Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 25th August

Investment markets and key developments over the past week

- Share markets were mixed over the last week with good global data but ongoing concerns about US politics, currency gyrations and mixed earnings results in Australia. Chinese shares rose 1.9% and US shares rose 0.7% on the back of positive indications regarding tax reform, but Eurozone shares fell 0.2% as the Euro rose further, Japanese shares fell 0.1% and Australian shares fell 0.1%. Bond yields were mostly down slightly, commodity prices were mixed with oil down but iron ore and metals up and the A$ slipped was flat despite a fall in the US$.

- Speeches by key central bankers at the Fed’s Jackson Hole symposium saw the Euro spike higher, but the overall message remains that global monetary policy will be easy for some time to come. Fed Chair Yellen provided a strong defence of post GFC financial regulations but had very little to say about the economy or monetary policy apart from reiterating that substantial progress has been made towards achieving the Fed’s economic objectives. ECB President Draghi was actually a bit dovish repeating that a significant degree of monetary accommodation is still required given ongoing low inflation and labour market slack with the key message that it will go very slowly in reducing stimulus. However, because Yellen was not hawkish as some had expected and Draghi did not attempt to jawbone the Euro lower, the foreign exchange markets interpreted it all as a green light to push the Euro even higher. But this is probably an overreaction: the Fed is still tightening and remains on track to announce quantitative tightening (ie, unwinding QE) next month and the ECB is still easing and will likely continue quantitative easing through next year albeit at a slower pace. So it is likely that the US$ will eventually turn back up again. Currency gyrations aside perhaps the main message from Jackson Hole is that global monetary policy will remain easy for some time to come in the face of ongoing low global inflation: the Fed is likely to remain gradual in undertaking monetary tightening; ECB is still dovish and doing quantitative easing; and the Bank of Japan’s Kuroda signalled “extremely accommodative monetary policy” for “some time”.

- Trump continuing to throw curve balls, adding to the risk but maybe not as bad as it looks. From North Korea, to Charlottesville, to a revolving door team in the White House and now the approaching budget/debt ceiling negotiations, the political mayhem in the US continues with President Trump at the centre of it. His comments to a rally of his supporters that he might terminate NAFTA and use the threat of a government shutdown to get funding for his wall have naturally kept investor nervousness alive around US policy and particularly the issue of a debt default if Congress and the President fail to agree a bill to increase the debt ceiling by late September/mid-October. This is because funding to avoid a shutdown may be paired with a bill to increase the debt limit by late September. US Government funding will run out on September 30 and the debt ceiling will be reached sometime between then and mid-October. As we saw in the last US Government shutdown between October 1-16 in 2013 the economic impact was minor, so another short shutdown would not be a major problem but a failure to raise the debt ceiling in time would be: although the US Treasury would avoid defaulting on its debt initially it would be forced to stop making some entitlement payments and this may trigger a broader downgrade to America’s credit rating which as we saw in 2011 caused a mini financial panic. However, there are several points to note in relation to this:

- President Trump should be taken seriously but not literally. He can go from Trump the populist rabblerouser to Trump the pragmatic businessperson within the same day to the point he looks schizophrenic so there is a danger in reading too much into what he says.

- Related to this his comments on shutting down the government and building the wall naturally appeal to his base but so did his comments about declaring China a currency manipulator and imposing 35% tariffs on Chinese imports and they haven’t happened. His comments on both NAFTA and the shutdown are likely both just part of a negotiating ploy.

- Congressional Republicans (and Democrats) are well aware of the blame they will take if welfare payments are stopped. The American public tended to blame Congressional Republicans for the 2013 shutdown and debt ceiling delay and they would probably do the same again which would not be good ahead of the 2018 mid-term Congressional elections.

- Consistent with this House Speaker Ryan has indicated that they are not interested in a shutdown, the chair of the conservative tea party group in the House has said “we will raise the debt ceiling and there shouldn’t be any fear of that” and Senate Majority Leader McConnell has said earlier this week that there is “zero chance, no chance, we won’t raise the debt ceiling.”

- With the departure of political adviser Stephen Bannon the populist influence around Trump in the White House has been dramatically reduced (almost wiped out).

- Finally, indications in the last week are that the White House and congressional leaders are making good progress on tax reform. The desire to achieve something by the 2018 mid-terms is a big driving force behind congressional Republicans’ in terms of tax reform.

- As a result, views remain that the debt ceiling will be raised in time and some form of tax reform will take place. However, unlike in the 2011 and 2013 debt ceiling debates the President is no longer calm and cool and has become a third force in the negotiations. So the risk is high that there will be lots of market disturbing argy bargy and last minute brinkmanship ahead of signing a new funding resolution and an increase in the debt ceiling. The worst case could be a two-week shutdown from October 1 which focuses public pressure ahead of a debt ceiling increase just before the ceiling is reached. Just like in 2013.

