Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

A FinSec View – Future insights into the global economy, FAANG & Fed’s excellent adventure, DINs and more…

|

Issue: 26th November 2021 |

| This week President Joe Biden declared that he would re-nominate Jerome Powell as chairman of the US Federal Reserve (his current term expires in February). After what has been quite a drawn-out selection process, it is indeed encouraging that Mr Biden has, at last, made the obvious choice, opting for a ‘steady pair of hands’.

Many investors have been hoping for this outcome – Given the delicate task ahead for the Fed, an experienced voice is preferred (over his term, the Fed and many central banks globally appeared to take on a much greater mandate for ensuring market stability). The challenge from here will be, how Powell starts to ‘wean the patient from the drugs’. Plotting a path back to normalised monetary policy settings, while minimising market fallout will not be easy. In equity markets, the US and Australia have continued their climb. As of last night with three trading days remaining for November, the S&P 500 was up 2.3% and the All ords up 1.6%. However, given today’s news regarding a new variant out of South Africa, we gave it all back – highlighting that we are in for an increasingly bumpy ride. Rising Covid case numbers across Europe and the reintroduction of lockdowns in some areas has been a reason for concern. The release of US CPI numbers (mid-month) with a rise of 6.2% the largest increase in 30 years didn’t do anything to help. However, the Jerome Powell announcement (mentioned above) along with better than expected US consumer spending, and the RBAs re-enforcement that there will not be any rate hikes in 2022 has helped to balance things out. We hope you enjoy this week’s View – We make special mention of the ‘housekeeping’ section containing important information with regard to Director Identification Numbers and a further scam alert. |

|

| Fund manager PIMCO recently held their annual Secular forum. At the summit, investment professionals, along with Global Advisory Board member and former Federal Reserve Chairman Dr Ben Bernanke, offered their insights into the key forces affecting the global economy over the next five years.

The below looks at four takeaways from the wide-ranging discussion:

|

|

| Our understanding of how investing works seems to be challenged on a near-daily basis.

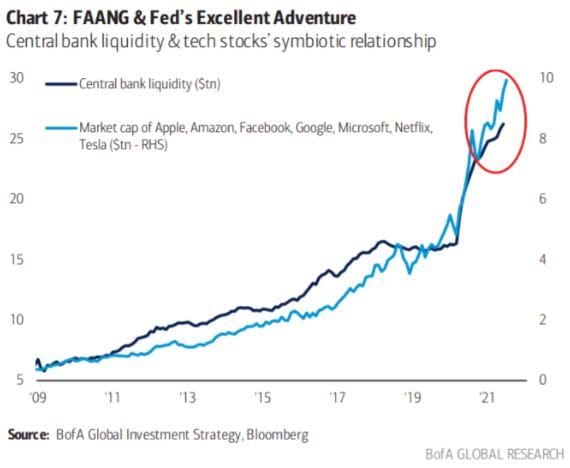

A Bitcoin is worth around US$60,000, but only 10 years ago, it sold for less than US$1. NTFs (non-fungible tokens) are a thing where effectively clip-art and tweets are selling for the same price as houses… The recent IPO of Rivian was another startling example of market mania, a company that has manufactured less than 200 cars with revenue forecasted between zero and US$1 million and costs of around US$1 billion for the September quarter. Yet, as mentioned in a previous View it is worth roughly the same as Honda, Hyundai, and BMW combined (we note that Rivian does seem to be appealing to commercial clients, including its own influential backers. After participating in two funding rounds for the start-up, Amazon last year committed to buying 100,000 electric delivery vehicles from the manufacturer by 2030). And, of course, then there is Tesla, the poster child of all asset bubbles – by all accounts, a good company that just doesn’t make much money. It would seem the market’s enthusiasm for technology is boundless (particularly if it promises to help fix climate change…). No revenues pfft, who cares when you have central banks to provide whatever liquidity is needed, including the longer-term valuations of these tech stocks. It doesn’t hurt to participate as long as you are happy to take your profits on the way out. Aptly named ‘FAANG & Fed’s Excellent Adventure’, the symbiotic relationship between central banks and tech stocks makes for our chart of the week.

|

|

| Director Identification Numbers (DIN)

If you are a director of an Australian company, new personal identification rules have been introduced requiring you to obtain your own personal Director Identification Number (Director ID). In short, if you are the corporate trustee of a Self Managed Super Fund (SMSF), family trust or a company director:

We are currently working with our third-party partners to ensure the appropriate action is taken by all those clients impacted. For further details on these new rules, including a guide to the application process, please click here.

Scam Week Scam week was held this month, a timely reminder to stay smart online. And, don’t think it can’t happen to you. Only this week, we had a client exposed to an elaborate con (luckily, in this case, no funds were lost) – the scammers seemed authentic and knew their way around financial institutions – Scary! Rest assured the matter has been handed over to the police. As these people become increasingly sophisticated, it is important to keep informed with regard to how scams work and how you can identify and protect your personal and financial information. Top tips to avoid being scammed:

If you think you’ve been scammed, contact your bank or financial institution immediately. You can also report a scam to Scamwatch.

|

|

| The concept of retirement, a brief period of leisure following four decades of hard work, is an outdated one. First introduced by German Chancellor Bismarck in the late 19th century and very much a product of the Industrial Age, retirement has now run its course.

