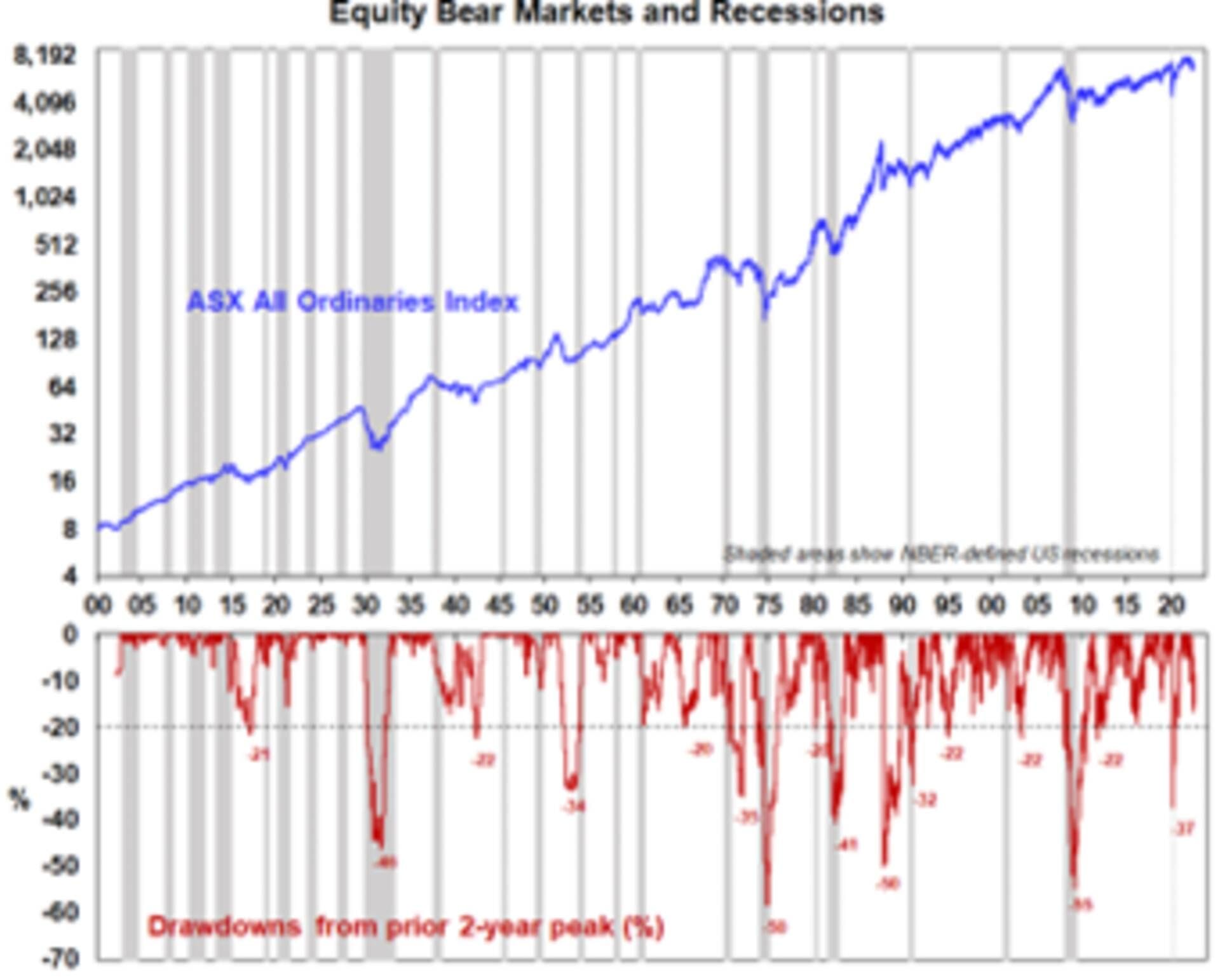

- The importance of whether the US has a recession to the depth of share market falls in Australia is indicated in the next chart. Severe share market set backs (or “grizzly bear markets”) tend to be associated with US recessions, particularly over the last 50 years with the exception of the 1987 crash.