- Political uncertainty ramped up a notch in Australia with the High Court unlikely to rule on the citizenship issue of five (soon to be at least seven) Federal parliamentarians until October/November with a significant risk to the Government’s ability to govern and the risk of an early election if the Court takes a literal view of the Constitution. The prospect of six prime ministerships in just over 10 years is not a good look. The risk of an early election has yet to impact Australian financial markets. But it would likely weigh on business confidence which has been surprisingly upbeat since the 2013 change of government to the Coalition which in turn could adversely affect employment and investment. A change of government would also have significant implications for banks (with the Labor Party committed to a bank royal commission) and property prices (with the ALP committed to restricting negative gearing and cutting the capital gains tax discount).

Major global economic events and implications

- US data remains solid with the composite business conditions PMI rising solidly in August to a strong reading of 56 driven by strength in the services sector. Underlying capital goods orders and shipments are strong, jobless claims remain low and home prices are continuing to rise. Home sales fell in July though.

- The Eurozone composite business conditions PMI also rose in August to a strong reading of 55.8 driven by manufacturing. Consistent with this the German IFO and French Insee business conditions/confidence readings were strong. Consumer confidence is about as strong as it ever gets.

- Japan’s manufacturing conditions PMI rose in August to a solid reading of 52.8. Core inflation remained around zero in July though highlighting that it will be a long time before the Bank of Japan can consider an exit from ultra easy money policy.

Australian economic events and implications

- Australian data was light on but skilled vacancies rose in July indicating that the jobs market remains solid.

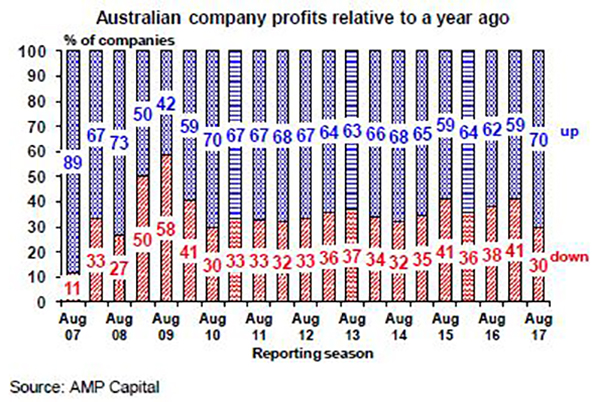

- We are now about 85% through the Australian June half earnings reporting season and results have remained a little disappointing. At a high level profits look good: they are up with 70% of companies reporting higher profits than a year ago (see the first chart below) which is the strongest since 2010, 69% have increased dividends from a year ago which is a good sign regarding the quality of earnings and overall earnings per share growth for 2016-17 is coming in at around 17.5% which is a huge improvement after two years of declines. However, dig beneath the surface and it’s not quite so good. First, the huge upswing in earnings owes to the rebound in the fortunes of the big resources stocks with resource sector profits up around 130% and there is no doubt that the turnaround here is impressive and reflecting this they have increased their dividends substantially. However, profit growth in the rest of the market is more modest at around 5-6%. What’s more only 38% of companies have surprised on the upside (which is less than normal and the weakest since 2012) and 32% have surprised on the downside. Outlook guidance has also been a bit soft. While the market as a whole has been relatively stable through the reporting season it’s basically flat for August to date – and a roughly equal number of companies have seen their share prices outperform and underperform the market on the day they released results, beneath the surface there has been intense volatility with some very sharp declines in share prices for companies who disappointed (eg Domino’s, Telstra, Suncorp, QBE, Bluescope and Healthscope) either in terms of the result, outlook comments or dividends. The problem of course is that PEs are relatively high and so much has been factored in. As a result, expectations for earnings growth for the current financial year have been revised down a bit to 1.8%, although again it’s worth noting that profit growth for the market excluding resources is expected to remain relatively stable at around 5%. Key themes have been: large caps doing better than small caps; resources stocks back to strength; constrained revenue growth with the domestic economy just okay with housing still strong but retailing mixed; some disappointment from foreign earners; and dividends (ex Telstra) continuing to roar ahead.

- While profit growth for Australian listed companies ex the miners at around 5% is all right it’s well below that in the US (at around 11%) and Europe and Japan (at around 30% lately) so it’s another reason to maintain a bias towards global shares over Australian shares.

Outlook for markets

- Share markets are at risk of a correction with signs of short term investor complacency and diminishing breadth in the US share market and various potential triggers including risks around North Korea, US politics and the Fed. However, with valuations remaining okay particularly outside of the US, global monetary conditions remaining easy and profits improving on the back of stronger global growth, a pullback would be seen as just a correction with the broad rising trend in share markets likely to resume through the December quarter and into 2018.

- Low yields point to ongoing low returns from bonds.

- Unlisted commercial property and infrastructure are likely to continue benefitting from the ongoing search for yield, but this will wane eventually as bond yields trend higher.

- National residential property price gains are expected to slow, as the heat comes out of Sydney and Melbourne.

- Cash and bank deposits are likely to continue to provide poor returns, with term deposit rates running around 2.5%.

- While further short term upside in the A$ is possible, views remain that the downtrend from 2011 will ultimately resume as the interest rate differential in favour of Australia is likely to continue to narrow as the Fed hikes rates and the RBA holds.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer