Disclaimer

Information provided on this website is general in nature and does not constitute financial advice. Every effort has been made to ensure that the information provided is accurate. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult a financial adviser to take into account your particular investment objectives, financial situation and individual needs.

Weekly Market Update – 1st February 2019

Investment markets and key developments over the past week

- Share markets were mixed over the last week. US shares rose 1.6%, helped by a more dovish and supportive Fed and mostly good economic and earnings news, Chinese shares gained 2% helped by continuing progress in US/China trade talks and Japanese shares rose 0.1%, but Eurozone shares fell 0.1% and Australian shares fell 0.7%. Bond yields mostly declined, helped along by a dovish Fed. Commodity prices rose with the iron ore price getting a big boost as Vale announced production cuts as a result of its dam disaster amounting to around 2-3% of global iron ore production. The US dollar fell on the back of Fed dovishness and this along with a surge in the iron ore price saw the $A rise.

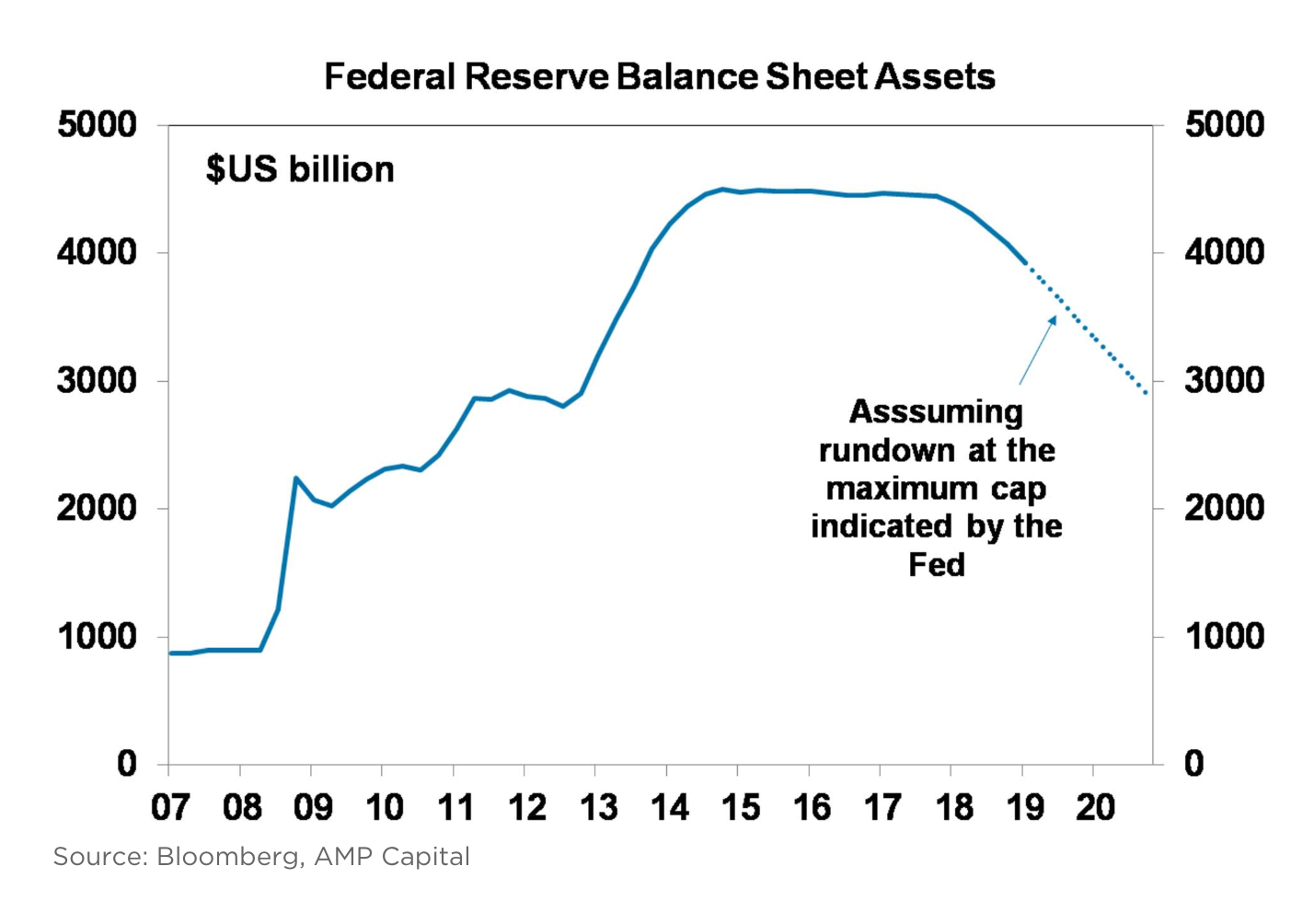

- While the Fed was not dovish enough in December with shares plunging accordingly, it made up for it in the past week going very dovish. Thanks to various “cross currents” that are clouding the outlook, gone is the reference to “further gradual increases” in the Fed funds rate to be replaced by “patience” as it assesses what to do next. Gone too is leaving the normalisation of its balance sheet (or Quantitative Tightening, QT) on “autopilot”, to be replaced by greater flexibility and an end to it at a higher level for the balance sheet than earlier expected. If the end point for the Fed’s balance sheet is around $3.5-3.7 trillion as Fed Chair Powell implied, then QT could be over by year-end. We see the Fed being on hold regarding rates for the next six months at least. The Fed’s dovish shift and its flexibility on rates and its balance sheet is akin to its 2016 interest rate pause and so is positive for investment markets.

- There was also more progress on the US/China trade front after two days of talks, with talks to continue in Beijing this month. Big differences appear to remain, e.g. around intellectual property, and may require a meeting between Presidents Trump and Xi to finalise. We remain of the view that a deal will be reached as both sides are under pressure from slowing growth, but it may require the March 1 deadline to be extended.

- The Fed’s dovishness and progress on trade help tick off some of the conditions for shares to do better this year. Others include Chinese stimulus getting the upper hand, ECB easing, a decisive end to the US government shutdown dispute and signs the US debt ceiling will be raised relatively smoothly, a bottoming in profit revisions and good earnings reporting seasons globally and in Australia, stronger than expected economic data and a bottoming in PMIs and share markets breaking through resistance on strong breadth. Some of these are still likely to drive volatility and setbacks in shares (as deep V style rebounds from falls like those seen last year are unusual) but at least we are making progress.