Source: ASX, Bloomberg, AMP

- Australia is moving to a monthly CPI – but it’s doubtful this will lead to better policy making. The ABS has announced it will release an information paper on Tuesday and starting in October it will publish a monthly CPI along with the September quarterly CPI. While many are hailing the benefit of more timely inflation data, there are some who are sceptical of the benefits of this. Economists tend to assume that the more data the better, but there is no evidence that the absence of monthly inflation data compared to other countries has led to worse economic policy management and outcomes in Australia or that more frequent inflation data will improve inflation control. Monthly data can be very volatile – which is why the ABS at times has urged a focus on the trend rather than monthly moves. And so, it could risk more twitchy monetary policy from the RBA or more likely the RBA will wait a few months until a clear trend is evident anyway in which case we may as well have stuck to quarterly. It’s good for money market traders and commentators though as it will mean more to trade on and talk about!

Coronavirus update

- New global Covid cases were little changed over the last week – with Europe, the US and South America down but Asia up. New cases in China are up a bit but still low and the recent outbreak has been limited to some small provinces.

Source: ourworldindata.org, AMP

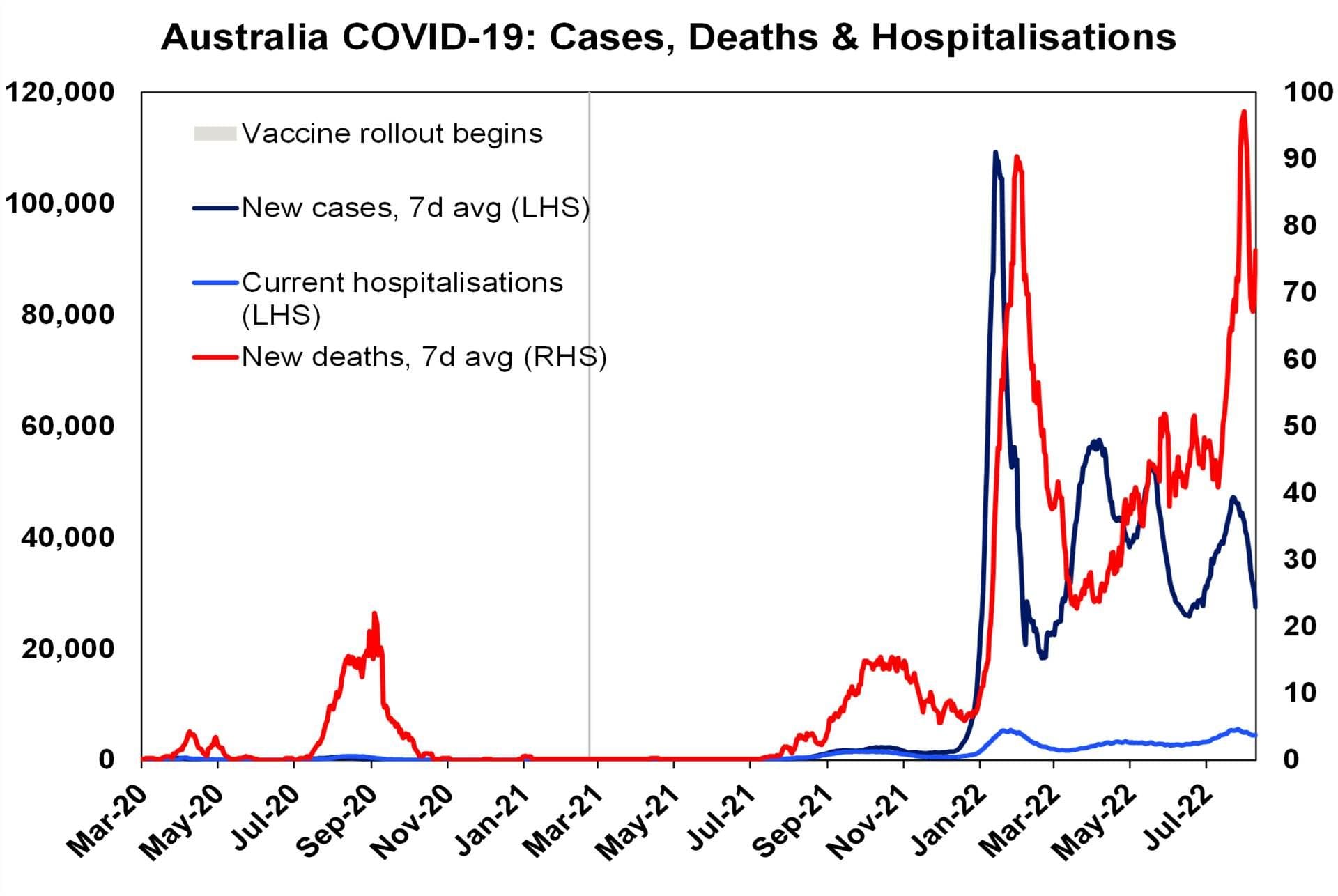

- In Australia, new covid cases are trending down, as are hospitalisations and positive testing rates in NSW and Victoria.

Source: ourworldindata.org, AMP

Economic activity trackers

- The Australian Economic Activity Tracker fell again over the last week and continues the loss of momentum seen since April consistent with a slowdown in growth. The US Tracker rose slightly and the European Tracker fell slightly.

Based on weekly data for e.g. job ads, restaurant bookings, confidence, mobility, credit & debit card transactions, retail foot traffic, hotel bookings. Source: AMP

Major global economic events and implications

- Apart from the inflation data it was a relatively quiet week for US data. June quarter data showed a fall in productivity and a sharp rise in unit labour costs suggesting ongoing upwards pressure on services inflation for now. Small business optimism rose slightly in the NFIB survey but like consumer confidence it remains depressed – in contrast to broader business measures (like PMIs) which are down but nowhere near as weak. The NFIB survey also showed a slowing in wages & price pressure.