It’s time to call time on this outdated notion – retirement has retired! There is no doubt that retirement is an exciting notion. In fact, it is probably a moment you’ve dreamt of for over a decade – endless days spent on the golf course, playing with smiling grandchildren and leisurely walks on the beach. Finally, your very own Utopian idyll. But what if it isn’t? What if those things you have looked forward to all these years are not enough to sustain you, to fulfil you and to energise you? Perhaps the good bishop was right? ‘Leisure is a beautiful garment for a day, but it will not do for constant wear’. Today work serves as more than just a source of income. It is a social life, a sense of utility and purpose. It provides dignity and pride, and self-esteem within a community. Prospective retirees list financial worries as their biggest concern. Actual retirees, however, rate sense of purpose as their biggest disappointment (being cut off from former colleagues, missing their jobs, and feeling behind the times). How will you replace all this? With time fast becoming that most precious of commodities, ‘am I living the life I want to live?’ becomes the most profound question of all. The following rules are the cumulative knowledge of over three decades of advising retiring Australians on the pursuit of life, liberty and happiness after full-time work. Regardless of where you might be in your retirement journey, we hope you find something here of value.

In a paper entitled ‘if money doesn’t make you happy, then you probably aren’t spending it right’ a Professor Gilbert recommends the following principles;

|

|

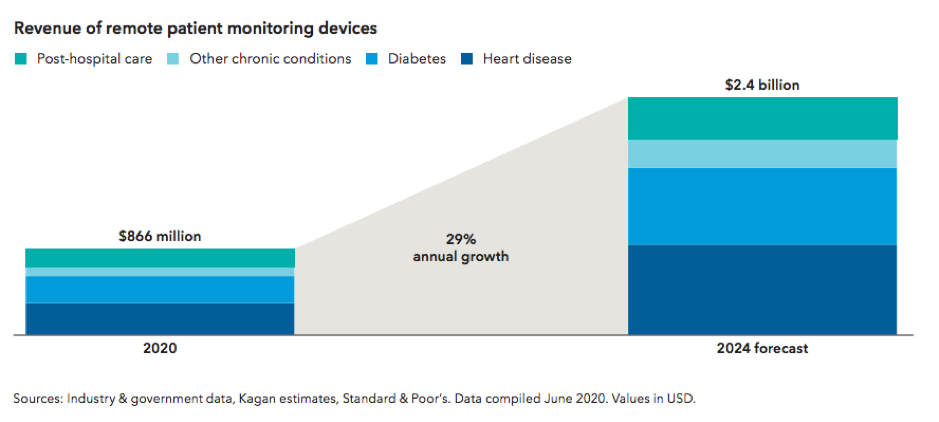

| Part 5 of our Capital Group series, ‘a guide to the world in 2030’ centres around health care innovation.

According to equity portfolio manager, Rich Wolf Star Trek depicted a far-off future where space explorers travelled the galaxies equipped with cutting edge technology such as the tricorder, a hand-held medical device that scanned a person’s vital signs, issued a diagnosis and prescribed treatment in minutes. While I don’t think we’ll have tricorders, I suspect that by 2030 many of us will have devices that will analyse blood, do cardiology monitoring and even remotely check our breathing while we sleep, some of which are already available. We are already experiencing a massive wave of innovation across the health care sector that will drive new opportunity for companies, potentially reduce overall costs and, most importantly, improve outcomes for patients. Breakthroughs in diagnostics may lead to earlier detection of illnesses, or in some cases treat disease before it progresses. Genetic testing equipment maker Illumina and research and manufacturing company Thermo Fisher Scientific are providing services to a host of drug developers. One of the most exciting things is the liquid biopsy, whereby a sample of your blood can be used to identify cancer at its earliest stages. Much of the recent focus has been on the pandemic and vaccine development. These are very important, but we have also been looking over the horizon, trying to determine how health care will transform itself and how we can invest in those shifts.

Whilst Wolf’s predictions for 2030 look past a COVID world we can’t but help take a moment to reflect on what the pandemic has meant for healthcare innovation – Life and business will never be the same for this sector; everything from how patients see their doctors and get treated to how hospitals use tools and share information is forever altered. The value of healthcare infrastructure Approximately 18 months ago, healthcare systems around the world were overwhelmed by an unknown virus and without the resources to deal with it. Communities confronted a variety of unprecedented shortages: Healthcare workers across the country and globe were scrambling for Personal Protective Equipment (PPE); hospitals were running out of supplies, beds and the human resources to treat Covid infected patients; medication supplies were dwindling and in some countries, crematoriums were being overrun. Similarly, 12 months later, as vaccines are being fast-tracked, distribution to communities became the new challenge. Many countries were forced to harness military resources for distribution, enable new digital platforms to track vaccine roll-out and contact tracing, and policy experts to coordinate between local and federal jurisdictions. The healthcare industry continues to fight the COVID-19 pandemic with innovation and grit. Many organisations pivoted to allow nonessential workers to work remotely. They erected field hospitals in parking lots and converted nonclinical spaces into auxiliary ICUs. Physicians turned to virtual visits to continue providing care (telehealth platforms). They sought out alternative suppliers for essential PPE. In a turbulent environment, a host of ingenious solutions surfaced to help bolster the healthcare system itself. We now live in a world where providing tools patients need to understand and manage their own health and sharing data with trusted partners and expanding access to care is the norm. From digital vaccine passports, to contact tracing, and now, more recently, harnessing big data to navigate the vaccine distribution process, the pandemic has reiterated how critical the role of technology is in healthcare. The silver lining here (if there is such a thing) is the innovation COVID has spawned: what was learned, how it was implemented, and now, how it can be sustained going forward. |

|

Stay safe and look after one another. As always, if you have any concerns or questions at any time, please reach out to your FinSec adviser. |

|

|

| We have enjoyed receiving much positive feedback in relation to this publication. Many have asked if they can share with family and friends and we would be delighted if you did! To ensure the integrity of the links please forward via the ‘send to a friend’ link at the very bottom of this email. |