Major global economic events and implications

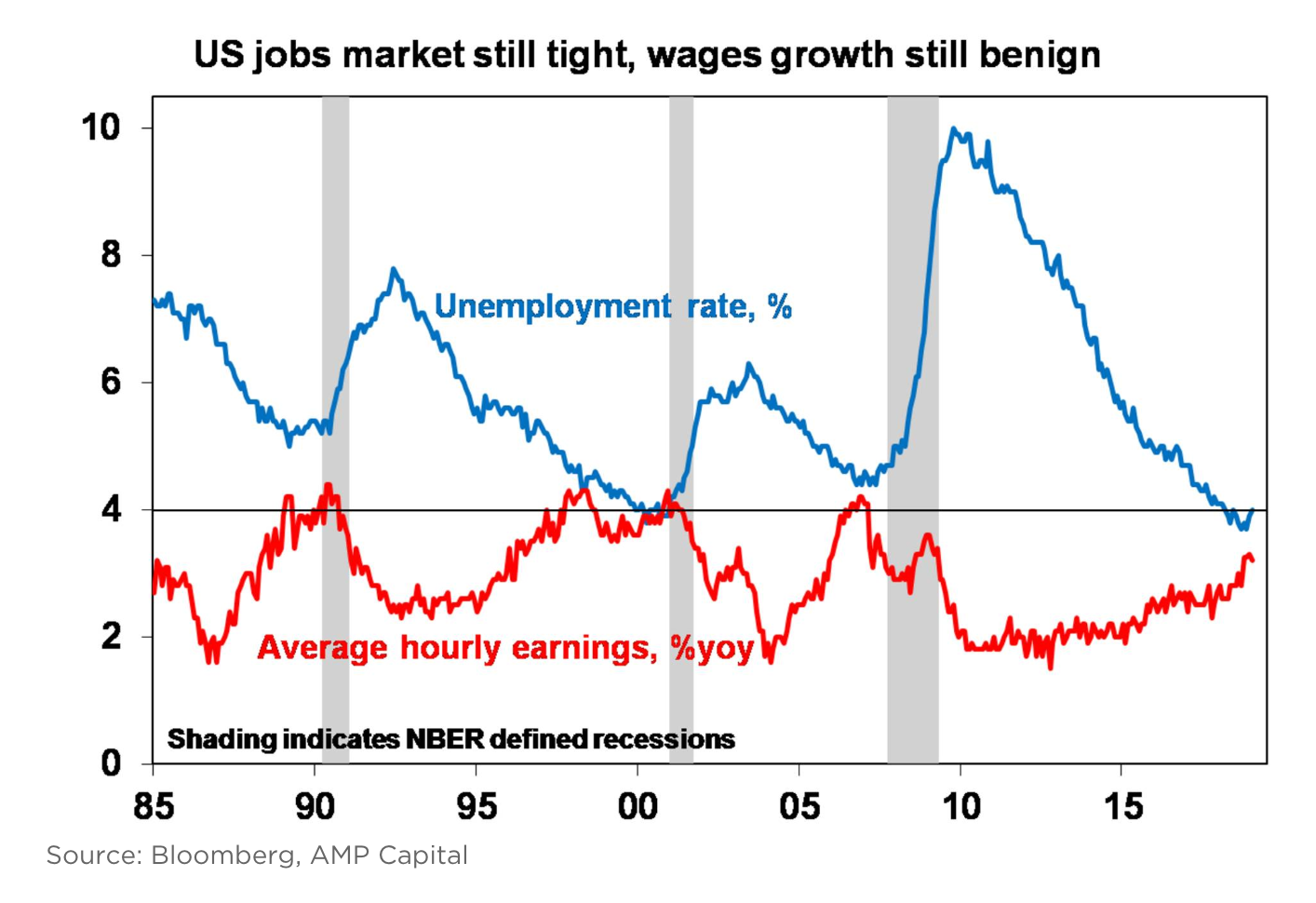

- US data was mostly good over the last week. While consumer confidence fell sharply again, the ISM manufacturing conditions index rebounded in January to a solid 56.6 but with the prices paid component falling further, construction activity rose more than expected in November and payrolls rose by a stronger than expected 304,000 jobs in January. Even with downwards revisions in previous months, payroll growth has been a strong 241,000 over the last three months. While unemployment rose to 4%, this looks to have been due to the partial government shutdown. Meanwhile, although wages growth is trending up, it remained relatively benign in January at 3.2% year-on-year, which is well below the inflation danger zone of around 4% (see the chart below). Overall the data supports the Fed both in terms of the economy remaining solid and the case for a pause on rates with inflation pressures remaining benign. The US money market got a bit ahead of itself though in factoring rate cuts.