Source: Bloomberg, AMP

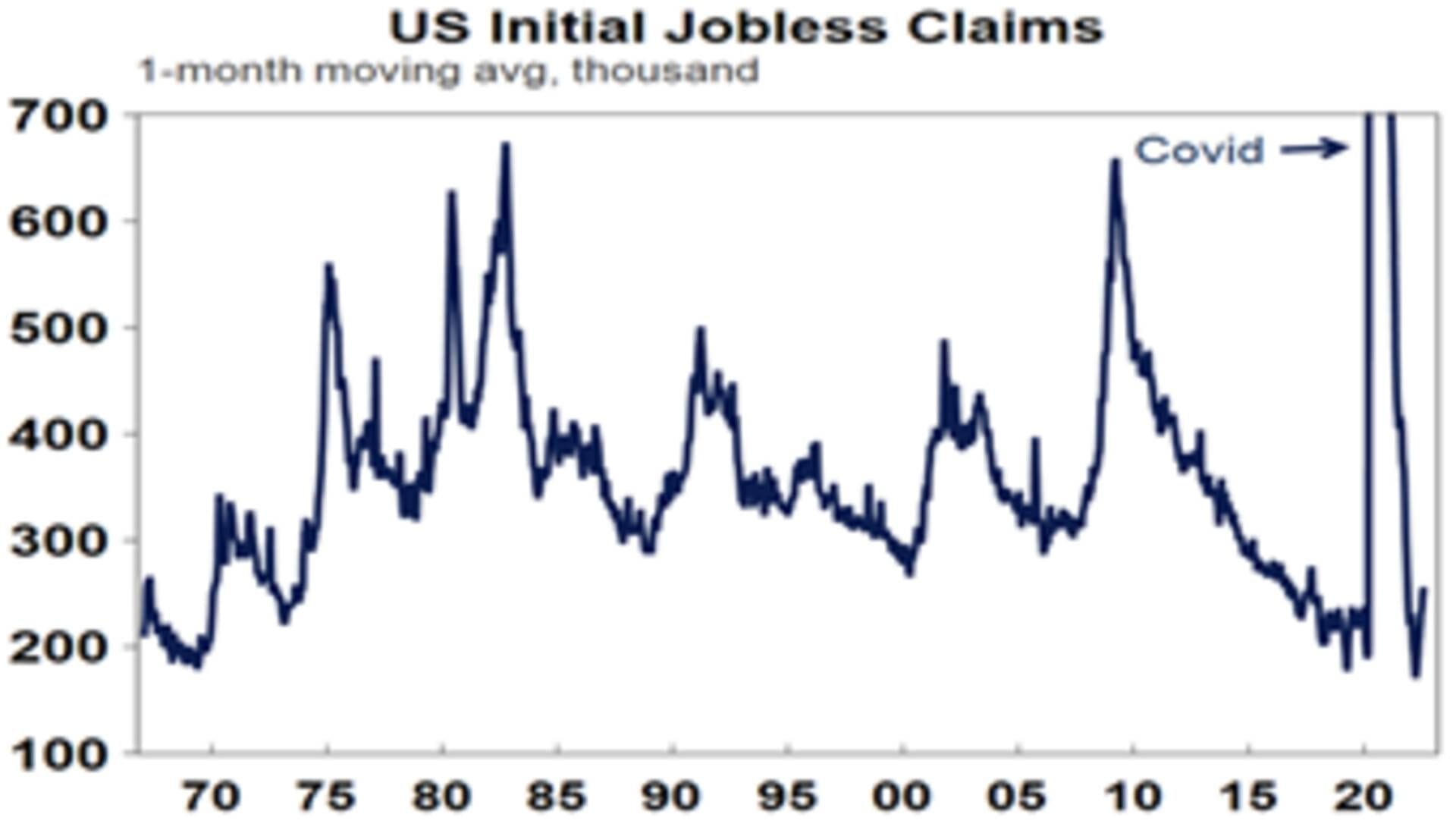

- Jobless claims rose again in the last week consistent with a cooling jobs market.

Source: Macrobond, AMP

- More than 91% of US S&P 500 companies have now reported June quarter earnings with 75% ahead of expectations and earnings growth expectations for the quarter rising from 5%yoy at the start of the reporting season to now 10%. This is far stronger than expected. Outlook comments have been mixed reflecting the uncertainty regarding the growth outlook but not overwhelmingly negative, although earnings expectations for the current half are being revised down.

- Japan’s Eco Watchers economic sentiment indicator fell back in July and producer price inflation slowed.

- Chinese export growth remained strong in July but import growth remained weak despite the reopening after the lockdowns earlier this year. Inflation remained soft with CPI inflation rising to 2.7%yoy, but core inflation fell to just 0.8%yoy and producer price inflation slowed further to 4.2%yoy. Inflation is no barrier to further policy stimulus in China.

Australian economic events and implications

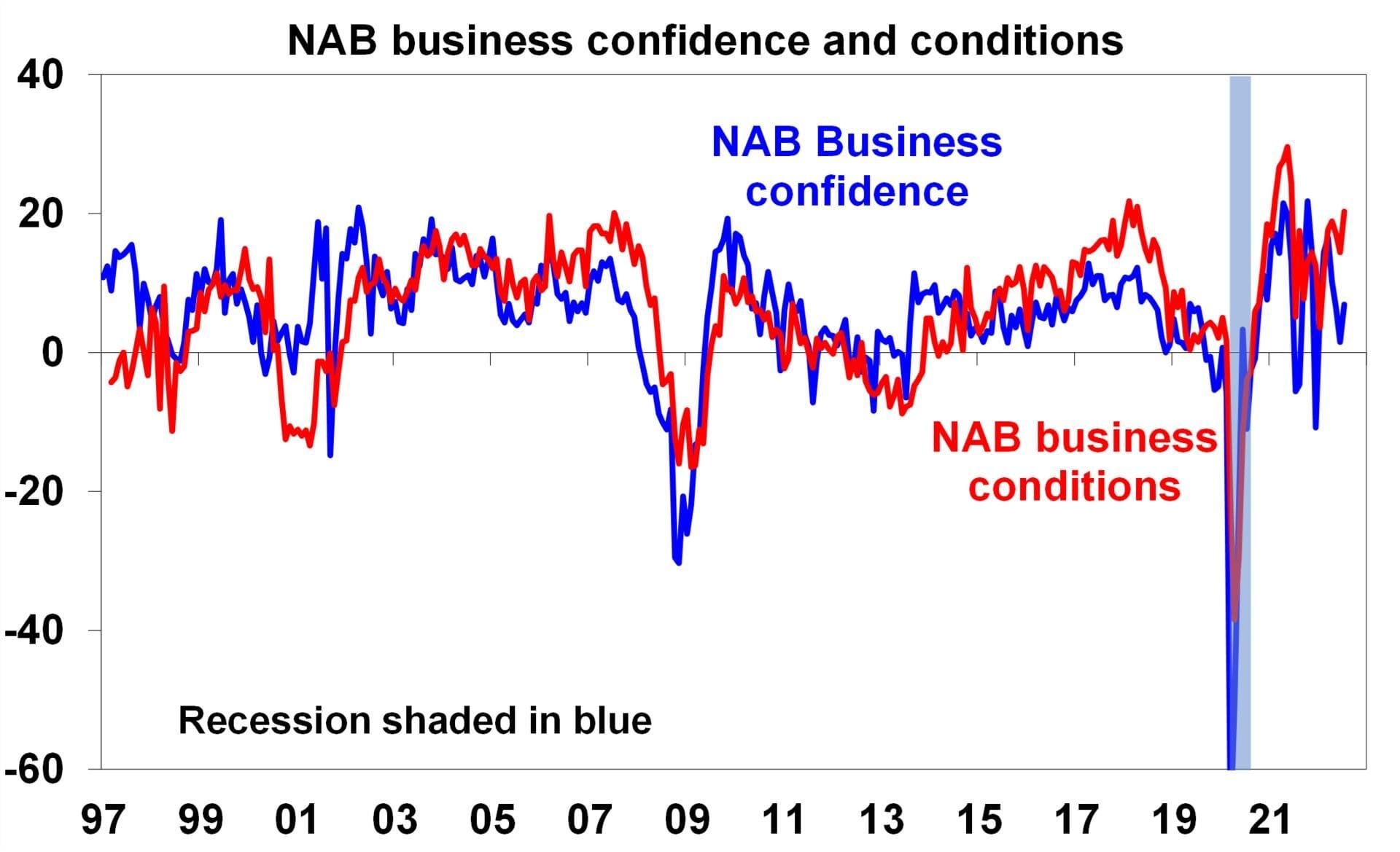

- Australia is continuing to show a confusing mix of strong coincident and lagging data but weakening leading data. In terms of the former the ABS’ household spending indicator (based on bank card data) showed continued strong growth of 10%yoy in June. Of course, this is being boosted by rapid inflation and the post reopening recovery in services (which are up 16%yoy) but it along with already released real retail sales data points to strong growth in consumer spending in the June quarter. The tight jobs market and excess household saving built up through the pandemic are clearly helping. This is also consistent with the NAB business survey which is continuing to report strong business conditions, still okay business confidence and capacity utilisation rising to a record high.