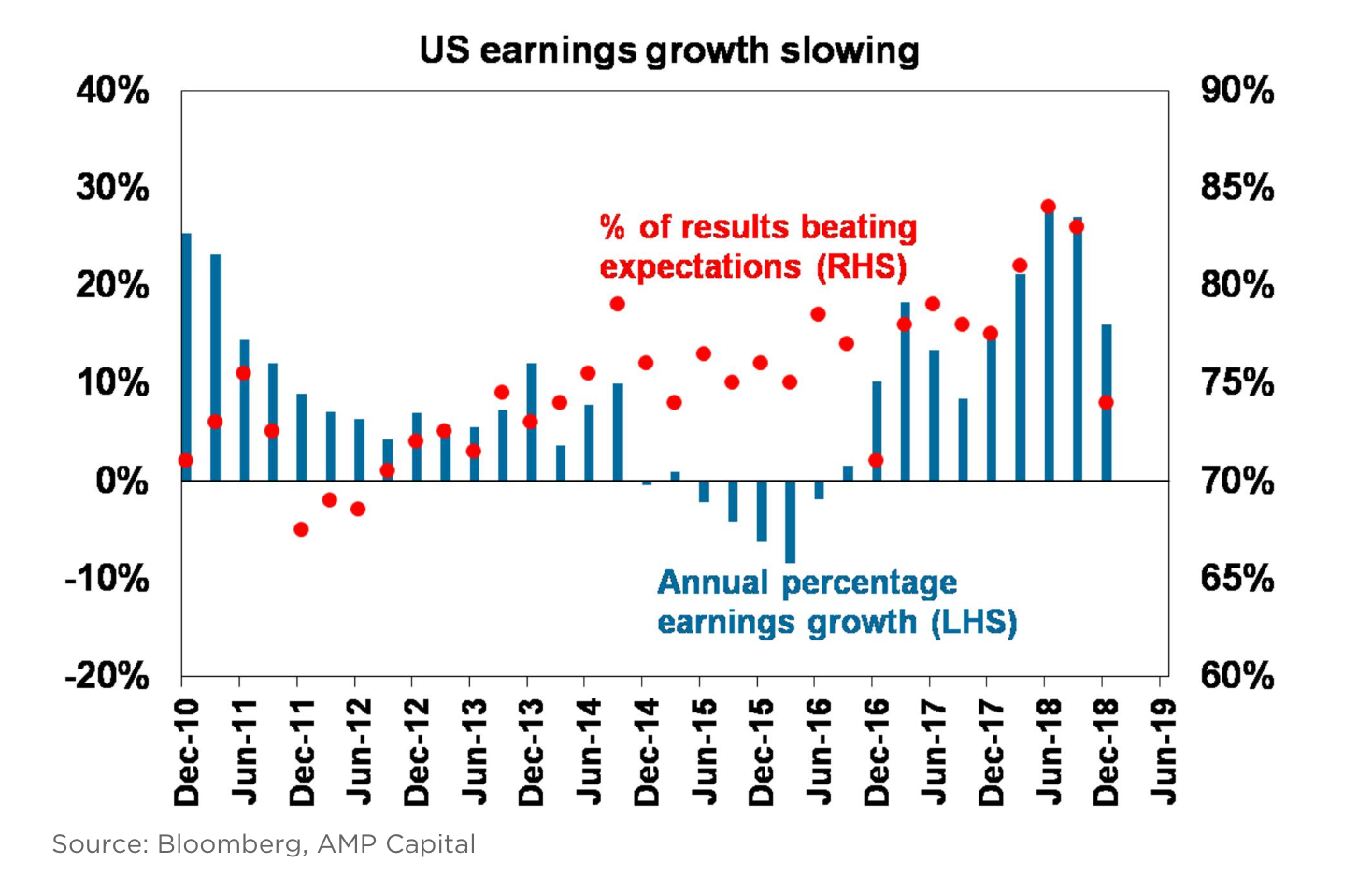

- The US December quarter earnings reporting season remains good, but it’s softer than previous quarters. 220 S&P 500 companies have now reported with 73% beating on earnings with an average beat of 2.3% and 60% beating on sales. Earnings growth is now running at 16.7% year-on-year for the quarter. But as can be seen in the next chart the level of surprises and earnings growth is slowing down as the tax cut boost fades. US earnings growth is likely to be around 5% this year as the tax cut boost drops out.

- The Eurozone remains weak. GDP growth remained soft in the December quarter at just 0.2%, seeing year ended growth drop to just 1.2% its lowest since 2014. Unemployment was unchanged in December at 7.9% and economic sentiment fell further in January. All this means increasing pressure on the ECB to ease again.

- Japanese data is also soft, with lower consumer confidence and industrial production. But at least jobs related data remains strong, albeit its being helped by a falling labour force.

- Chinese business conditions PMIs showed stronger services conditions but still weak manufacturing conditions, particularly for small businesses. Pressure for more stimulus remains.

Australian economic events and implications

- More soft Australian data with the NAB business survey for December showing a sharp fall in business conditions, house price falls continuing in January and credit growth remaining soft. The terms of trade rose solidly in the December quarter thanks to strong export price gains but this means that the contribution to growth from net exports will be weaker than expected which will be a drag on December quarter GDP growth.

- December quarter inflation of 1.8% year on year for both headline and underlying inflation highlights that pricing power continues to remain weak in the economy. That said the December result was not low enough to bring on an imminent rate cut, but the longer inflation stays below target the harder it will be to get it up again as inflation expectations will move down as they did in Japan after years of very low inflation. So with growth likely to disappoint the RBA we see inflation staying below target for longer than the RBA is allowing and see this driving the RBA to cut the cash rate to 1% this year.

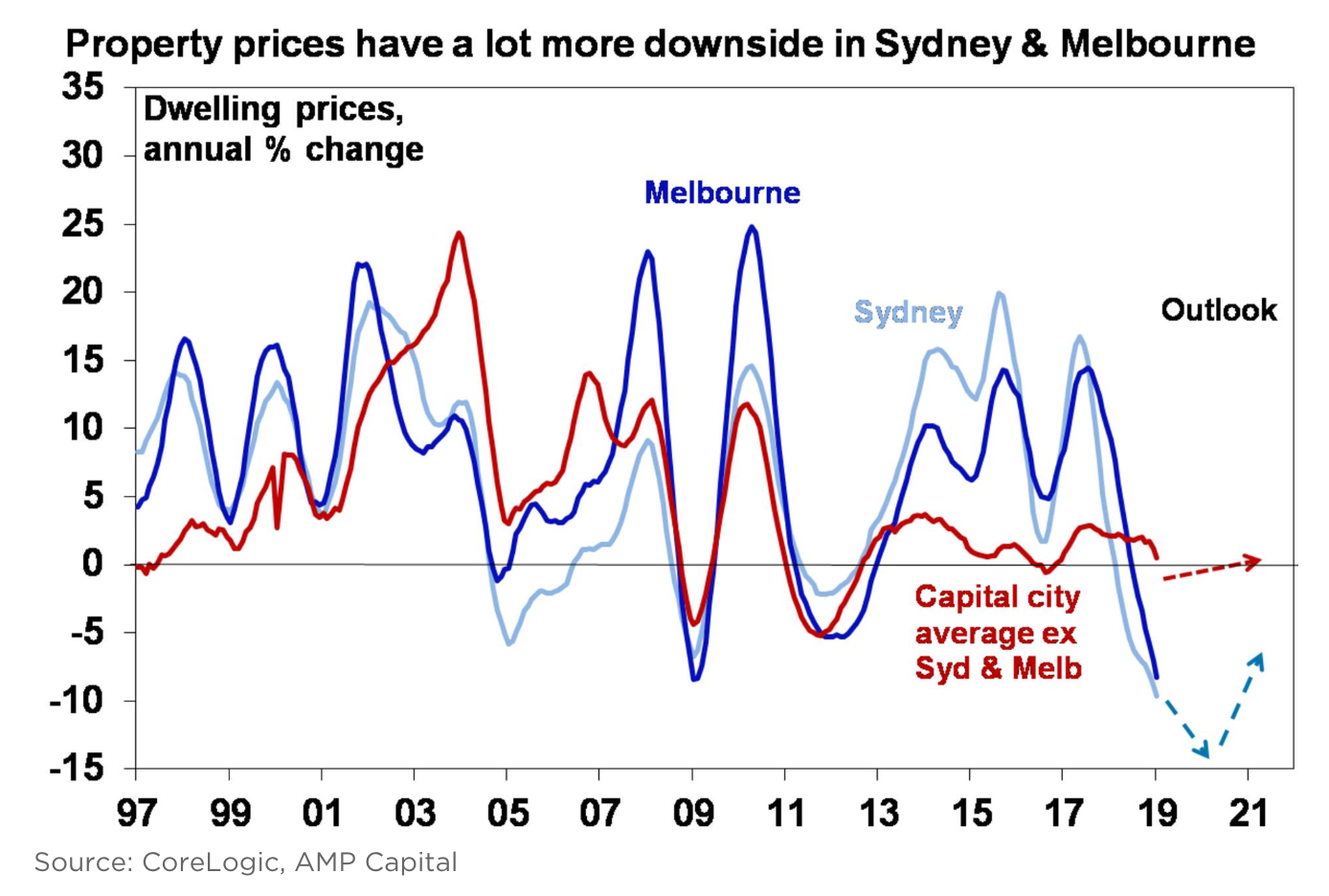

- Meanwhile, CoreLogic data showed a further sharp fall in dwelling prices in January with national capital city prices now down 7.8% from their September 2017 high which is more severe than their fall in the GFC. Sydney prices have now seen their biggest fall since the early 1980s recession. Tight credit, rising supply, falling foreign demand and falling prices feeding on themselves have combined to create a perfect storm for Sydney and Melbourne, with Perth and Darwin still falling and most other cities pretty soft. We see Sydney and Melbourne home prices falling another 15% or so this year as part of a total top to bottom fall of 25%, which with little change in average prices across other cities will see national average home prices fall another 5 to 10% this year. While this is a drag on economic growth it’s unlikely to drive a recession as property price weakness will mainly be concentrated in Sydney and Melbourne, the growth drag from falling mining investment is fading, non-mining investment and infrastructure spending are rising, the RBA can and we think will cut interest rates again and a likely further fall in the Australian dollar will help support growth.

What to watch over the next week?

- In the US, data releases delayed by the shutdown are expected to show a rise in durable goods orders, December core consumption deflator inflation remaining around 1.9% year on year, December quarter GDP growth of around 2.6% annualised, a modest rise in retail sales and a fall in housing starts. In terms of scheduled releases expect to see the non-manufacturing conditions ISM (Tuesday) fall to around the 57 level. Comments by Fed Chair Powell (Thursday) are likely to remain dovish. Finally, it will be another busy week in the US earnings reporting season, with companies including Alphabet, Walt Disney, Ely Lilly and GM due to report.