Source: NAB, AMP

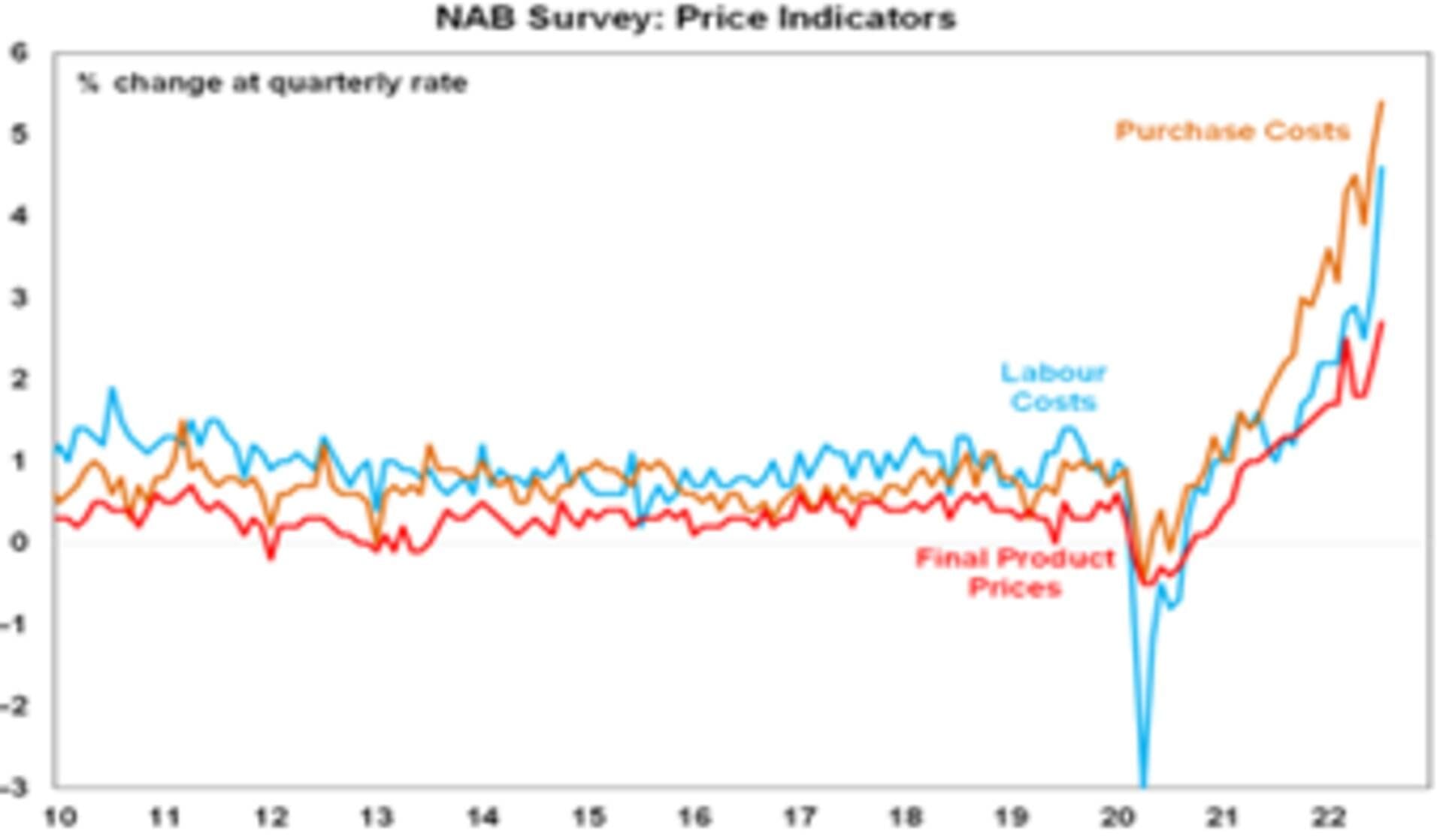

- Reflective of the economy being up against capacity constraints the NAB survey shows record high price and cost pressures. All of which is consistent with the RBA continuing with rate hikes for now and now expected is another 0.5% hike in September (but still see the cash rate peak as being around 2.6%).