- The Bank of England (Thursday) is unlikely to make any changes to monetary policy.

- The Australian earnings reporting season for second half of 2018 will also start to get underway but with only 15 major companies reporting including James Hardie (Tuesday), the CBA, IAG and Dexus (Wednesday), Mirvac, AGL and Newscorp (Thursday) and REA (Friday). 2018-19 consensus earnings growth expectations have fallen to around 3% for the market as a whole not helped by slower growth globally as well as locally, with resources running around 8% and the rest of the market around 2%. Resource, building materials, insurance and healthcare look to be the strongest with telcos, discretionary retail, media and transport the weakest and banks constrained. Key issues will be around the impact of the housing downturn, possible changes to franking credits if there is a change of government and how the consumer is holding up.

Outlook for investment markets

- Global shares are likely to see volatility remain high with the high risk of a re-test of December 2018 lows, but valuations are now improved, and reasonable growth and profits should support decent gains through 2019 as a whole helped by more policy stimulus in China and Europe and the Fed pausing.

- Australian shares are likely to do okay but with returns constrained by moderate earnings growth.

- Low yields are likely to see low returns from bonds, but they continue to provide an excellent portfolio diversifier.

- Unlisted commercial property and infrastructure are likely to see a slowing in returns over the year ahead. This is likely to be particularly the case for Australian retail property. National capital city house prices are expected to fall another 5-10% this year led again by 15% or so price falls in Sydney and Melbourne on the back of tight credit, rising supply, reduced foreign demand and uncertainty around the impact of tax changes under a Labor Government.

- Cash and bank deposits are likely to provide poor returns as the RBA cuts the official cash rate to 1% by end 2019.

- Beyond any further near-term bounce as the Fed pauses on rate hikes, the $A is likely to fall into the $US0.60s as the gap between the RBA’s cash rate and the US Fed Funds rate will still likely push further into negative territory as the RBA moves to cut rates. Being short the $A remains a good hedge against things going wrong globally.

Source: AMP CAPITAL ‘Weekly Market Update’

AMP Capital Investors Limited and AMP Capital Funds Management Limited Disclaimer