Source: NAB, AMP

- Against this though, leading indicators like consumer confidence are continuing to weaken. The Westpac/MI measure of consumer confidence fell another 3% in August and is down around levels associated with recession as cost of living pressures and higher rates impact. This is warning of much slower growth in demand ahead, which will ultimately ease capacity pressures and inflation. But of course, it runs the risk of an excessive growth slowdown or recession.

Source: Westpac/MI, NAB, AMP

- In another sign that rate hikes are impacting, new home sales fell 13% in July according to the HIA as builders report less enquiries and visits to display sites.

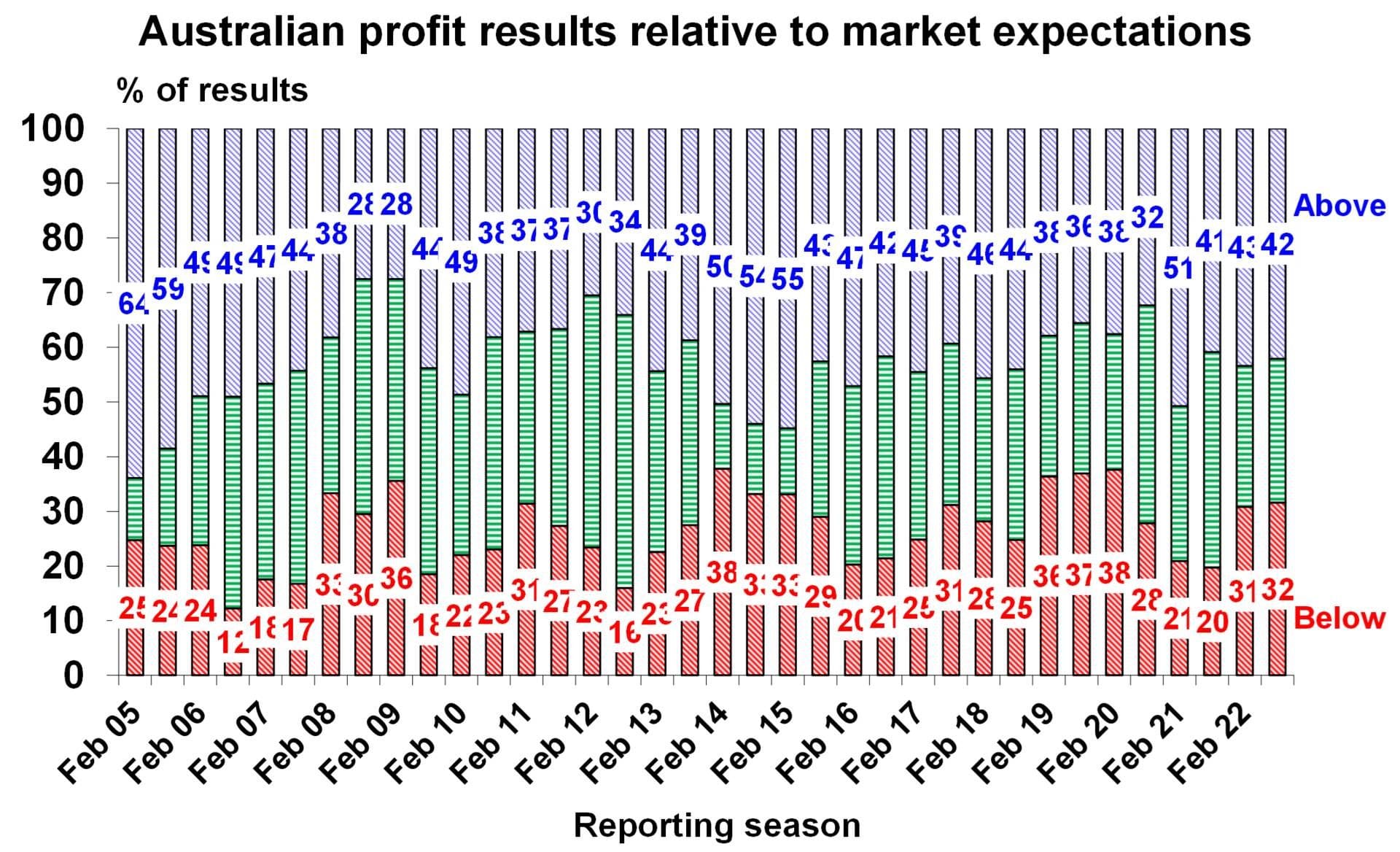

- The Australian June half earnings reporting season has picked up pace and so far results have generally been strong reflecting the strong economic conditions of the last financial year. It’s early days yet as only about 30 major companies representing just less than 30% of market capitalisation have reported so far and there is a tendency for good news results to come out early in the reporting period. So far 42% of results have surprised on the upside which is about average, but only 56% have seen earnings up on a year ago & 44% have increased dividends both of which are well below average reflecting the cost pressures some business are facing.

Source: AMP

What to watch over the next week?

- In the US, expect further falls in home builder conditions (Monday) and housing starts (Tuesday), modest gains industrial production (also Tuesday) and retail sales (Wednesday) and soft readings from the New York and Philadelphia regional manufacturing surveys. The minutes from the Fed’s last meeting (Wednesday) are expected to remain hawkish, but allowing for some possibility of a slowing in the pace of rate hikes.

- UK July inflation data (Wednesday) is likely to rise to 9.9%yoy.

- The Reserve Bank of NZ (Wednesday) is expected to hike it’s cash rate by another 0.5% taking it to 3%.

- Japanese June quarter GDP (Monday) is expected to show 0.7%qoq growth reflecting a rebound from Covid restrictions earlier this year. Inflation data for July (Friday) is expected to show a further slight lift in CPI inflation to 2.6%yoy, but core inflation remaining weak at just 1.1%yoy.

- Chinese economic activity for July (Monday) is expected to show further improvement following the reopening from Covid lockdowns with industrial production growth rising to 4.5%yoy and retail sales growth rising to 5%yoy.

- Australian June quarter wages growth (Wednesday) is expected to show a further modest lift to 0.8%qoq or 2.7%yoy and July jobs data (Thursday) is expected to have remained strong with another 25,000 new jobs leaving the unemployment rate at 3.5%.

- The June half Australian earnings reporting season will speed up with around 60 major companies due to report covering around 35% of market cap including BlueScope and JB HiFi (Monday), BHP and Seven West (Tuesday), Amcor, Dexus, Domain and Santos (Wednesday), ASX, Origin and Transurban (Thursday) and Cochlear and Stockland (Friday). Consensus expectations are for around 20% earnings growth for the 2021-22 financial year but with this boosted by energy earnings (+275%) and industrials averaging around 9.5% growth. The focus will likely be on outlook statements given cost pressures, labour shortages and slowing consumer demand.

Outlook for investment markets

- Shares remain at high risk of a pull back in the months ahead as central banks continue to tighten to combat high inflation, the war in Ukraine continues and uncertainty about recession remains high. However, expect to see shares providing reasonable returns on a 12-month horizon as valuations have improved, global growth ultimately picks up again and inflationary pressures ease through next year allowing central banks to ease up on the monetary policy brakes.

- With bond yields looking like they have peaked for now short-term bond returns should improve a bit further.

- Unlisted commercial property may see some weakness in retail and office returns (as online retail activity remains well above pre-covid levels and office occupancy remains well below). Unlisted infrastructure is expected to see solid returns.

- Australian home prices are expected to fall 15 to 20% into the second half of next year as poor affordability and rising mortgage rates impact.

- Cash and bank deposit returns remain low but are improving as RBA cash rate increases flow through.

- The $A is likely to remain volatile in the short-term as global uncertainties persist. However, a rising trend in the $A is likely over the medium-term as commodity prices ultimately remain in a super cycle bull market.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer